Airbnb (Ticker: ABNB) - Brief Breakdown

In our Brief Breakdowns, we pick a stock and take opposite sides – one of us presents the bullish argument and the other presents the bearish argument.

If you haven’t already, subscribe to our newsletter here to get our articles directly to your inbox and follow us onTwitter and Instagram!

Company Description

Airbnb Inc. (NASDAQ Ticker: ABNB) is an American company that operates as an online marketplace for lodging, primarily vacation homestay rentals, and tourism activities. Airbnb does not own any of the listed properties; instead it acts as a marketplace and profits by receiving commission from each booking. Airbnb was founded in 2008 and has been a disrupter to the hotel industry, allowing anyone to use a property in any location as a vacation rental. Airbnb currently operates in 100,00 cities and according to Stratojets, had 150 million users in 2018. Although Airbnb has had success, the company has faced criticism for a direct correlation between increases in the number of its listings and increases in nearby rent prices and creating nuisances for those living near leased properties.

Quantitative Analysis

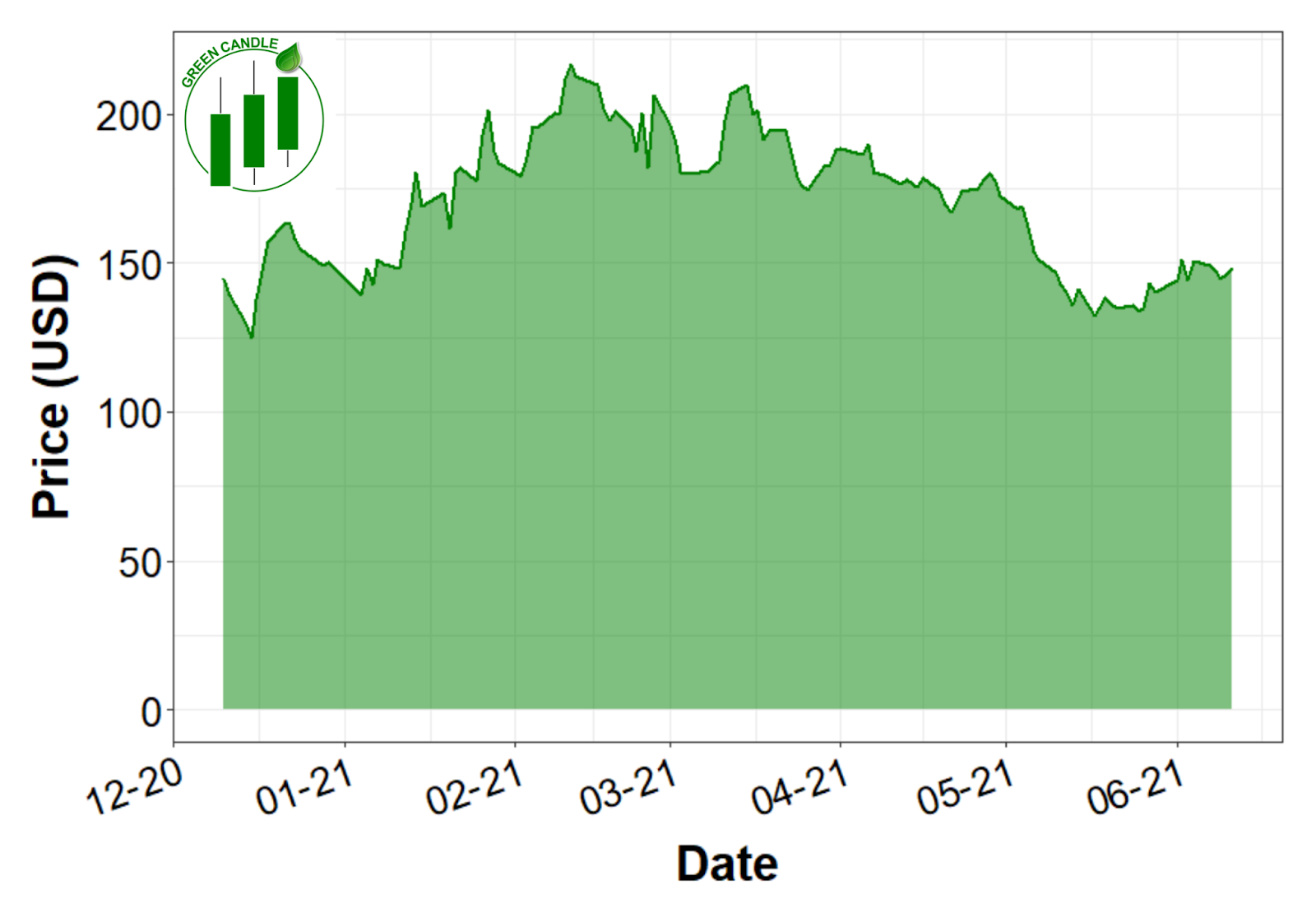

At the time of this writing (6/13/2021), Airbnb is trading at $148.44 with a 52 week range of $121.50 - $219.94 and a market cap of $90.3B. In Q1 of 2021, Airbnb’s revenue was $887 million, representing a 5% increase year-over-year. The Q1 earnings before interest, taxes, depreciation, and amortization (EBITDA) loss was $59 million, which is $190 million better than the same period in 2019 and $275 million better than 2020 on similar revenue. The net margin (net income / revenue) is -155.68%, the return of equity (ROE: Net Income / Total Equity *100) is -412.73% and the debt to equity ratio is 2.91. This financial analysis was done using financialstockdata.com (become a beta tester here). Initially, Airbnb’s stock shot to the moon, going from the initial price of $68 up 223% hitting an all-time high (ATH) of $219.94 in February of this year. Similar to Uber, ABNB’s lack of positive earnings has not hindered stock prices. You can view Airbnb’s 2021 Q1 earnings here and Airbnb’s 2020 annual report here.

Qualitative Analysis

Airbnb has drawn some criticism and has been regulated by jurisdictions such as the European Union and different cities such as San Francisco (where the company originated) and New York City. Similar to Uber, when innovation and disruption happens, there will be push back. Airbnb has drawn criticism over fair housing, housing affordability, hosts using fake information to circumvent Airbnb’s background checks, and bait-and-switch scams. Despite negative publicity, use of Airbnb soared during the COVID-19 pandemic. In the state of Florida, the Florida Rental By Owners reported that booking requests increased 60% over the previous year. And they don’t plan to slow down. On May 24, Airbnb unveiled 100 platform upgrades to help with user experiences. As the CDC loosens COVID-related restrictions, look for travel and vacationing to come booming back. Indeed, ABNB recently reported that rural travel is up to 42% from 32% when compared to the summer of 2019. These travelers appear to be opting for Airbnb rather than traditional booking services like Expedia and Booking, which have declined 67% and 63% percent. Airbnb can benefit from more than just short-stay travelers. With remote work becoming more popular, Airbnb may be able to provide housing for longer-term travelers. Indeed, in Q1 of 2021, 24% of bookings were for 28 nights or longer, showing that people are staying in Airbnb rentals for extended periods of time. If the remote work continues and travel increases as anticipated, Airbnb has a bright outlook for the rest of 2021!

Bullish Thesis

Here are three points to support the bullish thesis:

Competitive Advantage: As others may come into the space or have been in the space but are not as popular as Airbnb, ABNB has a huge competitive advantage in brand recognition. In the first 9 months of 2020 only 9% of users booked due to an ad. This is huge as Airbnb is currently in the stage of reinvesting its revenue back into the company but does not need to focus that budget primarily on marketing as its brand recognition is currently extremely high. Instead of sifting through Google for a place to stay, many will go directly to Airbnb’s website to determine where to stay. As Airbnb is at the top of consumers' minds, that will only benefit Airbnb in the long run. Although Airbnb still has plenty of room to grow with only 29% of the market share and with the strong brand recognition of Airbnb, that is primed to grow.

Source: Rental Scale Up

Remote Work Trend: According to Upwork, the remote work trend from the COVID-19 pandemic may be something that will stay. Approximately 26.7% of Americans will work remotely in 2021 which is a significant increase of only 7% in 2018. As mentioned above, 24% of Airbnb’s bookings were for 28 days or longer, so many are using Airbnb’s to live in a city with remote work opposed to brief travel. This benefits Airbnb significantly over the hotel industry because many would like to feel more at home while traveling and working remotely, with the opportunity to cook and explore a city more in depth. This trend does not seem to be going away and longer stays and traveling around will become more of the norm especially as more vaccines are distributed and more people feel comfortable to travel.

Increase in Travel: With Airbnb’s brand recognition, ABNB is primed for a breakout in 2021 as more and more people will be traveling this summer. Although travel prices are expected to increase and vary by travel destination, domestic travel restrictions are being lifted and many are now comfortable to get back to traveling. According to Forbes, many days in April 2020 TSA screenings were below 100,000 with the busiest day being 171,563 but 2021 is a different story. The busiest day in April 2021 there was 1,572,383 visitors for a daily TSA screening. As travel increases, many will look for places to stay and more people are visiting Airbnb to book travel. This trend is positive for the travel industry in general and will hopefully benefit Airbnb moreso than its competitors.

Bearish Thesis

Here are three points to support the bearish thesis:

Lack of Earnings: Last year (2020), ABNB posted a net loss of $4.6 billion, up from $674 million in losses posted in 2019. COVID-related changes to consumer behavior (reduced travel) and stock-based compensation following their IPO account for the majority of these losses. Lack of earnings is not uncommon for relatively young companies in the tech space, as it often signifies a growth-oriented mindset. This appears to be the case for ABNB. According to Motley Fool, while most of ABNB’s operating expenses have remained stable over the last 5 years, their R&D expenses have increased 10-fold. However, until ABNB leadership makes the company more profitable, investors - particularly value investors not overly impressed by growth on its own - may want to proceed with caution.

Competition and Regulatory Uncertainties: ABNB operates in the massive hospitality industry, where state-by-state regulation and competition from major hotel brands could become overbearing. While major hotel chains rely on construction to expand their control over room supply, ABNB relies on adding new hosts to their platform. While ABNB’s model is cheaper (no construction costs), it is much less predictable. This gives major hotel chains an advantage in scalability and will ultimately help them maintain control over room supply. Additionally, well-established hotels have operated in the market longer, are more familiar with the regulations and compliance necessities, and have built relationships with the regulatory agencies. This provides major hotel chains with lobbying power, which could force ABNB into a regulatory nightmare.

Lack of Hosts: As stated above, ABNB’s entire model relies on hosts voluntarily signing up to use their platform. It’s a challenging thing - ABNB needs to find creative ways of getting individuals to agree to let strangers stay with them. If customers grow at rates faster than hosts, they run into an obvious supply/demand imbalance. According to businessofapps.com, from 2016 to 2019 bookings grew from 52 to 193 million (3.7x increase) while listings grew from 2.1 to 7 million (3.3x increase), putting supply growth slightly behind demand growth. As of March 2021, there were only 4 million active hosts on the platform and the average annual earnings per host was $9,600. ABNB will need to focus on incentivizing hosts and making the onboarding process as streamlined as possible to encourage individuals to sign up. Investors should keep an eye on customer growth relative to host growth when assessing ABNB - if they fail to onboard new hosts, its model could fail.

Learn more about Airbnb here. Stay up to date on Green Candle by subscribing to our newsletter and following us on Twitter and Instagram!

Disclosure: The article was written by Daniel Kuhman and Brandon Keys, and it expresses the author's own opinions. They are not receiving compensation for it. They have no business relationships with any company whose stock is mentioned in this article. The information presented in this article is for informational purposes only and in no way should be construed as financial advice or recommendation to buy or sell any stock. Brandon and Daniel are not financial advisors. We encourage all readers to do further research and do your own due diligence before making any investments.