Alphabet Inc. (Ticker: GOOG) - Brief Breakdown

In my Brief Breakdowns,I pick a stock and present opposite sides – I present the bullish argument and the bearish argument.

If you haven’t already, subscribe to our newsletter here to get our articles directly to your inbox and follow us on Twitter and Instagram! Also join us for our Twitter spaces, every Tuesday we discuss our stock breakdown at 8 PM EST, & Friday we have a Bitcoin Happy Hour at 4:30 PM EST!

Company Description and Qualitative Analysis

Alphabet Inc. is an American multinational conglomerate that is the parent company of Google and several of former Google subsidiaries. Alphabet is the world’s fourth-largest technology company by revenue and one of the world’s most valuable companies. Alphabet Inc. provides online advertising services in the United States, Europe, Middle East, Africa, the Asia-Pacific, Canada, and Latin America. It offers performance and brand advertising, operates through Google Services, Google Cloud, and Other Bets segments. The Google Services segment provides products and services such as ads, Android, Chrome, hardware, Google Maps, Google Play, Google Search, and YouTube, as well as technical infrastructure and digital content. The Google Cloud segment offers infrastructure and data analytics platforms, collaboration tools and other services for enterprise customers (similar to Amazon Web Services). The company has an agreement with Sabre Corporation to develop an artificial intelligence-driven technology platform for travel. Alphabet also has the most hours driven of any artificial intelligence self-driving vehicle with their company Waymo. Alphabet is publicly traded under two tickers: GOOG and GOOGL. GOOG shareholders have no voting rights and GOOGL shareholders do. It is perhaps best known for its search engine, which remains the most dominant search engine on the Internet. Google’s search engine is so widely used that it has seeped into common parlance, with people commonly saying “Google it” to reference an internet search. Alphabet has various sources of revenue including products and services such as ads, Android, Chrome, Google Maps, Google Play, Search, YouTube, Google Cloud and much more. Google has facilitated the digitization of information and has created platforms that increase access to that information. Google also owns Android, which accounts for 73% of the mobile OS market. YouTube TV ranks second in streaming services. All this is to highlight just how enormous Alphabet and Google are, and with their access to capital, competitors will be hard pressed to penetrate GOOGL’s moat.

Quantitative Analysis

At the time of this writing (8/14/2022), GOOGL is trading at $122.65 with a market cap of $1593.17B and a 52-week range of $102.20 - $152.10. In Q2 of 2021, Alphabet’s revenue grew to $69,685 million, up 13% year over year (16% in constant currency). Operating income grew to $19,453 million and operating margin grew to 28%. Return of equity (ROE: Net Income / Total Equity *100) of Alphabet Inc. is 28.65%, the price to earnings ratio (P/E) is 22.46, and net margin (net income / revenue) is 25.89%. You can view GOOG’s 2022 Q2 earnings here and their 2021 Annual Report here.

INVRS is a social and collaborative investment research platform which I recently started using and absolutely LOVE. INVRS is increasing access to high-quality investment research and discussion. Its built around top notch data and tools for over 10k stocks and ETFs and the best part is its completely free to sign up! Sign up here and join my Green Candle Group!

Bullish Thesis

Here are three points to support the bullish thesis:

Google Accounts Integrated into Other Services: I often talk about the “stickiness” of products/services. There is perhaps no better example of “stickiness” in the digital space than Google. Google’s search engine is now so commonly used that the term “Google” has become a verb (as in “Google it”). With smartphones, the knowledge of the internet is in your pocket, and it’s accessed predominantly via Google. Indeed, Google is by far the top search engine, claiming ~92% market share (Bing is second, with only 2.4% market share). But Google’s search engine isn’t the only thing that people have come to rely on for daily use. Gmail, Google’s email client, is the top email platform in the world with 1.8 billion users (~18% market share). Google is also commonly used for cloud storage (Google Drive), video-based meetings (Meet), navigation (Maps), scheduling (Calendars), and much more. These services/products have become so ingrained in the daily lives of users, it’s hard to see any competition toppling Google.

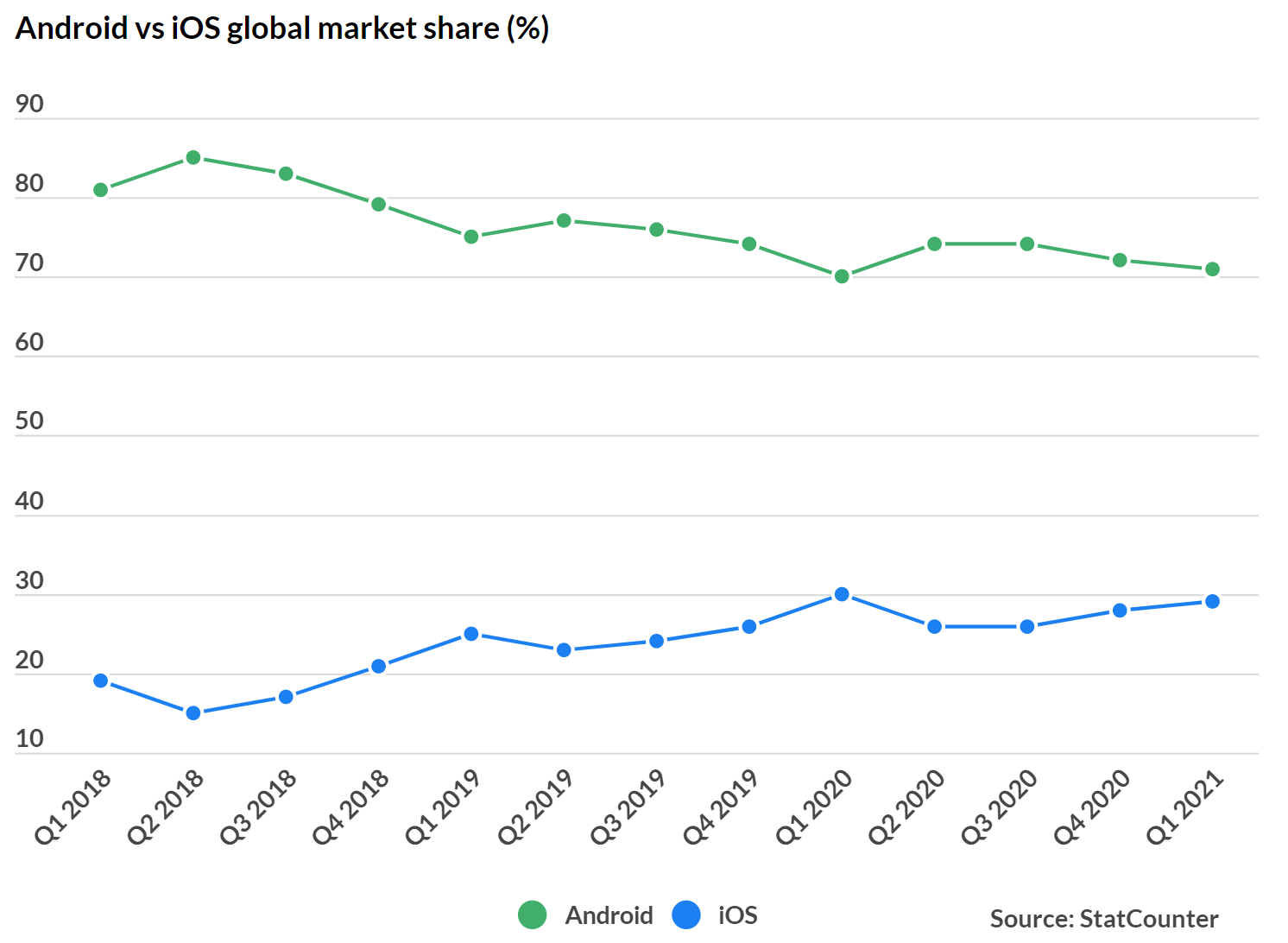

Dominating market share in multiple domains: Google dominates market share across multiple services. Their search engine is far and away the most used in the world, claiming 91.5% market share. Google’s Android has 2.8 billion active users around the world, dominating the global market share of mobile devices (71%). With 1.8 billion users globally, Google’s Gmail is the top email platform in the world with 18% market share. According to statista, Google Maps was the most downloaded navigation app in the U.S. in 2020. Google’s cloud storage currently ranks third in market share of cloud-based infrastructure with 9% (behind Amazon Web Services and Azure). A whopping 74% of adults in the U.S. use YouTube (owned by Alphabet), which is more than Facebook’s 68% and nearly double Instagram’s 40%. Google’s ability to play such a massive role in multiple global markets should keep investors bullish. Globally, Android is more popular everywhere but the United States. This is encouraging because not only does it dominate multiple markets, Android has room to grow in one of the largest markets in the world.

Access to Capital: As highlighted above, Google is a major player in multiple markets and generates revenue via seval streams (primarily through online advertising). Google’s massive revenue, combined with the reputation of their brand name, give them access to nearly unlimited capital. Access to capital, particularly in the technology space, can be a huge advantage. Capital can allow Google to both acquire other companies (as they did in 2006 when they purchased YouTube) and invest in R&D for their own internal products/services. In a space where growth is seen as a key indicator for a company, Google has the capacity to grow via acquisitions and internal development.

Bearish Thesis

Here are three points to support the bearish thesis:

Majority of Revenue from Ads: In Q2 2022, 80% of Alphabet’s total revenue was from the display of advertisements online. Alphabet relies on other companies needing to advertise and others access to capital to advertise. This is reliant on Alphabet’s ability to provide value to its clients to want to advertise with Alphabet and Google. Changes to advertising policies and data privacy practices can drastically affect Alphabet’s main source of revenue. There has been a recent development in technologies that have make customized ads more difficult or block the display of ads altogether and some providers of online services have integrated technologies that could hinder Alphabet’s ability to advertise as a third-party company. This also has not changed over time. In the past two years, revenue from advertisements based on percentage of total revenue remains unchanged showing a lack of priority to change from Alphabet’s management.

Continually Investing in New Businesses: Alphabet and in turn Google has a lot of access to capital and the company invests that money into new businesses, products, services, and technologies. Although the amount of capital Alphabet has access to is incredible, if multiple investments fail this could prove to be detrimental to the cash flow of the business. Google Services continues to invest heavily in hardware such as smartphones and home devices, Google Cloud invests in enterprise-ready cloud services, and Other Bets is investing heavily in health, life sciences, and transportation. Due to the wide range of investments it is tough to see all of them failing but it is a possibility as Alphabet tries to diversify its revenue streams.

Supply Chain Disruption: Currently, Alphabet relies on other companies to manufacture many of its finished products, to design certain components and parts, and to participate in the distribution of Alphabet’s products and services. There are always inherent risks when using a third-party to manufacture and distribute products and services and these companies can be shut down due to various factors. There has been a chip shortage and with a potential China and Taiwan conflict, this could continue to persist.

Learn more about Alphabet here. Stay up to date on Green Candle by subscribing to our newsletter and following us on Twitter, Instagram, and YouTube!

Video edition: Sunday Scaries Stock Talk

If you’re new to stock investing, check out our introduction to stock investing series:

Have a great week everyone,

Brandon

Sign up for INVRS here and join my Green Candle Group!

Disclosure: The article was written by Brandon Keys, and it expresses the author's own opinions. I am not receiving compensation for it. I have no business relationships with any company whose stock is mentioned in this article. The information presented in this article is for informational purposes only and in no way should be construed as financial advice or recommendation to buy or sell any stock. Brandon is not a financial advisor. I encourage all readers to do further research and do your own due diligence before making any investments.