Amazon.com, Inc. (Ticker: AMZN) - Brief Breakdown

Amazon.com, Inc. (Ticker: AMZN) - Brief Breakdown

In our Brief Breakdowns, we pick a stock and take opposite sides – one of us presents the bullish argument and the other presents the bearish argument.

In the coming weeks, we will be covering the FAANG stocks (Facebook, Amazon, Apple, Netflix, and Google) because of their size and popularity. These will be coupled with our new Wednesday newsletter, which covers basic investing information. If you haven’t already, subscribe to our newsletter here to get our articles delivered directly to your inbox and follow us onTwitter, Instagram, and YouTube for the most up to date information on Green Candle!

Company Description

Amazon.com, Inc. is an American multinational technology company that is a leader in e-commerce, cloud computing, digital streaming, and artificial intelligence. Amazon was famously founded by Jeff Bezos as an online marketplace for books and has since grown into the largest e-commerce marketplace in the world. Amazon has evolved and expanded its capabilities and offers a very wide range of products including video games, software, electronics, clothing, toys, food, and much more. Amazon owns Amazon Web Services (AWS), the world’s largest seller of cloud computing services. Amazon entertainment streaming services produce its own movies and TV shows and Amazon Music provides access to millions of songs. Amazon is also a subsidiary of Ring home security services and owns Whole Foods Market, one of the leaders in organic grocery retail. The list goes on with all of Amazon’s different products and it seemingly has a product in every sector. Amazon is one of the top five market caps in the world, making it one of the largest publicly traded companies globally.

Quantitative Analysis

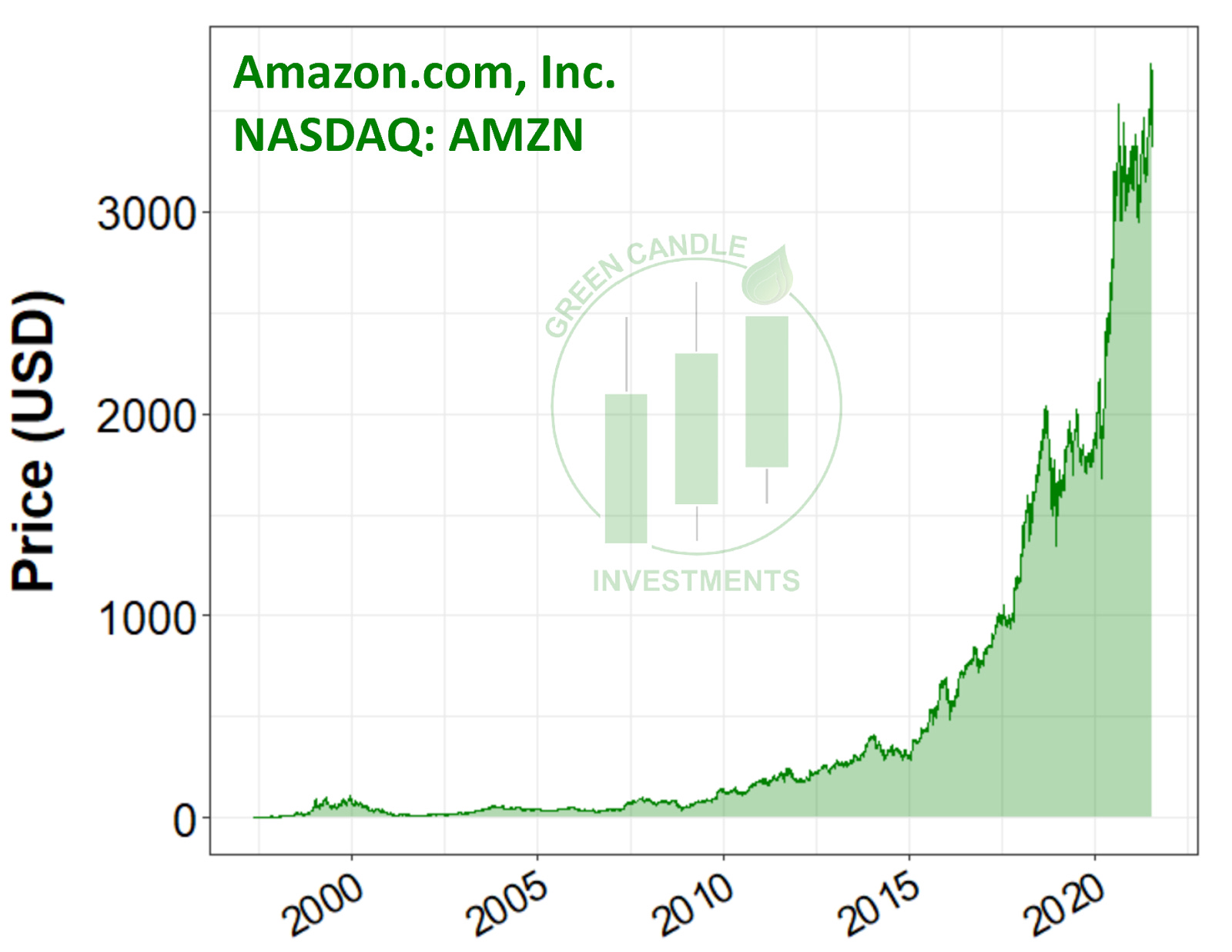

At the time of this writing (8/1/2021), AMZN is trading at $3,327.59 with a market cap of $1.68T and a 52-week range of $2,871 - $3,773.08. Amazon is in a league of its own - its main competitor may be Alibaba, whose stock has had nowhere near the run that Amazon has had. Alibaba’s stock price has been about even with its 2020 low while Amazon’s price is up over 100% from its low of 2020. Amazon released its Q2 earnings on July 29th, which reported an operating cash flow increase of 16% to $59.3 billion for the past 12 months, a net sales increase of 27% to $113.1 billion, an operating income increase to $7.7 billion, and a net income increase to $7.8 billion. The return of equity (ROE: Net Income / Total Equity *100) of Amazon is 30.47%, the price to earnings (P/E) ratio is 57.98, and the Net Margin (Net Income / Revenue) is 6.42%. This financial analysis was done using financialstockdata.com (become a beta tester here). You can view AMZN’s 2021 Q2 earnings here and their 2020 Annual Report here.

Qualitative Analysis

Amazon is the largest e-commerce company in the world, with various other industries including the leader in cloud-based computing services with AWS. It is estimated that over 40,000 businesses gross sales of over $1 million through Amazon. Amazon has established a moat and now is ranked 2nd in the Fortune 500 company rankings, trailing only Walmart. The COVID-19 pandemic skyrocketed Amazon’s growth, as more and more people were forced (through lockdowns) or opted for online shopping. Although the pandemic seems to be near the end, many enjoy and have developed the habits of delivery, which bodes well for AMZN’s future. Amazon continues to grow and expand into various fields with innovative ideas and the necessary capital to back their efforts.

Bullish Thesis

Here are three points to support the bullish thesis:

Size: It is almost a given, but the size of Amazon is absolutely incredible. Amazon has about 1.3 million employees, profits over $113 billionin revenue in the past year and has companies relying on their platforms for sales and for cloud based services. Because of Amazon’s size it has the ability to allocate capital to new and innovative projects and take risks in order to grow the business. It is always a risk to expand and grow, but the amount of capital Amazon makes each year or even quarter allows Amazon to attempt to grow and will allow Amazon to potentially fail on some of those attempts. It is difficult to continually grow, but with money and the brand name of Amazon it is difficult to see a world where Amazon’s growth halts.

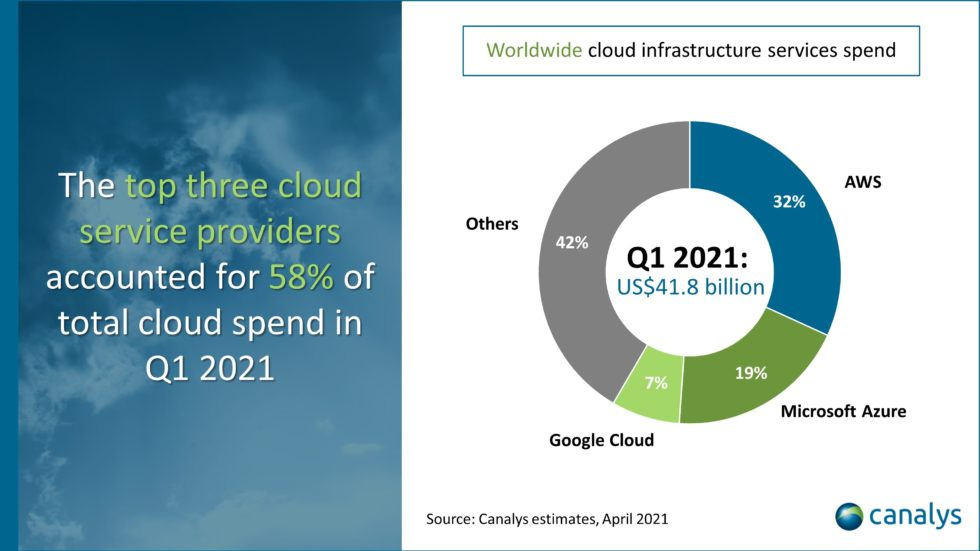

Product Diversity: Amazon is the largest e-commerce site and has the largest web services platform by a large margin. Of the web cloud market, AWS holds 32% of the market with the next largest only holding 19% of the market. Amazon is not a one-trick pony and this will give Amazon revenue in multiple areas so no matter if one sector of Amazon is affected, others might be able to pick up the slack. Amazon now offers Amazon Prime, consumer electronics (Kindle, Alexa, etc), digital content, Amazon Studios, Amazon Game Studios, Amazon Video, groceries, Amazon business, Amazon Drive, and even offers its own brand label of various products. It will take failure in multiple industries in order for Amazon to fail.

Innovation: Amazon keeps coming up with new ways to make money and is not afraid to take risks to innovate in some way, shape, or form. Amazon has the financial backing to create whatever it wants. Amazon looks to expand its telehealth sector called Amazon Care with the delivery of prescription drugs. Amazon can now expand its healthcare services which can be a great growth opportunity as health care costs are nearly ⅕ of the entire United States economy. Amazon would be the first company working on this type of delivery and if it's successful, it would mean significant growth for Amazon going forward.

Bearish Thesis

Here are three points to support the bearish thesis:

Regulation Uncertainties: At the top of the list of bear arguments against Amazon is regulatory uncertainty. Like many other large tech companies, Amazon has fallen under the scrutiny of government officials/agencies both in the U.S. and abroad. The primary pushback against Amazon is from antitrust watchdogs, who accuse Amazon of creating an anti-competitive environment, particularly in its treatment of third party sellers. The U.S. Congress introduced a series of bills in June that targeted Amazon and other tech giants (like Apple and Google) and could cause major disruptions in their business operations. And they’re not just under attack from the U.S. government. Last week (7/30/2021), an E.U. regulator slapped Amazon with a nearly $900M fine for breaching data privacy laws - Amazon said they would be appealing these fines, however. As Amazon grows, the regulatory pressure will only get larger.

Logistics of scaling e-commerce: There’s no question that more and more people are opting to purchase goods online rather than in person. This trend started well before the COVID pandemic and experienced windfall growth during COVID-related lockdowns. COVID-related growth in online shopping exposed bottlenecks in Amazon’s e-commerce pipeline - during the first several months of the pandemic, Amazon was forced to limit restock quantities of “non-essential” goods and experienced such a spike in demand that they removed web features such as “frequently bought together” recommendations to slow excess ordering. Amazon has gradually eased these limitations, in part due to logistics optimization but also due to economic re-opening. As Amazon continues to grow, it will need to scale and optimize logistics without compromising features and services that customers know and expect. If they’re unable to successfully scale, Amazon could lose customers.

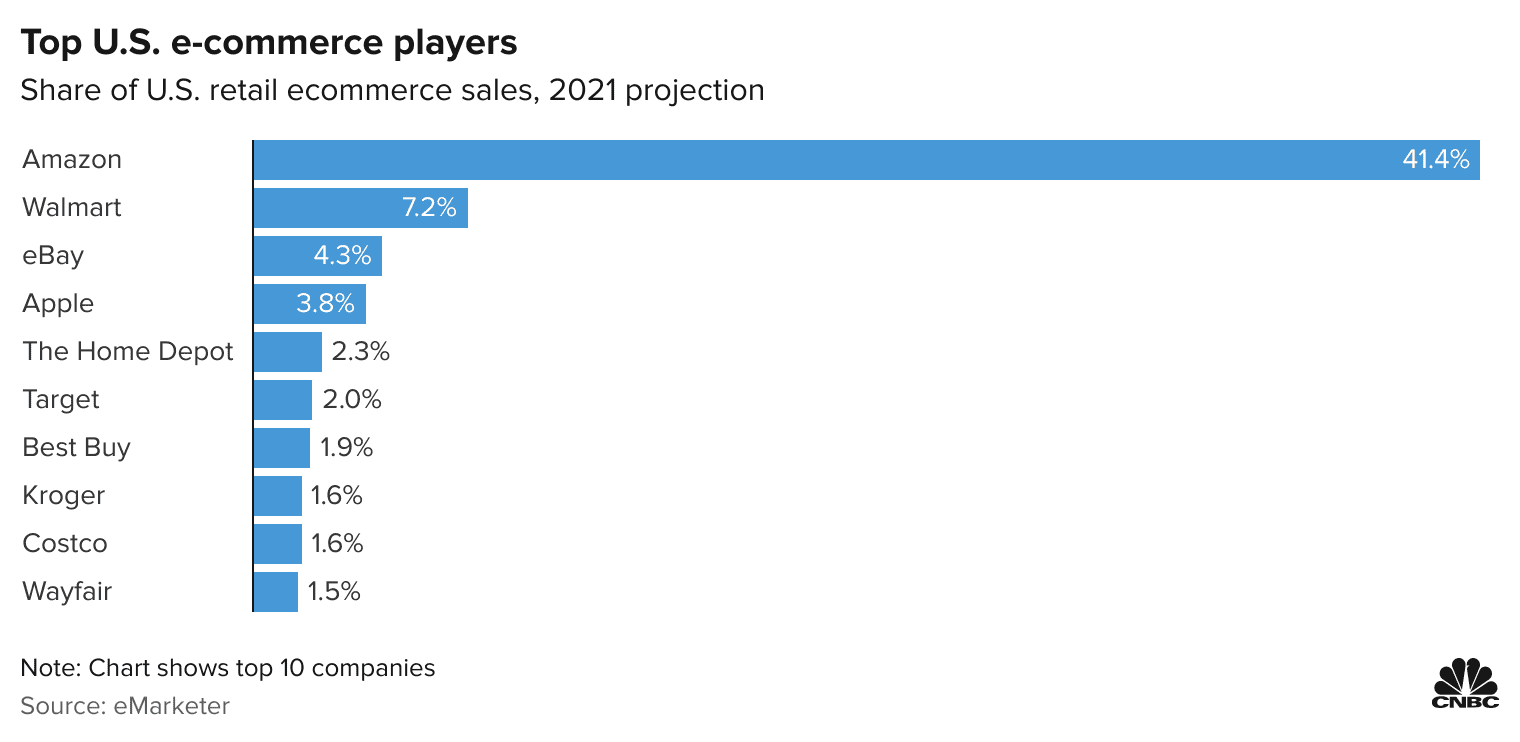

Increasing competition in the e-commerce space: The COVID pandemic forced many retailers to shift their focus toward e-commerce rather than in-person shopping. Although Amazon is currently sitting atop the e-commerce mountain (by a large margin), it’s important to recognize that other major companies - like Walmart - are climbing quickly. According to data by eMarketer, although Amazon currently controls 40% of e-commerce market share, competitors such as Walmart and Target have experienced faster growth rates. Fortunately for Amazon, many of its primary competitors also offer in-person retail, which may make hyper-focused e-commerce R&D more difficult (they must maintain customer experience both online and offline). Investors should keep their eyes on Amazon’s competitors as much as on Amazon itself - if the competition heats up, Amazon could lose its online dominance.

Learn more about Amazon here. Stay up to date on Green Candle by subscribing to our newsletter and following us on Twitter, Instagram, and YouTube!

Have a great week everyone,

Brandon & Daniel

Disclosure: The article was written by Daniel Kuhman and Brandon Keys, and it expresses the author's own opinions. They are not receiving compensation for it. They have no business relationships with any company whose stock is mentioned in this article. The information presented in this article is for informational purposes only and in no way should be construed as financial advice or recommendation to buy or sell any stock. Brandon and Daniel are not financial advisors. We encourage all readers to do further research and do your own due diligence before making any investments.