Brief Breakdown: McDonald’s Corp (NYSE: MCD)

In our Brief Breakdowns, we pick a stock and take opposite sides – one of us presents the bullish argument and the other presents the bearish argument. If you haven’t already, subscribe to our newsletter here to get our articles directly to your inbox and follow us on Twitter and Instagram! Also join us for our Twitter spaces, every Tuesday we discuss our stock breakdown at 8 PM EST, & Friday we have a Bitcoin Happy Hour at 4:30 PM EST!

Video edition: Sunday Scaries Stock Talk

Company Description

McDonald’s Corporation operates and franchises McDonald’s restaurants globally. It is the largest fast food chain and largest restaurant chain by revenue, serving over 69 million customers daily in over 100 countries across 39,198 outlets as of the end of 2020. McDonald’s is known globally and sponsors many big events such as the Olympics.

Quantitative Analysis

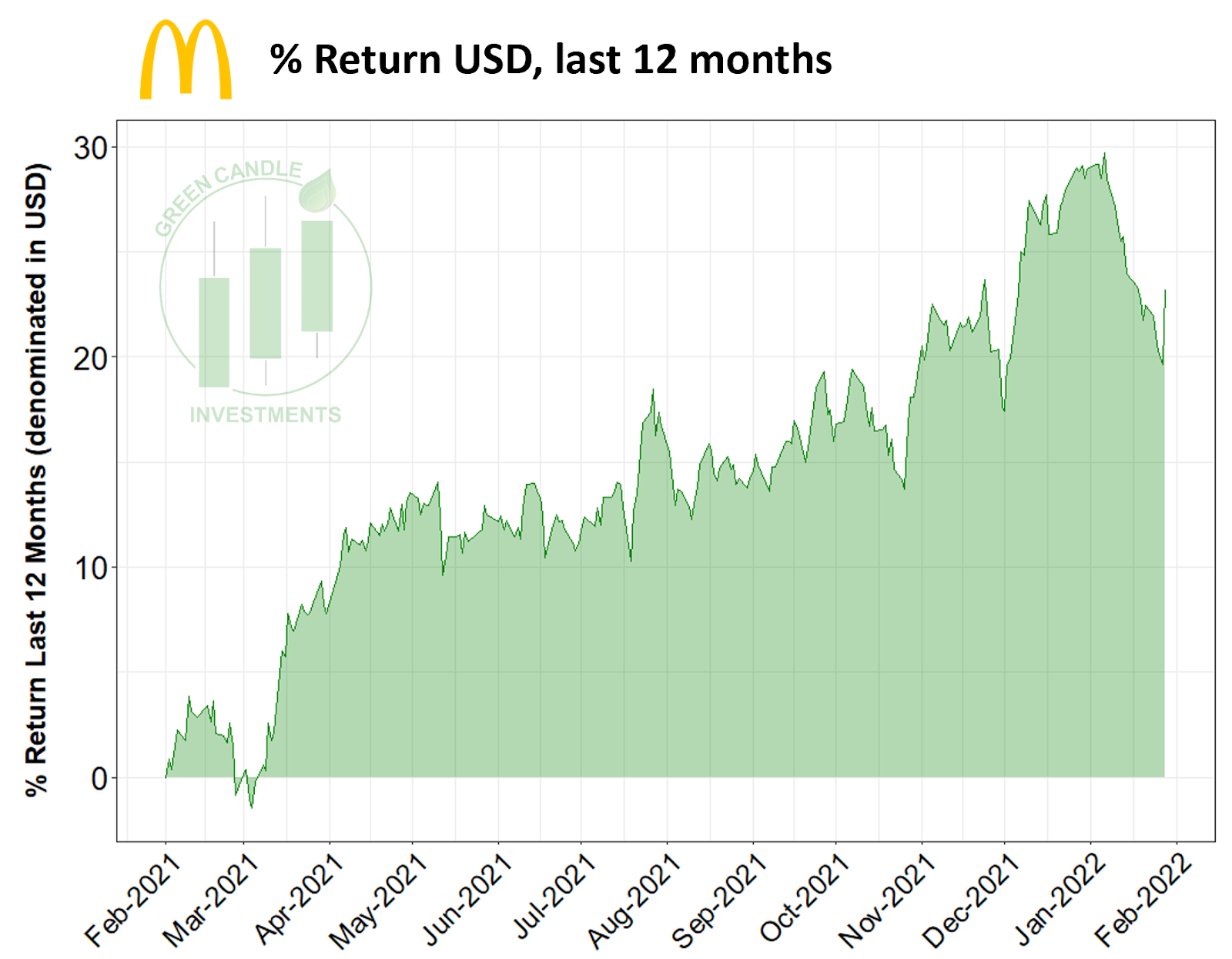

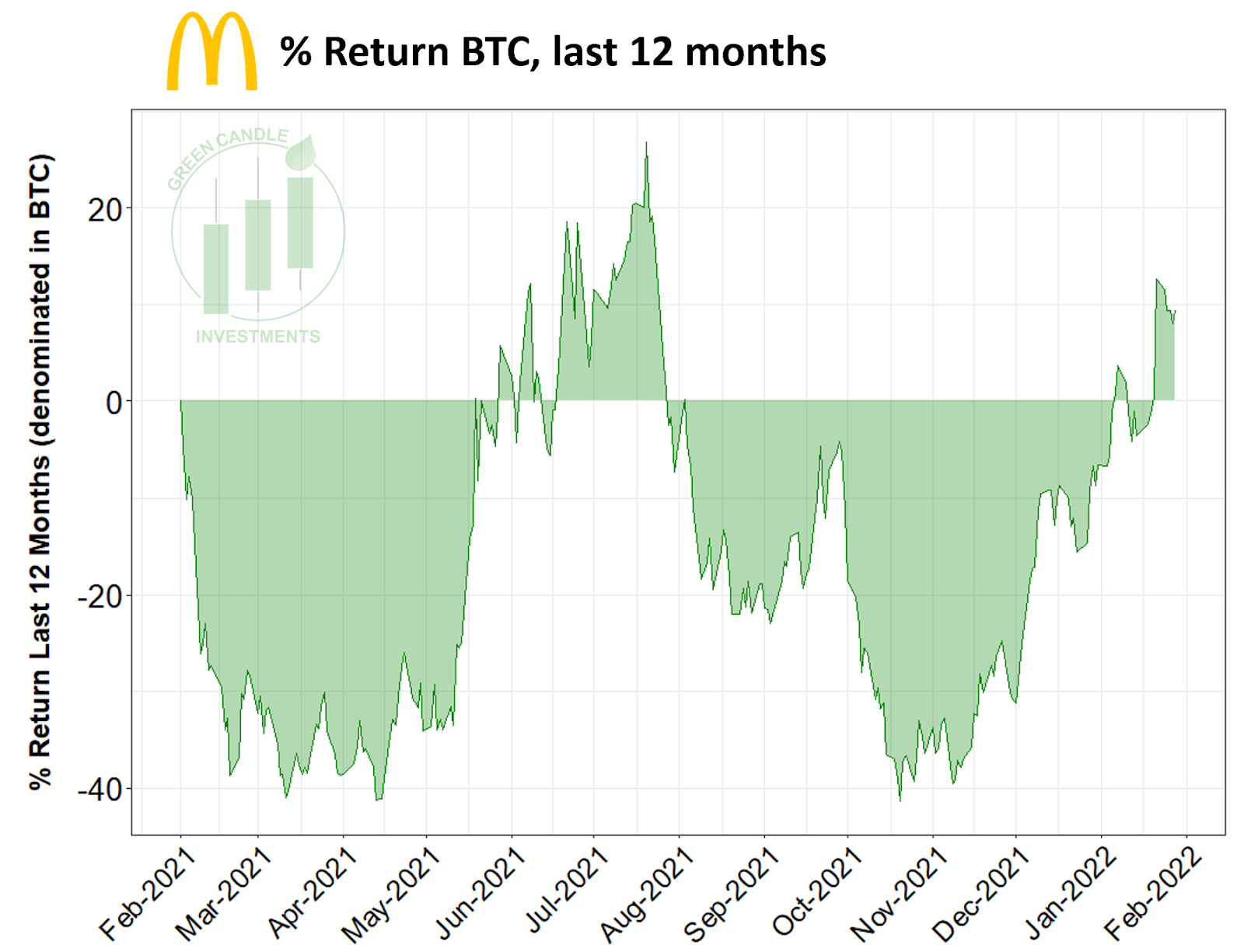

At the time of this writing (1/30/2022), MCD is trading at $256.09 with a 52 week range of $202.73 - $271.15 and a market cap of $191.36B.

In Q1 of 2021, McDonald’s comparable sales and revenues for the quarter surpassed Q1 of 2019 driven by the US sales. Global comparable sales increased by 7.5% in Q1 with growth across all segments. Diluted earnings per share of $2.05 increased by 39% excluding strategic gains, diluted earnings per share of $1.92 increased 31%. MCD has a price to earnings ratio (P/E) of 25.52, return of equity (ROE: Net Income / Total Equity *100) of -109.76% and net margin (net income / revenue) is 32.33%. The debt to equities ratio (total liabilities / total equity) is -10.29. This financial analysis was done using financialstockdata.com (sign up using our promo code GCI here). You can view MCD’s last quarterly earnings here and 2020 annual report here. Below we have percent returns denominated in both USD and in Bitcoin.

Financial Stock Data allows users to analyze a company’s financials and qualitative factors such as leadership better than any other platform available. You can use the same tool as the pros for 50% off using our promo code GCI at checkout. Be sure to sign up for Financial Stock Data HERE.

Qualitative Analysis

McDonald’s raised its prices on its famous Big Mac, Chicken McNuggets and other food items, helping them offset the sharp rises in food and labor costs. This move gave McDonald’s its highest revenue since 2016. Although there is no shortage of competitors in the fast food industry, McDonald’s is the largest and most well known chain globally, controlling ~21% of the market. There is a recent push for cooking and eating healthier, which has hurt McDonald’s up until this past quarter. However, if household expenses continue rising (e.g., rent, mortgages, taxes, etc.), people will likely seek out cheaper alternatives for food, and McDonald’s might be at the top of that list. The McDonald’s brand is powerful and it will continually be known as the king of fast food, whether or not that will hold weight in the future, time will tell.

Bullish Thesis

Here are three points to support the bullish thesis:

Market dominance in a thriving industry: The global fast food industry continues to grow, and McDonalds continues to dominate in market share. According to market research by T4, the size of the global fast food industry grew from $540B in 2016 to $636B in 2020 (a 17.8% increase). The same analysis projects that the industry will grow by an additional $55B by the end of 2022. For the 12 months ending in March of 2021, fast-food chains took in 70.2% of dollars spent eating out and 82.9% of all restaurant traffic, according to data from The NPD Group. In this thriving industry, McDonalds reigns supreme, claiming 21.4% of global fast food market share. If McDonalds can continue its market dominance, it seems like a no-brainer for investors in the fast food space (*not financial advice).

Automated order taking: In 2019 McDonalds acquired technology firm Apprente and rebranded it to McD Tech Labs to “advance employee and customer facing innovations.” In October of last year McDonalds announced that they would be selling McD Tech Labs to IBM as part of a larger, more strategic partnership with the iconic technology giant. With the help of IBM, McDonalds plans to create and scale out better automated order taking (AOT) technologies - including improved mobile app UI/UX and in-person technologies in dining rooms and drive-thrus. According to CEO Chris Kempczinski, "That work is beyond the scale of our core competencies, if you will. And so I think in this case, IBM is a natural partner for us." These technologies not only have the potential to improve customer experience (e.g., more convenient ordering, faster food delivery, etc.), but could also help cut down on operating expenses (e.g., lower labor costs).

McDelivery: McDonalds, like many other businesses, was forced to improve their delivery services over the last two years as economic policies and changes in consumer behavior kept foot traffic in their dining rooms low. Since 2016, McDonalds has expanded their delivery footprint from just 3,000 restaurants to more than 32,000 restaurants across 100 countries. Their “McDelivery” program still relies on third party delivery operators like DoorDash and Uber Eats, whose service fees can eat into profits. However, McDonalds expects that the size of their consumer base could be used as leverage in negotiating better rates with these delivery services. In a Q3 call last year, they said "we have an ability to drive traffic to (3rd-party delivery) apps that we think is second to none, and that should be reflected in the rates that we're paying," adding that “this is yet another example of where our scale confers upon us competitive advantages.”

Bearish Thesis

Here are three points to support the bearish thesis:

Post-Pandemic Healthy Trend: More and more people globally have become more aware of their health and one of the first areas many try to improve is their diet. McDonald’s has the perception of being unhealthy and very bad for you, so many will cut fast food out in general. The fast food industry has grown, but not at the pace of inflation. This past quarter was the highest revenue since 2016, but it came after increasing prices on their menu. The healthy trend will be something to watch going forward to see if it affects McDonald’s as it has in previous quarters outside of Q1 of 2021.

Increased Costs to Operate: There has been an increase in gas, labor, food, supplies, and everything needed to operate the business have risen by 14% in one quarter. That increase is astronomical. In order to combat these increases, McDonald’s responded by increasing prices across their menu. This helped get McDonald’s revenue back up to 2016 type numbers, but at the end of the day will the price increases be sustainable if McDonald’s prices get closer to more “Mom and Pop” type of prices? My inclination is no.

Staff Shortages: There has been a big push by the current administration to show the increase of jobs, but it seems like more and more people want higher paying jobs that are remote and not in the restaurant or service industry. From my personal experiences, I see restaurants and grocery stores all over my city and in cities I travel too there’s a lot of “Now Hiring” signs at front and open tables with a wait because of staff shortages. This will hurt the business going forward if they cannot hire to keep up with the demand for the food.

Learn More and Stay Up to Date

Learn more about MCD here. Stay up to date on Green Candle by subscribing to our newsletter and following us on Twitter and Instagram! And don’t forget to join us in our Twitter Spaces Tuesday nights at 8 PM EST!

If you’re new to stock investing, check out our introduction to stock investing series:

Have a great week everyone,

Brandon & Dan

Disclosure: The article was written by Daniel Kuhman and Brandon Keys, and it expresses the author's own opinions. They are not receiving compensation for it. They have no business relationships with any company whose stock is mentioned in this article. The information presented in this article is for informational purposes only and in no way should be construed as financial advice or recommendation to buy or sell any stock. Brandon and Daniel are not financial advisors. We encourage all readers to do further research and do your own due diligence before making any investments.