Brief Breakdown: Taiwan Semiconductor Manufacturing Company (Ticker: TSM)

In my Brief Breakdowns,I pick a stock and present opposite sides – I present the bullish argument and the bearish argument.

Stay up to date with Green Candle Investments by following me on Twitter. Also join us for our Twitter spaces, every Tuesday we discuss our stock breakdown at 8 PM EST, & Friday we have a Bitcoin Happy Hour at 4:30 PM EST!

Company Description and Qualitative Analysis

Taiwan Semiconductor Manufacturing Company manufactures and sells semiconductors, integrated circuits, customer service, account management, and engineering services. The company operates in North America, Europe, Japan, China, and South Korea. As of December 2021, Apple was TSM’s largest customer and contributed 25.93% of the company’s revenue. Apple continues to use TSMC because of their latest and most advanced N5 and N5P nodes for hundreds of millions of its chips. The next two largest clients are MediaTrek and AMD, but both with less than 6% of TSMC’s revenue. As long as Apple remains a large customer, TSM will have a consistent and large source of revenue. Apple also seems like a company that may begin to develop their own chips out of necessity if issues arise, so this is something to monitor.

Quantitative Analysis

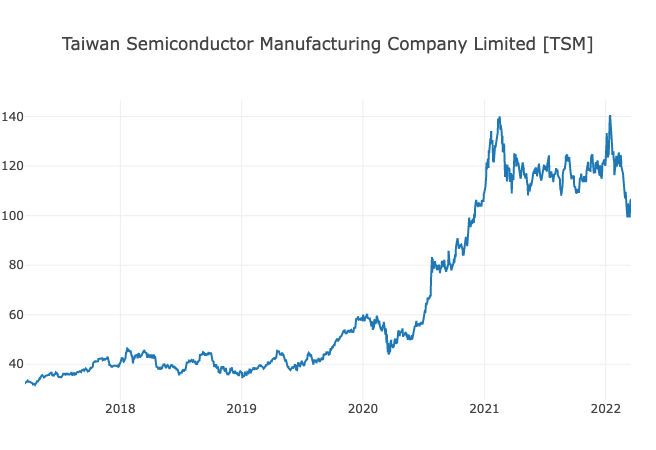

At the time of this writing (3/20/2022), TSM is trading at $106.72 with a 52 week range of $97.62 - $145.00 and a market cap of $553.43B USD. In Q4 of 2021, TSM posted a net revenue of $15.74 billion, gross margin of 52.7% and an operating margin of 41.7%. TSM has a price to earnings ratio of 26.16, net margin of 37.76%, ROE of 29.37%, and D/E ratio of 0.72. This financial analysis was done using financialstockdata.com (sign up using our promo code GCI here). You can view TSM’s last quarterly earnings here and latest 10K here.

Financial Stock Data allows users to analyze a company’s financials and qualitative factors such as leadership better than any other platform available. You can use the same tool as the pros for 50% off using our promo code GCI at checkout. Be sure to sign up for Financial Stock Data HERE.

Bullish Thesis

Here are three points to support the bullish thesis:

Growing Industry: Seemingly everything you interact with on a daily basis has some sort of screen or “smart” aspect on it, and this is a trend that seems to keep going. Semiconductors will be a vital part of the future and a vital part of the growing tech industry. TSM is set to succeed because of their history and ability to scale their chip manufacturing capabilities.

Supplier for Apple: Apple is a household name and one of the largest tech companies in the world. You would be hard pressed to walk into an average American household and NOT find a single Apple product in it. TSM being a large supplier for Apple means that as Apple grows and develops new products, TSM will have a consistent and reliable source of revenue. As Apple's products scale so will TSM’s sales and that is something you always like to see as an investor.

Reputation: By having a major client such as Apple, TSM has seemingly developed a reputation in the industry by making high quality semiconductors. This reputation will allow other potential consumers to know that TSM has a reliable and quality product. This is also a selling point for more clients and other companies to purchase and use TSM’s semiconductors in the future. Having one large customer can change the trajectory of a business dramatically.

Bearish Thesis

Here are three points to support the bearish thesis:

Supply Chain Issues: It seems as time has gone on during the COVID-19 pandemic there has been one constant: supply chain issues. Semiconductors are one of the largest industries affected by the supply chain issues and there is seemingly no end in sight. The semiconductor industry has caused the auto industry and many others to rapidly increase in price and in demand. If the semiconductor industry cannot figure out how to increase production, many large companies similar to Apple may start to develop their own chips and cut a company like TSM out.

Geopolitical Threat of China invading Taiwan: Unfortunately it is difficult to ignore the macro environment and geopolitical landscape when analyzing a company in the short to medium term. Currently there is a war between Russia and the Ukraine and rumblings of China potentially invading Taiwan. With TSM being based in Taiwan, it is difficult to see how a potential war or Chinese invasion could not negatively affect TSM in the short term. I for one hope that China does not decide to invade Taiwan and this is simply a talking point, but it is definitely a conflict to be aware of going forward.

Reliance on one major customer: A reliance on one major customer, although it is a tech giant like Apple, can be extremely beneficial or detrimental to a third party company such as TSM. TSM is at the whims of Apple’s decision making and with one change of supplier or if Apple decides to develop its own semiconductors, 25% of TSM’s revenue will now be gone. A major reliance on one customer is a large risk which can pay off but also can be detrimental if the large customer is unhappy.

Learn more about TSM here. Stay up to date on Green Candle by subscribing to our newsletter and following us on Twitter and Instagram! And don’t forget to join us in our Twitter Spaces tonight at 8 PM EST!

Video edition: Sunday Scaries Stock Talk

If you’re new to stock investing, check out our introduction to stock investing series:

Have a great week everyone,

Brandon

Disclosure: The article was written by Brandon Keys, and it expresses the author's own opinions. I am not receiving compensation for it. I have no business relationships with any company whose stock is mentioned in this article. The information presented in this article is for informational purposes only and in no way should be construed as financial advice or recommendation to buy or sell any stock. Brandon is not a financial advisor. I encourage all readers to do further research and do your own due diligence before making any investments.