Brief Breakdown: Under Armour Inc Class A (NYSE: UAA)

In our Brief Breakdowns, we pick a stock and take opposite sides – one of us presents the bullish argument and the other presents the bearish argument. If you haven’t already, subscribe to our newsletter here to get our articles directly to your inbox and follow us on Twitter and Instagram! Also join us for our Twitter spaces, every Tuesday we discuss our stock breakdown at 8 PM EST, & Friday we have a Bitcoin Happy Hour at 4:30 PM EST!

Video edition: Sunday Scaries Stock Talk

Company Description

Under Armour Inc. develops, markets, and distributes branded athletic apparel and footwear globally. Under Armour initially became well known for its compression and fitted-style apparel, but has since developed loose types of clothing and footwear for athletes in various sports. Recently, Under Armour developed a digital fitness subscription service and digital advertising through MapMyFitness. Under Armour has 439 brand and factory house stores, sells its products through various retailers, and direct to consumers through e-commerce websites.

Quantitative Analysis

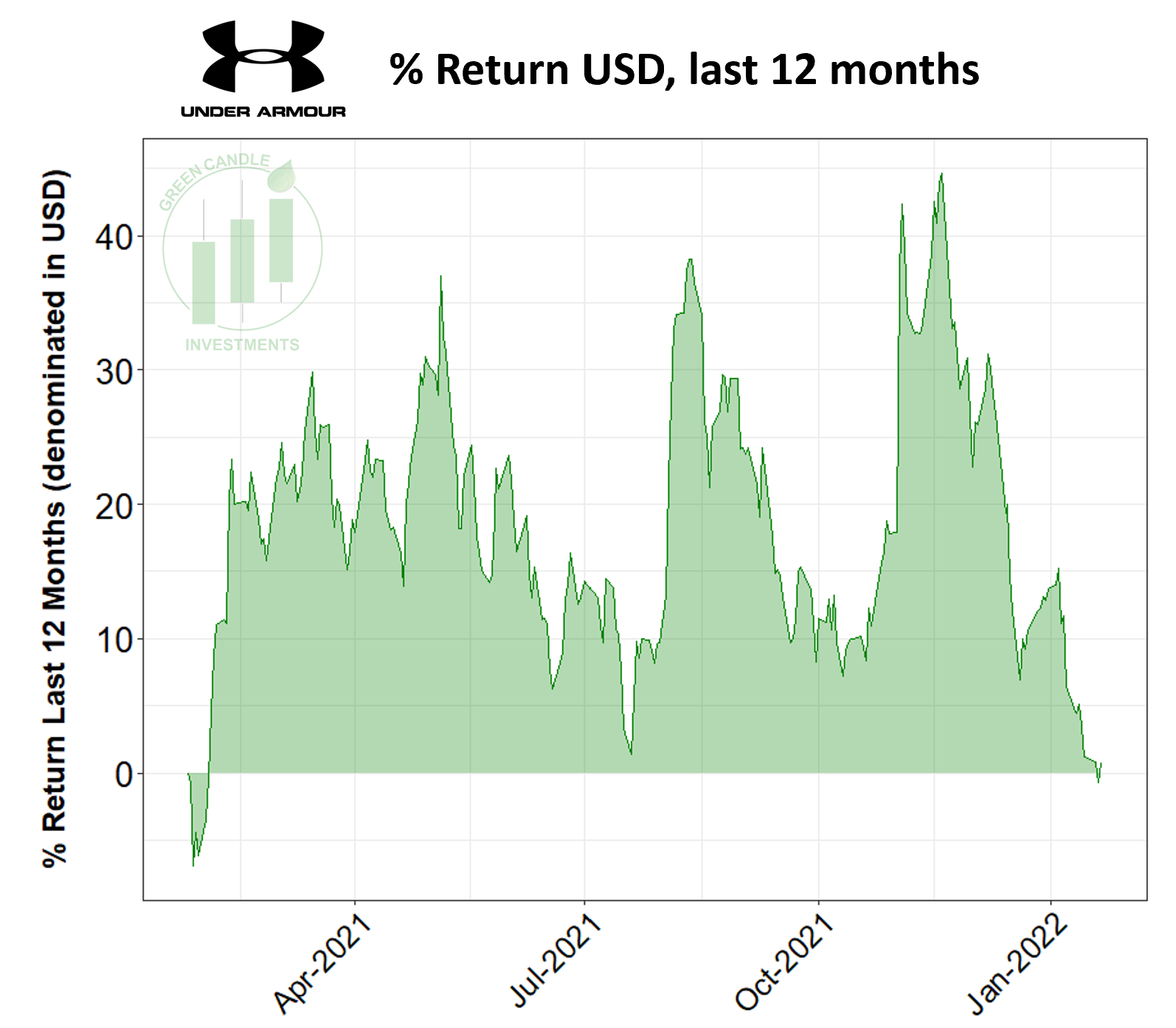

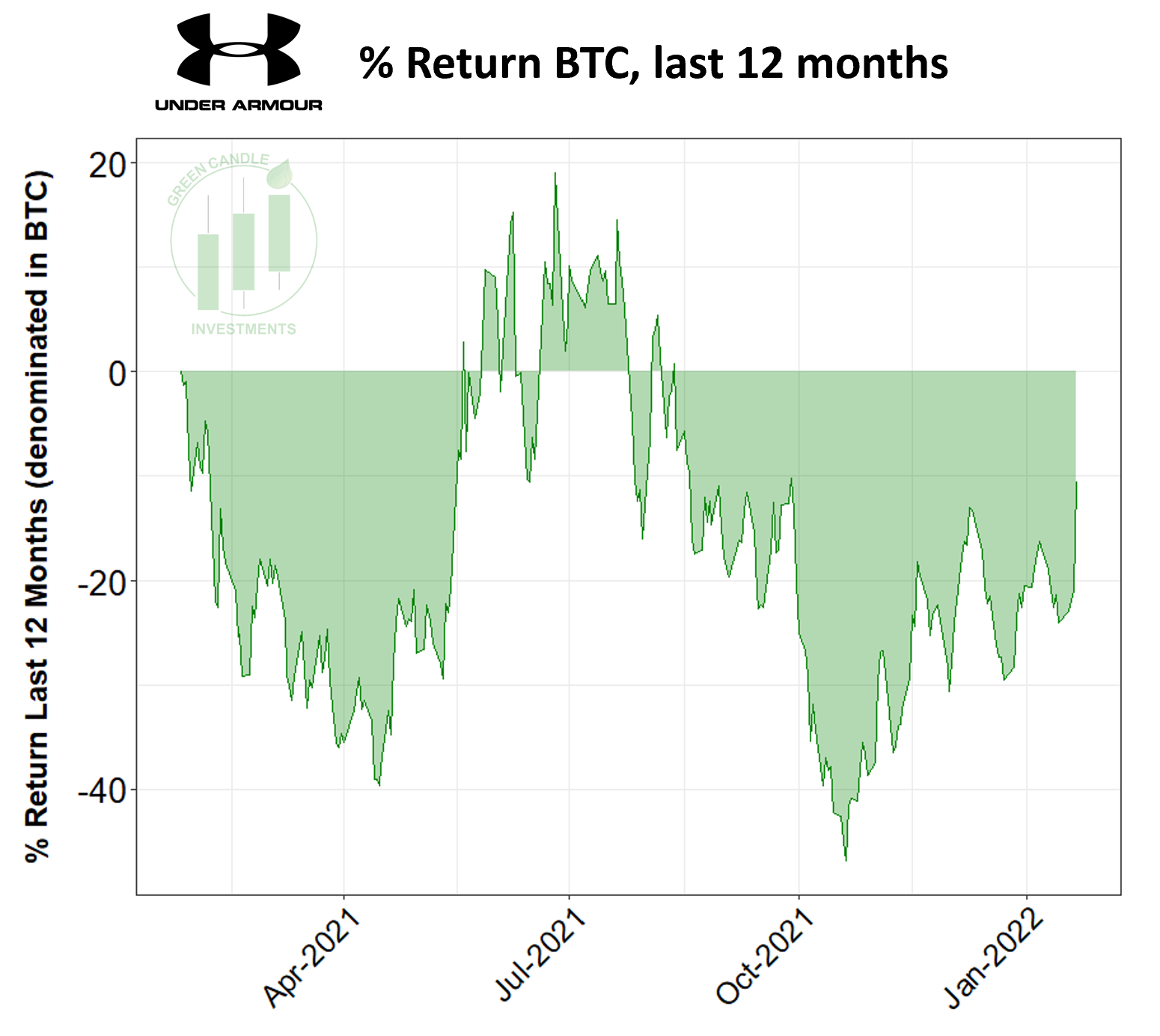

At the time of this writing (1/23/2022), UAA is trading at $18.77 with a 52 week range of $17.16 - $27.28 and a market cap of $8.29B. In Q3 of 2021, Under Armour’s revenue was up 8% year-over-year (YoY) to $1.5 billion and gross margin increased to 310 bases points to 51%. Operating income was $172 million and adjusted operating income was $189 million. Return of equity (ROE: Net Income / Total Equity *100) of UAA is 23.92% and net margin (net income / revenue) is 7.82%. The debt to equities ratio (total liabilities / total equity) is 1.44. This financial analysis was done using financialstockdata.com (sign up using our promo code GCI here). You can view UAA’s last quarterly earnings here and 2020 annual report here. Below we have percent returns denominated in both USD and in Bitcoin.

Financial Stock Data allows users to analyze a company’s financials and qualitative factors such as leadership better than any other platform available. You can use the same tool as the pros for 50% off using our promo code GCI at checkout. Be sure to sign up for Financial Stock Data HERE.

Qualitative Analysis

Under Armour is one of the largest sports and athletic wear retailers in the world and rose to popularity with its compression-style athletic wear. It now sponsors world famous athletes, most notably Steph Curry of the Golden State Warriors (NBA) and Tom Brady of the Tampa Bay Buccaneers (NFL), and various collegiate athletic programs in the United States. Under Armour has shot up in popularity and is releasing new kinds of athletic wear, which customers can purchase both through in-person retail and through direct to consumer e-commerce platforms. The growing popularity of athleisure clothing and the popularity of Under Armour for the quality of their clothing has helped UAA in the short term. However, the CEO insists that Under Armour is not an athleisure company and will primarily focus on developing their performance products (you can read more on this here).

Bullish Thesis

Here are three points to support the bullish thesis:

Recent Restructuring: In 2019 Patrik Frisk took over as chief executive of Under Armour after Founder Kevin Plank stepped down. Just a year after Frisk became CEO, he instituted a large restructuring plan, yielding a significantly "cleaner" expense base. The 2020 restructuring plan involved charges of $550 to $600 million to cover a variety of costs, including lease terminations, severance packages, and asset impairments. According to Seeking Alpha, “the restructuring plan was implemented to rebalance their cost base, to improve profitability, and to improve cash flow.” If this plan works out, Under Armour may regain the momentum they had in 2013-2015.

Redistributing Sourcing: Post-pandemic economic recovery has been stifled by a number of factors, including supply chain disruptions. Recognizing the importance of reducing potential bottlenecks in their supply chain, Under Armour has redistributed their sourcing. For example, from 2013 to 2018, Under Armour reduced their sourcing from China from 46% down to 18% and expects to reduce to 7% by 2023. In fact, by 2023, Under Armour expects that no one country will account for more than 25% of their sourcing. With this redistribution, they reduce potential bottlenecks in their supply chain - for example if economic instability or uncertainty causes slowdowns in one country, it will have less of an effect on Under Armour’s supply chain.

Household Brand: Under Armour is a well-established brand with a history of producing quality apparel. According to a September 2021 report by Footwear Distributors & Retailers of America, Under Armour overtook Adidas in combined apparel and footwear sales to become the second biggest sports brand in the United States (behind Nike). Their brand familiarity, history of success, and market performance should have investors bullish on Under Armour.

Bearish Thesis

Here are three points to support the bearish thesis:

Large Marketing Costs: Similarly to Nike (which we broke down last week, you can find that here) athletic apparel companies sponsor individual athletes, sports teams, collegiate programs, and even athletic leagues. Although these sponsorships bring publicity and allow UA to sell branded and licensed apparel, this comes at a very large cost. Recently Under Armour attempted to back out of their 15 year $280 million dollar deal with University of California Los Angeles (UCLA) and now the university is suing Under Armour for damages. Not only is there a large cost on marketing all of these athletes and teams, UA is also having increased cost in lawyer fees due to the recent lawsuit.

Increased Competition: Although UA is focusing on performance rather than athleisure type clothing, more and more companies are producing athletic type clothing. Under Armour also has stiff competition with long standing companies like Nike and Adidas and has to play catch up with those two giants. The competition with these large players will force UA to spend more on marketing as they will be continually be playing catch up. It will take something big in order for UA to surpass Nike and Adidas.

Lack of Focus on Athleisure: I do not necessarily believe you always need to follow trends because sometimes focusing on trends that do not last can be detrimental to the business, but the athleisure trend is different. The comfortable athletic type clothing movement is here to stay because there’s been an increase in “business casual” type clothing and remote works popularity has people wearing more comfortable type clothing. By ignoring this trend, at least for now, will lead to loss in potential sales and UA will be playing catch up in this sector of the industry as well.

Learn more about UAA here. Stay up to date on Green Candle by subscribing to our newsletter and following us on Twitter and Instagram! And don’t forget to join us in our Twitter Spaces tonight at 8 PM EST!

If you’re new to stock investing, check out our introduction to stock investing series:

Have a great week everyone,

Brandon & Daniel

Disclosure: The article was written by Daniel Kuhman and Brandon Keys, and it expresses the author's own opinions. They are not receiving compensation for it. They have no business relationships with any company whose stock is mentioned in this article. The information presented in this article is for informational purposes only and in no way should be construed as financial advice or recommendation to buy or sell any stock. Brandon and Daniel are not financial advisors. We encourage all readers to do further research and do your own due diligence before making any investments.