International Business Machines Corporation (Ticker: IBM) - Brief Breakdown

In our Brief Breakdowns, we pick a stock and take opposite sides – one of us presents the bullish argument and the other presents the bearish argument.

If you haven’t already, subscribe to our newsletter here to get our articles directly to your inbox and follow us onTwitter and Instagram!

Company Description

International Business Machines Corporation (IBM) is an American technology company that produces and sells computer hardware, middleware and software, and provides hosting and consulting services in areas ranging from mainframe computers to nanotechnology. IBM also has a cloud and cognitive software segment that offers vertical and domain-specific solutions in health, financial services, Internet of Things (IoT), weather, and security software and services application areas. Another sector of IBM offers customer information control system and storage, and analytics and integration software solutions to support client mission critical on-premise workloads in banking, airline, and retail industries. IBM is also a major research organization and holds the record for most annual U.S. patents generated by a business for 28 consecutive years. IBM was founded in 1911 and has been a public company since its creation.

Quantitative Analysis

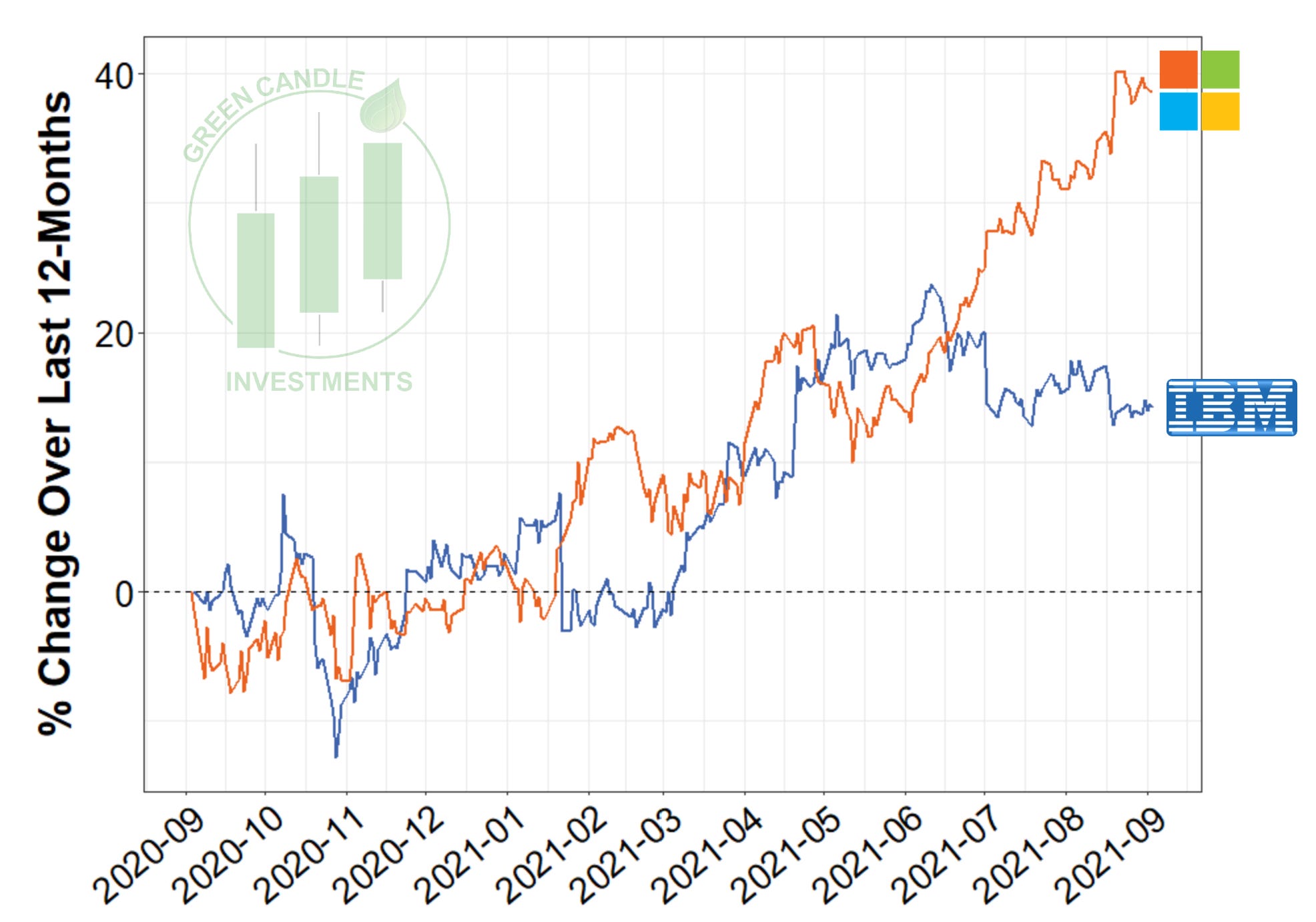

At the time of this writing (9/06/2021), IBM is trading at $139.58 with a 52 week range of $105.92 - $152.84 and a market cap of $125.11B. In Q2 of 2021, IBM’s revenue grew to $18.7 billion, up 3% with the cloud & cognitive software up 2% and global business services up 7% year over year. Total cloud revenue over the last 12 months was $27 billion, up 13% from the previous year. Return of equity (ROE: Net Income / Total Equity *100) of IBM is 24.9%, the price to earnings ratio (P/E) is 23.59, and net margin (net income / revenue) is 7.17%. This financial analysis was done using financialstockdata.com (become a beta tester here). You can view IBM’s 2021 Q2 earnings here and their 2020 Annual Report here.

Qualitative Analysis

IBM has been a major player in the global tech industry for longer than many of the big name technology companies have been around. In April of 2020, Arvind Krishna became chairman and chief executive of IBM. He prioritized building an open hybrid cloud platform with a focus on artificial intelligence technology. IBM provides its customers with both public and private cloud options to give companies extra network security. IBM completed 2 acquisitions in 2020, with a total cost of $723 million and 3 more acquisitions in Q1 of 2021 with a total cost of $987 million. Through both internal development and external acquisitions, Krishna has made a strong push to reshape IBM’s future with a cloud and AI focus. Prior to the change in leadership, IBM had not seen significant growth and seemed to be behind the industry in innovation, particularly in the cloud sector. With Krisna at the helm, it will be interesting to see whether IBM can compete with the other tech giants of the world (e.g., Microsoft, Apple, Amazon).

Bullish Thesis

Here are three points to support the bullish thesis:

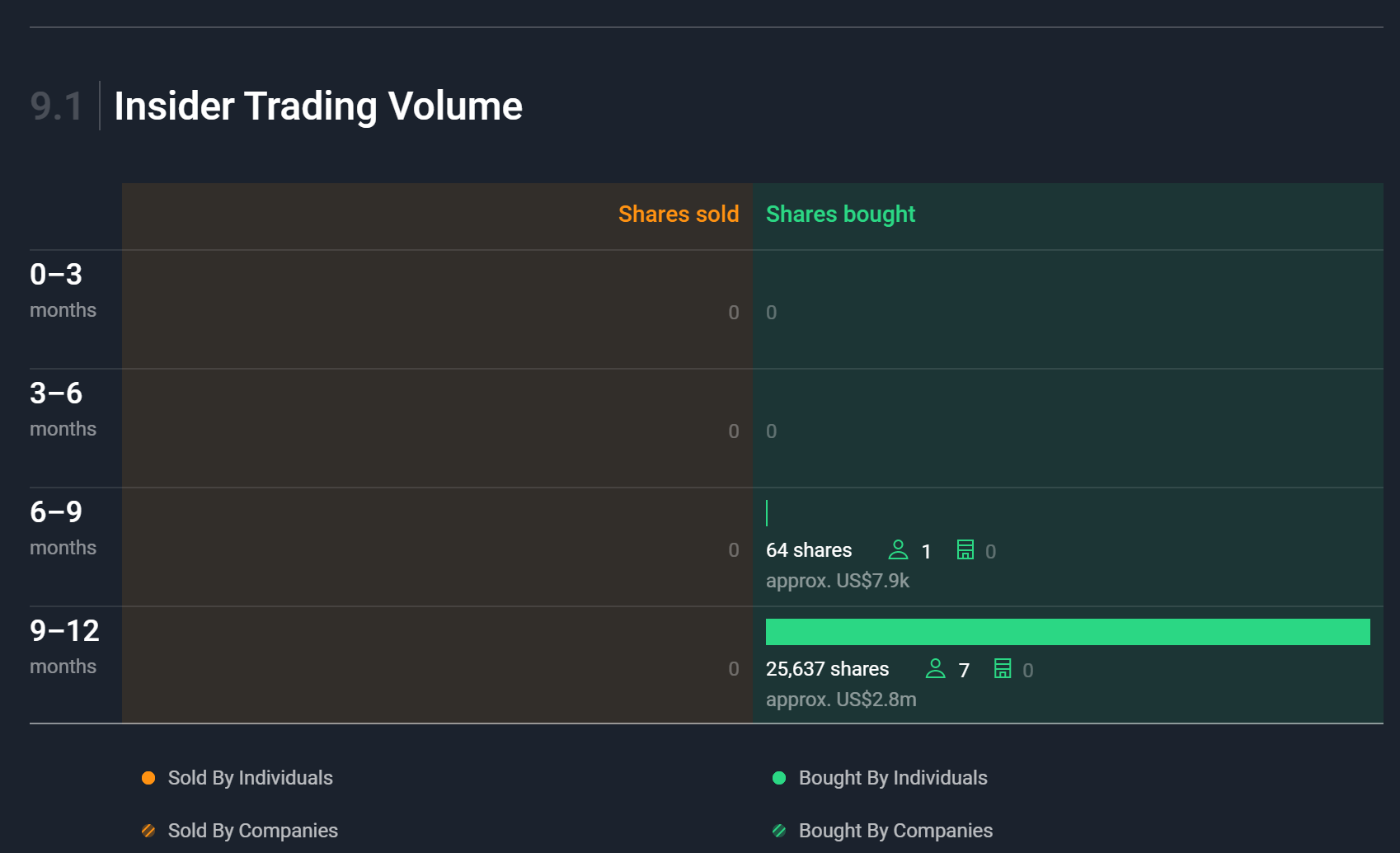

Recent Insider Buying: According to simplywall.st, insider buying at IBM has been significant over the last 12 months. Indeed, over this time period, insiders have purchased ~$2.8M worth of IBM stock. Substantial stock purchases from directors, officers, and executives within the company signals that they believe the stock is undervalued (or, at least it was when the purchases were made). The average price of IBM stocks 9-12 months ago (Sep 2020 - Dec 2020) was ~$121 +/- ~$5. The current price of $139.58 is ~15% higher than the average price from 9-12 month ago. Lack of insider buying in the last 6 months may indicate that the higher ups now believe the stock is priced appropriately. However, according to simplywall.st, their data over the last 3 months is insufficient for accurate reporting. This will be something to keep an eye on going forward - if the insider buying trend continues, investors may want to consider joining them.

A CEO Focused on Cloud Management: In January 2020 IBM appointed longtime employee Arvind Krishna as CEO. Krishna joined IBM in 1990 and spent his first 18 years with the company working in the Watson Research Center. In 2015 he became senior VP of IBM Research and was then promoted to senior VP of IBM’s cloud and cognitive software division. He is seen by many to be the driving force behind IBM’s 2019 acquisition of Red Hat, a world-leading open-source software company. As CEO, Krishna has made it clear that his focus is going to be on transforming IBM into a hybrid cloud management vendor moving forward. Although IBM lags other major companies in this sector, I can’t think of a better person to help IBM play catch-up - Krishna knows IBM inside and out and has devoted much of his life to research in the cloud management space.

Healthy Dividends: Although we typically try to keep our arguments in the macro space, we’d be remiss not to mention IBM’s history of healthy dividends. IBM has raised its dividend payouts for 25 years and currently boasts a yield of ~5%. With a payout ratio of over 50%, its dividend is well-covered by its earnings. Dividends mean more to some investors than others, but it’s hard to argue against a 5% yield.

Bearish Thesis

Here are three points to support the bearish thesis:

Declining Brand Power: IBM is a tech giant and has been around since 1911, but their brand power has been declining as the company has lacked innovation for some time. Because of IBM’s longevity they have had a consistent set of products but now other technology companies are entering the field and taking away from IBM’s chip sector which has forced IBM to pivot in order to survive and grow. As highlighted in the qualitative analysis and in the bull arguments, the current CEO is now focused on cloud computing and AI, but this required IBM to make 11 acquisitions in the past 5 quarters which proved to be costly. It will take time for IBM to crack into Amazon, Google and the other major players in the cloud computing space, but hopefully the growing demand will leave room for IBM going forward.

Expert in “Old” Tech: Other than IBM’s artificial intelligence offering with Watson, it is mostly viewed as an “old” tech company compared to its competitors. IBM does not have the reputation of being an innovative company and that can affect obtaining new clients in their attempt to grow cloud computing and AI sectors. There is a large need for cloud computing and growing demand for AI, but major competitors like Amazon and Google have unbelievable brand power, growth, and have increasing revenue to deploy towards marketing while IBM is in the developmental phase of cloud computing and AI.

Lack of Consistent Growth: Because of IBM’s reputation as an old tech company and its need to acquire companies in the cloud computing and AI space, IBM has seen a lack of consistent growth in revenue. IBM generated revenues of around $70 billion which is actually down 10% over the past five years. Its competitors are growing at a rapid pace and it seems as if IBM is playing catch up which will require either acquiring companies which it is currently doing or investing heavily in development teams. Either solution will require time to get integrated in IBM’s core business while many competitors in the space already have in place.

Learn more about IBM here. Stay up to date on Green Candle by subscribing to our newsletter and following us on Twitter and Instagram!

If you’re new to stock investing, check out our introduction to stock investing series:

Have a great week everyone,

Brandon & Daniel

Disclosure:

The article was written by Daniel Kuhman and Brandon Keys, and it expresses the author's own opinions. They are not receiving compensation for it. They have no business relationships with any company whose stock is mentioned in this article. The information presented in this article is for informational purposes only and in no way should be construed as financial advice or recommendation to buy or sell any stock. Brandon and Daniel are not financial advisors. We encourage all readers to do further research and do your own due diligence before making any investments.