PayPal Holdings Inc. (Ticker: PYPL) - Brief Breakdown

In our Brief Breakdowns, we pick a stock and take opposite sides – one of us presents the bullish argument and the other presents the bearish argument.

If you haven’t already, subscribe to our newsletter here to get our articles directly to your inbox and follow us onTwitter and Instagram!

Company Description

Paypal Holdings Inc. (NASDAQ Ticker: PYPL) is an American financial services and digital payments company that provides a platform for electronic money transfers. PayPal serves as an electronic alternative to traditional paper methods like checks and money orders as it operates as a payment processor for online vendors, auction sites, and many other commercial users. PayPal also owns the popular peer-to-peer money transfer app, Venmo. PayPal’s top competition is Square (NASDAQ: SQ), which we broke down last week. PayPal, similar to Square, now allows its users to buy, sell, and hold Bitcoin on its platforms. PayPal also recently acquired the web browser extension Honey Science, a relatively seamless extension that automatically applies coupon and discount codes during online purchasing, helping shoppers save money.

Quantitative Analysis

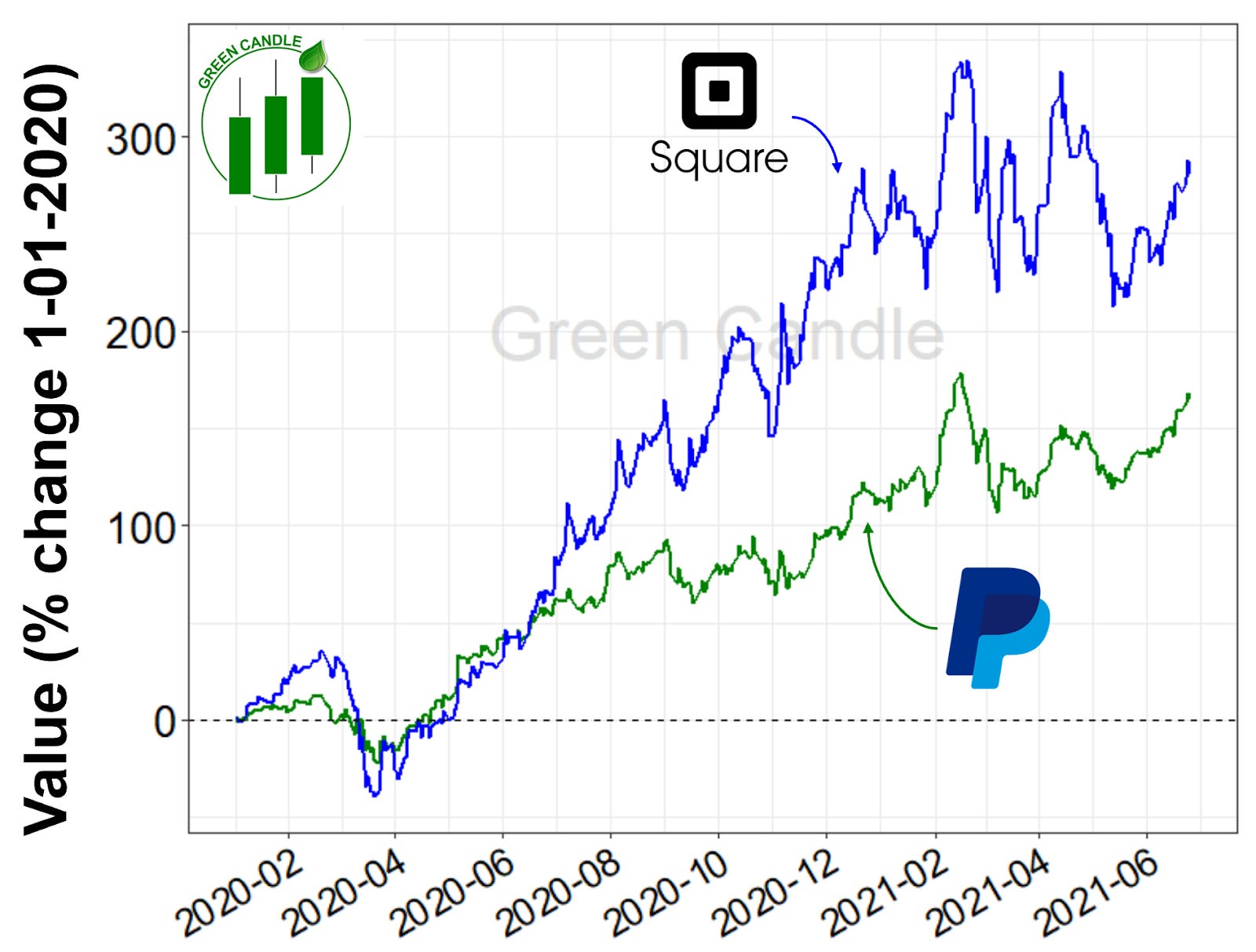

At the time of this writing (6/27/2021), Paypal is trading at $289.60 with a 52 week range of $164.33 - $309.14 and a market cap of $340.2B. In Q1 of 2021, PayPal’s net revenue was $6.03B, representing a 29% year-over-year increase. On top of increased revenue, their free cash flow increased by 27%! They posted an operating income of $1.04B in generally accepted accounting principles (GAAP), which is a 162% year-over-year increase. PayPal’s earning per share has skyrocketed, hitting $0.92 in Q1 of 2021, representing a whopping 1200% year-over-year increase. The return of equity (ROE: Net Income / Total Equity *100) of PayPal is 27.58%, the price to earnings (P/E) ratio is 60.0, and the Net Margin (Net Income / Revenue) is 22.8%. PayPal’s stock went from ~$91.46 in March of 2020 to $309.14 in February of 2021. Similarly to Square, PayPal’s stock price has roared over the last year, shooting up ~300% since the low in March 2020! This financial analysis was done using financialstockdata.com (become a beta tester here). You can view PayPal’s 2021 Q1 earnings here and PayPal’s 2020 Annual Report here.

Qualitative Analysis

PayPal was the first web-based online payment platform that allowed small businesses to operate entirely online. Although the negative effects of COVID-19 may have affected small businesses drastically, it seems like PayPal’s model for online payments may have benefitted. PayPal has recurring customers, is a large income generator through its online platform, and is expanding. Venmo was the first peer-to-peer transfer application on the market, giving it a “first to market” advantage over newer apps. Such an advantage forces industry competitors like Square (which we broke down last week) to spend heavily to attract users (e.g., on marketing and R&D for platform innovation). While the “first to market” advantage is beneficial in the short term, it can cause some companies to become complacent. Indeed, PayPal has had to play to catch up with competitors in some respects. For example, PayPal began allowing users to trade Bitcoin last November and only recently rolled out a crypto feature in Venmo in April (2021) whereas Square implemented these features in 2018. Despite pressure from competitors, PayPal’s head start has allowed it to maintain a sizable advantage in payment volume and earnings over Square. PayPal recently acquired Honey, a browser extension that automatically applies discount codes during online shopping. Although Honey (as of now) is a free service, it will provide PayPal a data stream of consumer shopping habits. PayPal has been a leader in the financial tech space since the start of the internet and it looks to continue that trend moving forward.

Bullish Thesis

Here are three points to support the bullish thesis:

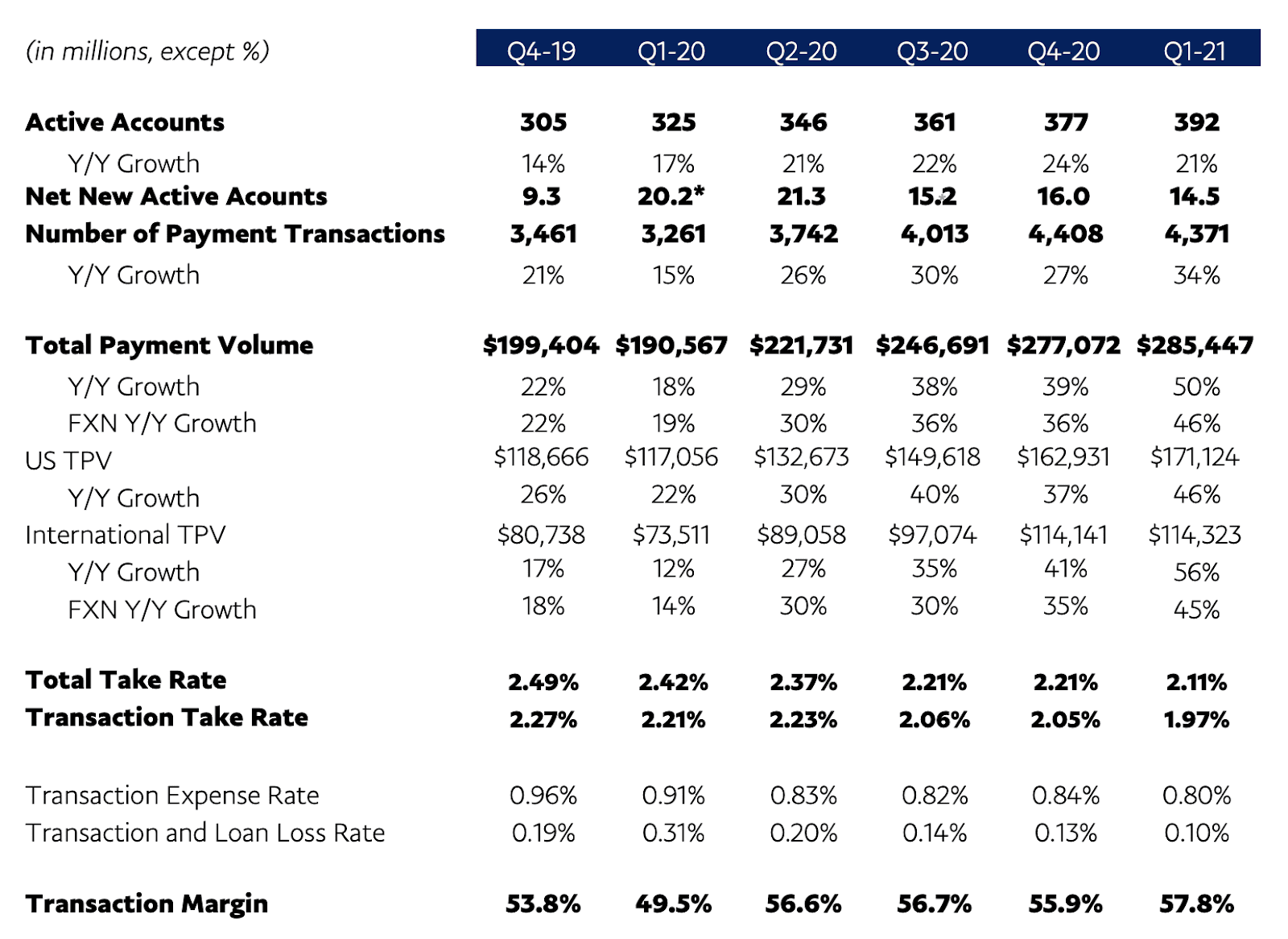

Longevity: PayPal was created in 1998 and is now one of the largest companies in America. In Q1 of 2021, PayPal added 14.5 million accounts bringing the total accounts to 392 million. As more and more transactions are becoming strictly digital, PayPal has established customers and is continuing to grow. PayPal has also moved into the younger generation with the widely successful mobile phone application Venmo. PayPal’s total payment volume was $285 billion in Q1 of 2021, up 50% on a spot basis. Merchant services also grew 54% and represented 94% of the total pay volume which gives a great base and allows PayPal to expand into different avenues and earn revenues elsewhere.

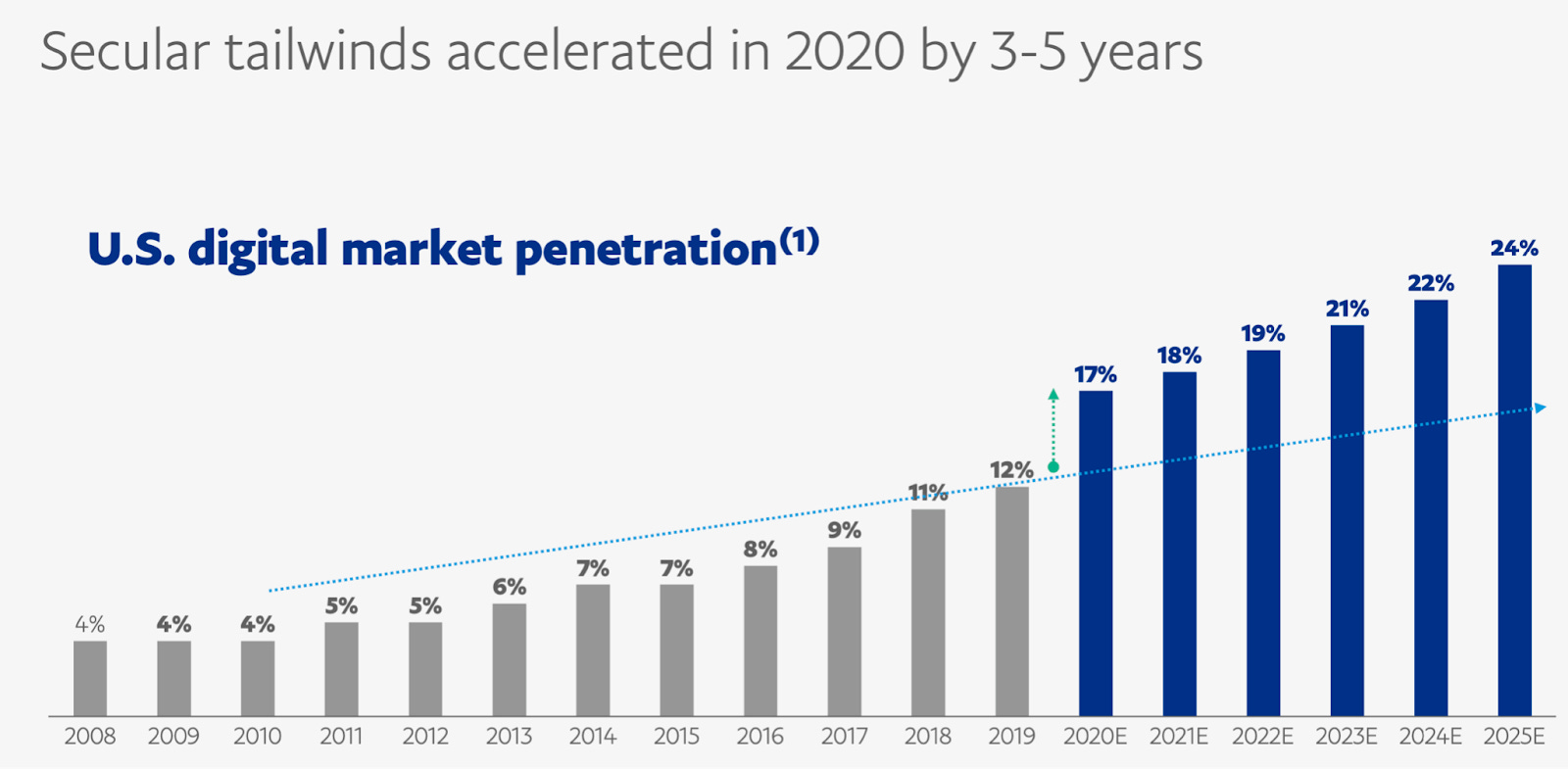

Growing Digital Market: PayPal currently has approximately a 17% market share of the U. S. digital transactions and took a large jump in the market share in 2020. The digital market is growing exponentially due to the COVID-19 pandemic forcing many companies to go online retail. The amount of ecommerce sales has risen to over $600 billion in 2020 and PayPal has the ability to grow its market share within a rapidly growing industry. PayPal already has steady growth in its merchant services and that has shown consistent growth, showing that PYPL still has room to grow in that sector. The digital market looks ripe for the taking!

Network Effect: Businesses who use PayPal convert 60% of consumers of their business into PayPal users. PayPal has a built in network effect that has businesses who use their services. Also the use of the peer-to-peer services like Venmo require both users to have the application to send and receive money which can keep increasing the user base of both PayPal and Venmo. Now with the addition of cryptocurrencies on all of PayPal’s platforms some may go to their platform strictly for buying, selling, or trading cryptocurrencies. Although there are plenty of places to buy, sell, and trade crypto, PayPal has millions of existing users that can now interact more with the platform. This sector is rapidly growing and with a large existing network, PayPal can now keep more user’s capital on their platform.

Bearish Thesis

Here are three points to support the bearish thesis:

Increased industry competition: As stated throughout this breakdown, PayPal currently enjoys a “first to market” advantage over emerging industry competitors like Square. This advantage has allowed PayPal to maintain a substantially larger user base than their competitors. For example, it currently boasts 392 million active accounts, much more than Square’s ~30 million. However, although they’re larger than competitors now, they seem to be losing momentum. Net new active accounts slowed through the final two quarters of 2020 and continued to slow through Q1 of 2021. Payment systems can be difficult to change for small businesses, which can allow “first to market” products to become embedded in the market. However, COVID-related business closures may have given small businesses the time needed to reassess their options. Additionally, their relative lack of innovation in the peer-to-peer transaction space should give investors pause. For example, Square’s CashApp beat Venmo to crypto integration by ~2 years.

Processing fees: PayPal recently announced that it would raise their processing fees for online merchants by ~0.5% (from its current rate of 2.9% to 3.49%) beginning in August of this year. Analysts overwhelmingly interpreted this announcement as a positive in that it showed PayPal’s pricing power. However, while PayPal is counting on their “stickiness” with current users, the hike in processing fees may continue to slow their already diminishing new active accounts growth. Post COVID, many small businesses will look to play catch up after a year of forced shutdowns and lower capacity operations. To do so, they may opt for payment systems with lower transaction fees. If this happens, look for their competitors (Square, Apple Pay, etc.) to continue to eat up PayPal’s market share. Investors should pay close attention to PayPal’s user count through Q4 of 2021 and Q1 of 2022.

Complacency: PayPal is heavily reliant on the stickiness of their products with current users and less concerned about developing their products to draw in new users. Their competitors, on the other hand, are doing everything in their power to catch up. In my opinion, their competitors should focus on simplifying onboarding of new users (particularly merchants) and on facilitating transferrals from alternative systems (e.g., transferring a business from PayPal to Square). If PayPal’s competitors can continue to gain new users AND begin to pull users away from PayPal’s platforms, look for PYPL stock to struggle. On a personal note, I use both Venmo and CashApp and have been much more satisfied with CashApp’s UI/UX.

Learn more about PayPal Holdings Inc. here. Stay up to date on Green Candle by subscribing to our newsletter and following us on Twitter and Instagram!

Have a great week everyone,

Brandon & Daniel

Disclosure: The article was written by Daniel Kuhman and Brandon Keys, and it expresses the author's own opinions. They are not receiving compensation for it. They have no business relationships with any company whose stock is mentioned in this article. The information presented in this article is for informational purposes only and in no way should be construed as financial advice or recommendation to buy or sell any stock. Brandon and Daniel are not financial advisors. We encourage all readers to do further research and do your own due diligence before making any investments.