Peloton Interactive Inc. (Ticker: PTON) - Brief Breakdown

Peloton Interactive Inc. (Ticker: PTON) - Brief Breakdown

In our Brief Breakdowns, we pick a stock and take opposite sides – one of us presents the bullish argument and the other presents the bearish argument.

If you haven’t already, subscribe to our newsletter here to get our articles directly to your inbox and follow us onTwitter and Instagram!

Company Description

Peloton Interactive Inc. is an exercise equipment and media company based in the United States. Peloton offers stationary bikes and treadmills which include interactive touchscreens that stream live and on-demand classes, allowing people to remotely participate in fitness classes. In order to join the classes, every participant must pay a monthly membership fee on top of the cost of the equipment. Customers can also purchase a monthly subscription to the website or mobile application and access classes that do not need a piece of Peloton exercise equipment. Peloton is also in the process of bringing in-person classes to New York City.

Quantitative Analysis

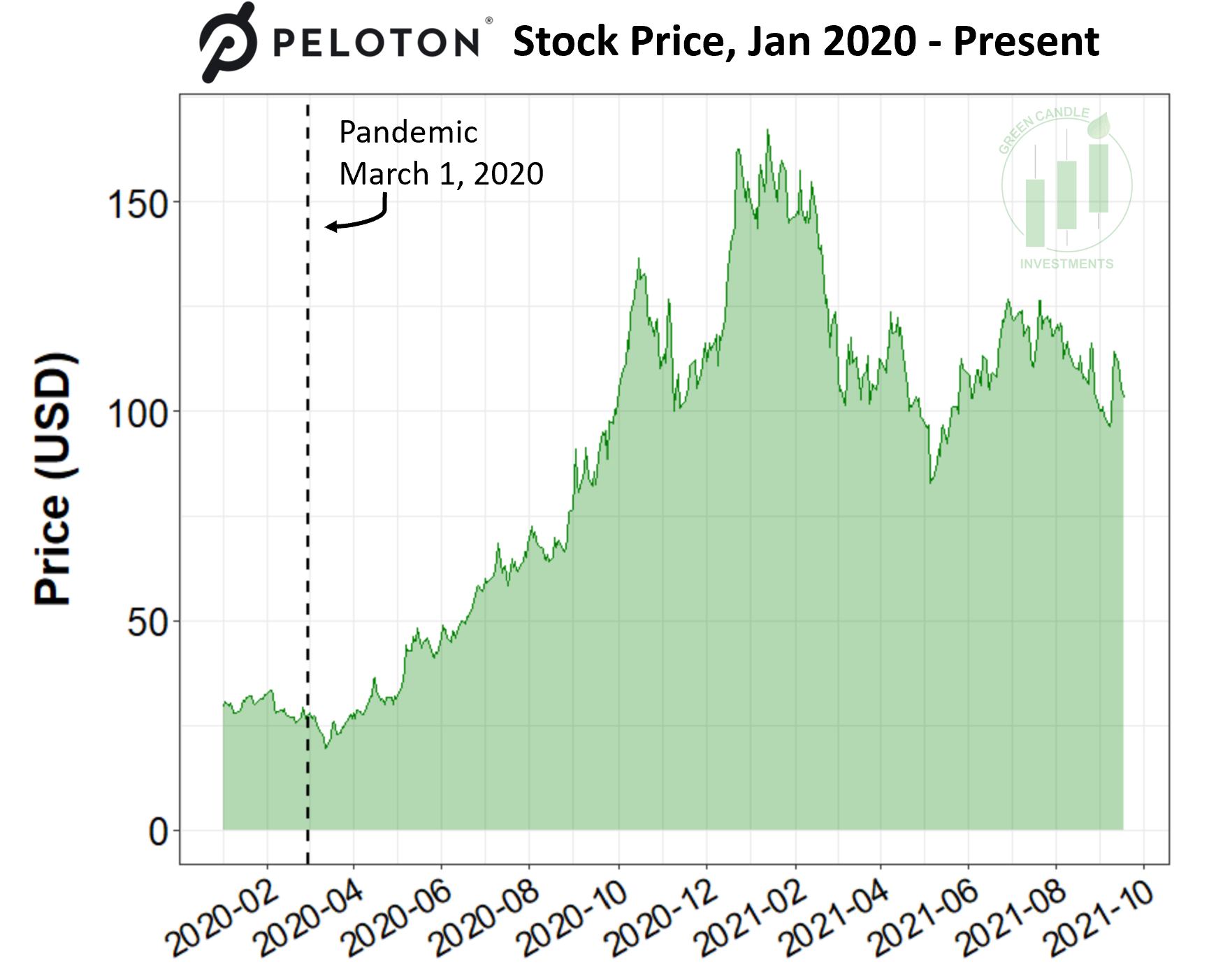

At the time of this writing (9/20/2021), PTON is trading at $103.42 with a 52 week range of $80.48 - $171.09 and a market cap of $31.08B. In Q4 of their fiscal year 2021, PTON’s revenue grew to $937 million, up 54% year over year. Q4’s net loss was $313.2 million and $1.05 per diluted share. Return of equity (ROE: Net Income / Total Equity *100) of PTON is -10.14% and net margin (net income / revenue) is -4.71%. This financial analysis was done using financialstockdata.com (become a beta tester here). You can view PTON’s 2021 Q4 earnings here and their 2020 Annual Report here.

Qualitative Analysis

Similar to Zoom, Peloton took off during the COVID-19 pandemic with people working from home and unable to go to physical gyms. Peloton experienced massive initial growth and popularity. In Q4, the amount of connected fitness subscriptions grew by 114% to 2.33 million and paid digital subscriptions grew 176% to over 874k, with total members over 5.9 million. Although gyms and workout classes are opening throughout the country, Peloton is still increasing its subscription base and has built a strong digital community with its subscribers. Peloton has 1.6 million followers on instagram and many of their certified coaches have thousands of followers individually. This interactive audience will keep subscribers and retain customers which is shown in their 92% retention rate in Q4. Eventually, the manufacturing will not be as needed for the business as more people own Peloton’s interactive equipment and will be consistent subscribers.

Bullish Thesis

Here are three points to support the bullish thesis:

Digital Disruption in the Fitness Industry: Technological disruption is well on its way in many industries. Services like Netflix, Hulu, and YouTube disrupted the traditional media and entertainment industry. Services like Zoom, Microsoft Teams, and Slack are disrupting the traditional workplace and allowing companies to operate with remote employees. Services like Uber, Lyft, and DoorDash have disrupted the transportation and food delivery industries. Peloton represents the technological disruption of the fitness industry, a space that has been steadily growing over the last decade. According to Statista, in 2019 market size of the global health club industry reached $96.7B, up from $67.2B in 2009 (~44% increase). If Peloton can be as successful in the fitness industry as their disruptor-peers have been in other industries, be prepared to see the company’s value skyrocket as they eat up market share in the growing fitness space.

Strong Brand Loyalty: We often talk about product/service “stickiness” and the value of creating things that customers use on a daily basis. Stickiness and brand loyalty are particularly important in areas where onboarding new customers is expensive. The relatively high prices on Peloton’s equipment make it difficult to attain new customers. It is therefore vital for Peloton to retain existing customers and work to make their equipment more affordable. As noted above, in Q4 of 2021 Peloton had a 92% customer retention rate, which is well ahead of traditional fitness studios/gyms. Indeed, according to the Association of Fitness Studios (AFS), the average studio retention rate is 75.9%. Now that they’ve nailed customer retention, I'd like to see them streamline product development and bring equipment costs down.

Post-pandemic Health Consciousness: The COVID-19 pandemic put health at the forefront of many people’s minds. As more data is released, it is becoming clear that obesity is a major risk factor in COVID patients. One recent study found that, in COVID patients, extremely high BMIs (45 or greater) were linked with a 61% increased risk of death and a 33% increased risk of hospitalization compared with healthy weight patients. If these trends are taken seriously by the general public, an increased focus on health and fitness could open up a huge market for Peloton and should keep investors bullish.

Bearish Thesis

Here are three points to support the bearish thesis:

Not Profitable: Although many tech companies do not make a profit, it is interesting that Peloton does have enough revenue to account for its overhead costs. This might be a short term worry though because once Peloton gets enough subscribers it can then have enough monthly revenue to pay for its overhead costs, but the need to get enough equipment in households to reach that threshold may prove to be costly. Peloton became known for extreme delays in their supply chain causing orders to be months late for the delivery of their equipment which could hinder its brand power in the short term.

Delays in Interactive Treadmill: There were reports of dozens of injuries and a child death with the Peloton Treadmill pulled under the Tread+. This caused Peloton to voluntarily recall their treadmill and have many questioning their ability to create interactive products safely other than their stationary bike. The more interactive the equipment becomes the more dangerous it may be. For example, if the treadmill changes speeds because of the connected workout, someone might not expect the change or might not be able to handle increased speeds thus causing injuries. It is difficult to implement this feature with the stationary bike and with increased difficulty to pedal is not as dangerous as increasing speed on a treadmill.

Need to Lower Cost of Equipment: Peloton has seen a need to lower the costs of their interactive products which already have low margins. The hope is that purchasers of the interactive equipment will become subscribers to help with monthly revenue but will put an initial cost in customer acquisition. The lower the cost of customer acquisition the better for any company and Peloton has determined that their ideal price for the interactive products will be more affordable to reach a larger audience. It will be interesting to see how much this will help Peloton’s growth, if it will allow more people to purchase but at what cost? Will the low margins hinder the long term growth because of the initial upfront costs or will Peloton be able to manage the increased customer acquisition cost and will be beneficial for long term growth?

Learn more about Peloton here. Stay up to date on Green Candle by subscribing to our newsletter and following us on Twitter and Instagram!

If you’re new to stock investing, check out our introduction to stock investing series:

Have a great week everyone,

Brandon & Daniel

Disclosure:

The article was written by Daniel Kuhman and Brandon Keys, and it expresses the author's own opinions. They are not receiving compensation for it. They have no business relationships with any company whose stock is mentioned in this article. The information presented in this article is for informational purposes only and in no way should be construed as financial advice or recommendation to buy or sell any stock. Brandon and Daniel are not financial advisors. We encourage all readers to do further research and do your own due diligence before making any investments.