Samsung Electronics Co (Ticker: SMSN) - Brief Breakdown

In my Brief Breakdowns,I pick a stock and present opposite sides – I present the bullish argument and the bearish argument.

If you haven’t already, subscribe to our newsletter here to get our articles directly to your inbox and follow us on Twitter and Instagram! Also join us for our Twitter spaces, every Tuesday we discuss our stock breakdown at 8 PM EST, & Friday we have a Bitcoin Happy Hour at 4:30 PM EST!

Company Description and Qualitative Analysis

Samsung Electronics Co. is a consumer electronics, information technology, mobile communications, and device solution company that specializes in appliances, TVs, smartphones, tables, watches, and much more! Samsung also provides medical equipment, software, processes semiconductors and display panels, logistics, financing, marketing, consulting, installation and optimization, and seemingly everything surrounding electronics. Samsung was founded in 1938 and is based in South Korea. Samsung is an electronics giant that has expanded into seemingly every single sector. It has such a wide range of products and services that Samsung seemingly has so many revenue streams it will be very difficult to crack.

Quantitative Analysis

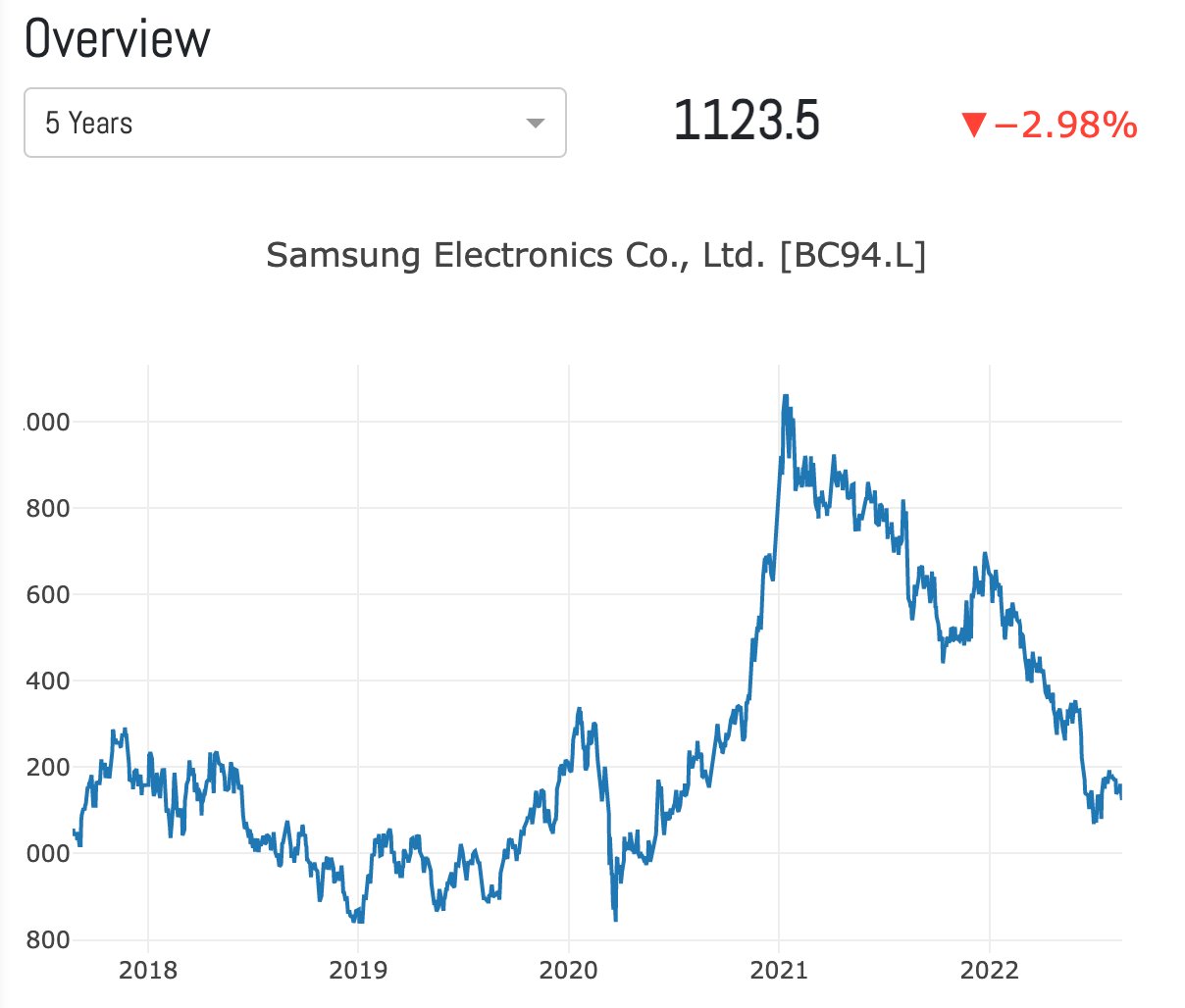

At the time of this writing (8/21/2022), SSNLF is trading at $1123.50 with a market cap of $76.32B and a 52-week range of $69.43 - $1698.50. In Q2 of 2022, Samsung’s revenue grew to $77.02T with 21.25% YoY increase and the net income increased to $10.95T which was an increase of 15.86% YoY. The EBITDA increased 12.67% to $23.16T. The price to earnings ratio (P/E) is 9.24. You can view SMSN’s 2022 Q2 earnings here and their 2021 Annual Report here.

INVRS is a social and collaborative investment research platform which I recently started using and absolutely LOVE. INVRS is increasing access to high-quality investment research and discussion. Its built around top notch data and tools for over 10k stocks and ETFs and the best part is its completely free to sign up! Sign up here and join my Green Candle Group!

Bullish Thesis

Here are three points to support the bullish thesis:

Diversification of Products: Samsung offers everything and anything that has to do with semiconductors and electronics. Although this business relies on tech, it almost seems recession proof. Everyone is always going to need a washer/dryer or appliances. Hospitals are always going to need medical equipment. Smartphones are a necessity in society these days. Samsung offers so many tech products that when the world economy is thriving, consumers will flock to their products and when the world economy is struggling consumers will go to their products because of the name brand.

Sales Jump: The market is always very interesting. Samsung’s second quarter results were bad but not bad as expected, therefore the stock price rose. Samsung was able to manage memory chip shipments, keep inventories, and stabilize prices. It appears Samsung is primed to maintain this price point for its products with the inventory of chips it now has.

HQ in South Korea: As much as this is a weird point to make, I believe in the current macro environment this is a major positive. Samsung’s biggest competitor in the chip space is Taiwan Semiconductors and with their operation being located in Taiwan and the pending China invasion, it may greatly benefit Samsung’s chip sales in the short term. If those new customers like the Samsung chips, it will be likely that those new customers stick with Samsung if TSMC business is halted or affected by this geopolitical conflict.

Bearish Thesis

Here are three points to support the bearish thesis:

Chip Operations Demand Slowing: Samsung currently has majority of its revenue coming from its chip manufacturing side of the business that also assists with all other products. Samsung has benefited greatly from the increased prices of chips due to the shortage but now it seems there is an oversupply in the market. Chip demand is slowing and the prices have begun to stabilize and in some cases decrease. If this is the case, Samsung will need to hope that other areas of the business increase in order to combat the decreased revenue from the chips part of the business, but I find this difficult to predict. With the world economy looking grim, I would find it hard to believe that tech would be a sector/industry that prospers.

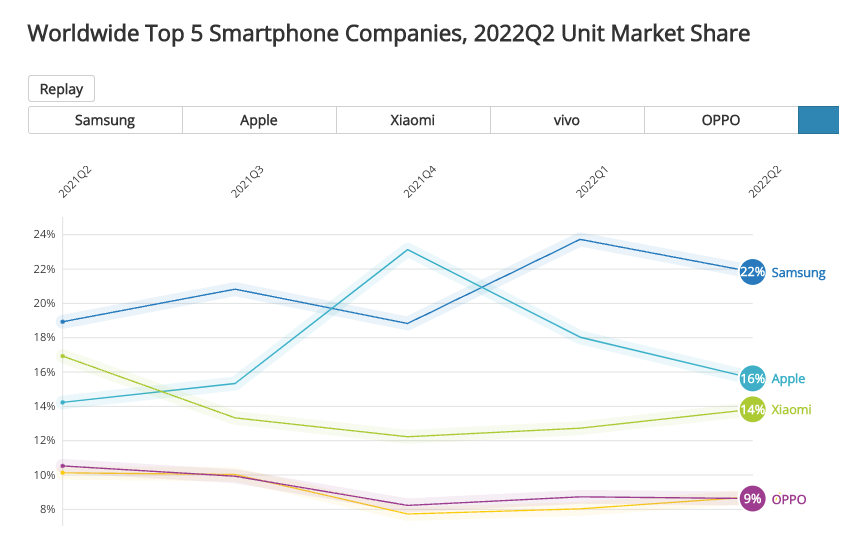

SmartPhone Demand Slowing: As shown in the chart below, Samsung has a good hold on the global smartphone market, but that hold is shrinking. More competitors are coming and big players are catching up. Samsung had some difficulties with smartphone batteries exploding and other issues with their phones and it appears over time their smartphones are becoming less desirable. Hopefully this is just a year corrections and current Samsung users just purchase new phones every other year, but this has to look like a chink in the armor of Samsung’s grasp on the market.

Foldable Phone Push: Recently, Samsung announced they are developing two new foldable phones. This trend and development of the product makes no sense to me at all. As the saying goes, “if it ain’t broke, don’t fix it”. I believe people enjoy the fact they do not have to open a phone in order to use it and they can simply pull their phone out of their pocket to use it. There was once a foldable phone craze with the RAZR and others, but those phones are now seemingly non-existent and I believe that is for a reason. Developing bendable glass and tech does not seem like a great use of resources if you ask me.

Learn more about Samsung here. Stay up to date on Green Candle by subscribing to our newsletter and following us on Twitter, Instagram, and YouTube!

Video edition: Macro Insights

If you’re new to stock investing, check out our introduction to stock investing series:

Have a great week everyone,

Brandon

Sign up for INVRS here and join my Green Candle Group!

Disclosure: The article was written by Brandon Keys, and it expresses the author's own opinions. I am not receiving compensation for it. I have no business relationships with any company whose stock is mentioned in this article. The information presented in this article is for informational purposes only and in no way should be construed as financial advice or recommendation to buy or sell any stock. Brandon is not a financial advisor. I encourage all readers to do further research and do your own due diligence before making any investments.