Saving for Retirement - Introduction

If you haven’t already, subscribe to our newsletter here to get our articles delivered directly to your inbox and follow us on Twitter, Instagram, and YouTube! In our Educational Series we will be taking a deep dive into different ways to invest your money in hopes that one or multiple of these methods strikes you as interesting and encourages you to invest your money to grow your wealth.

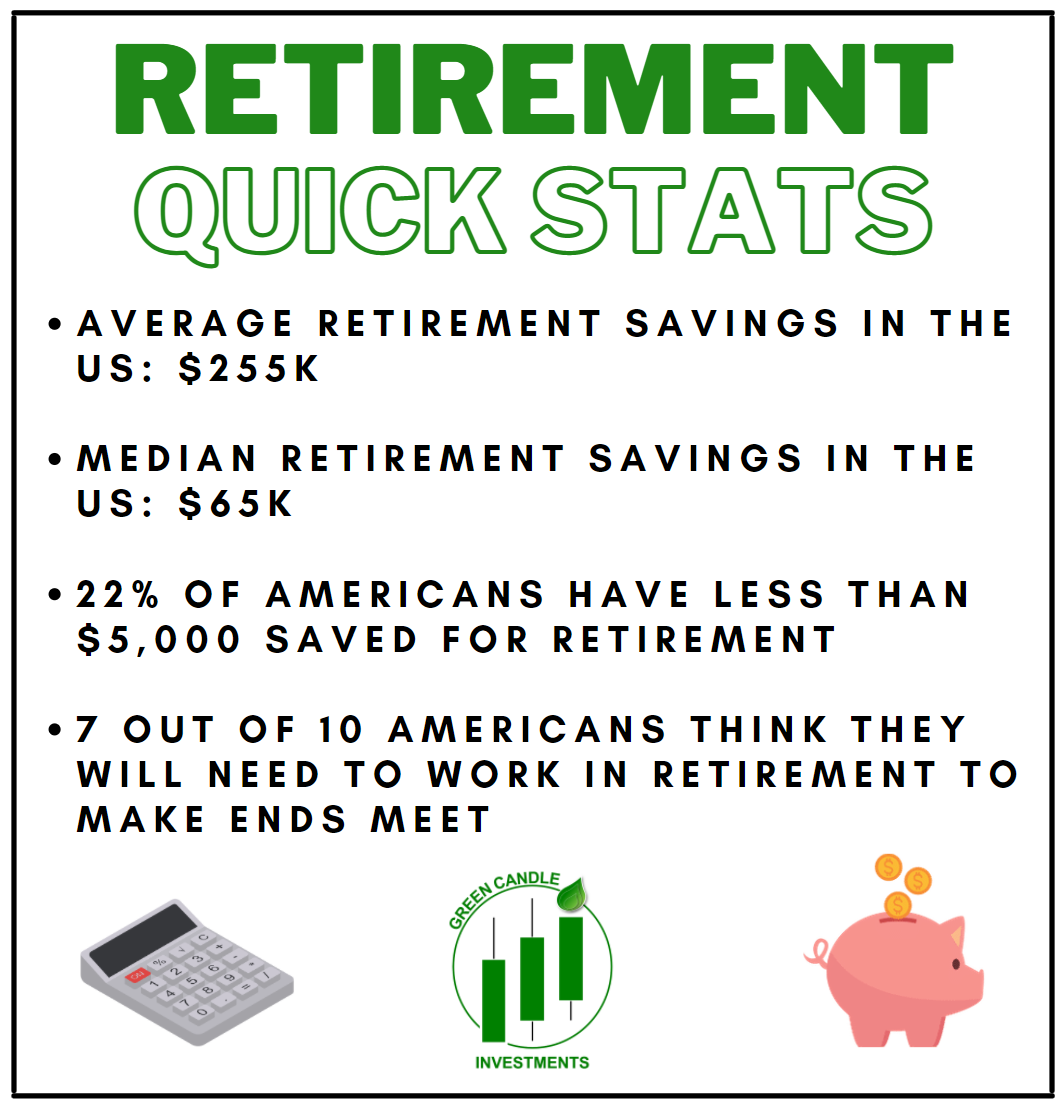

Why save for retirement?

When you’re young, it’s hard to think about retirement - it seems so far away. It’s even more difficult to think about saving for retirement. If you’re like me, you’ve got other financial items that need your attention NOW, including bills, student loan repayments, and saving for a down deposit on a house. If you’re in a similar situation, you might think to yourself (as I often do), “why put my money into a retirement account that I can’t touch until I’m 65?” or “I can always start saving for retirement next year.” So, why should you start saving for retirement now?

First, consider the alternative - having no money saved when you reach retirement age. How will you pay your bills and meet your living expenses without the income you relied on until retirement? You may think that Social Security will cover your expenses. However, according to the Social Security Administration, its payments replace only about 40% of the average wage earner’s income after retiring. Unless you’re willing to take a 60% cut in income following retirement, you’ll need more than Social Security to live comfortably (and this assumes that Social Security won’t run out before you retire). So, what will you do to earn money after retirement? Rely on your children or other family members? Pick up a part-time job? If these options are unappealing to you, then you need to start considering a retirement plan NOW.

Fortunately, in the U.S. there are many retirement options, each with slightly different advantages and disadvantages. However, the biggest advantage of starting early on any retirement plan is the power of compounding interest!

The power of compounding

What is compound interest? Compound interest is the interest on a loan or deposit calculated based on both the initial principal and the accumulated interest from previous periods. It is calculated by multiplying the initial principal amount by one plus the annual interest rate raised to the number of compound periods minus one. This differs from “simple” interest, in which interest is calculated based only on the principal amount.

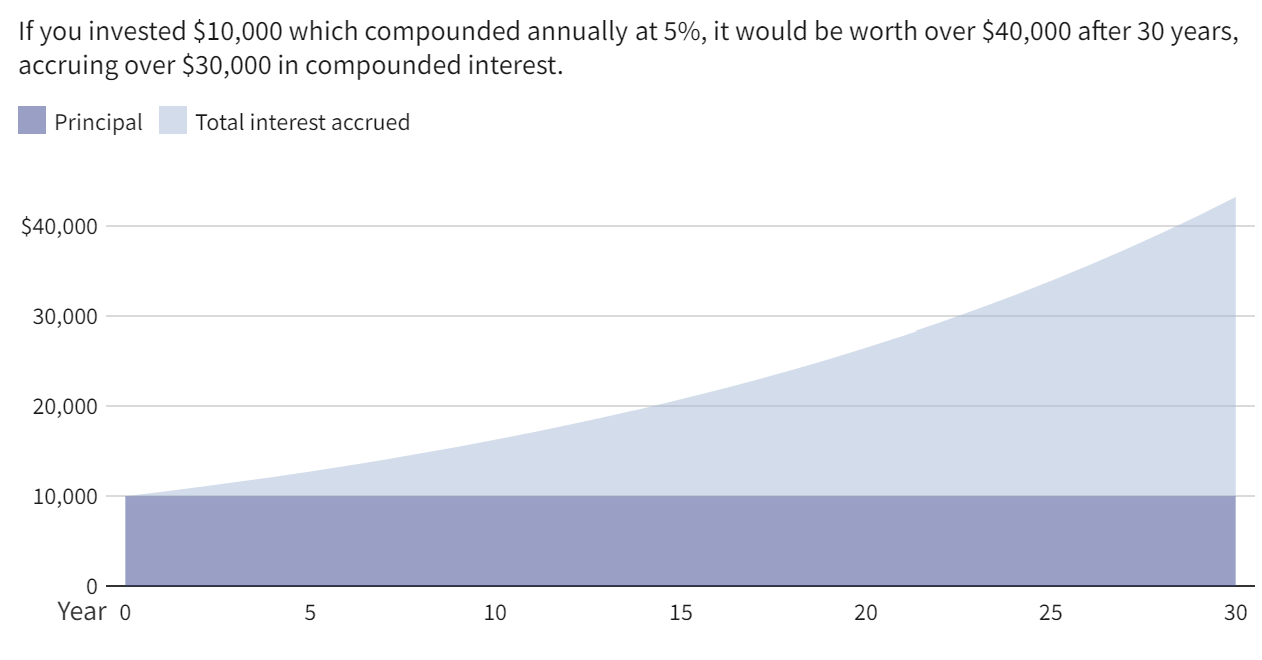

Because compound interest includes interest accumulated in previous periods, it grows at a nonlinear, ever-accelerating rate. This means that the earlier you start, the more your money will grow - but it will grow at ever accelerating rates the longer you let interest accrue. Below is a chart from Investopedia that highlights this nonlinear growth trajectory:

In the chart above, a $10k principal investment compounded by 5% annually would result in a gain of $30k over 30 years. If the same $10k principal amount were to gain 5% simple interest annually, you would receive $500 per year, resulting in a gain of $15k over 30 years. That’s the power of compounding.

Here’s another example: If you contribute $6k per year to a Roth IRA from the age of 30 to the age of 65, and the rate of return on your investment is 7% annually, your IRA will be worth nearly $900k by the time you're 65 years old. You can tweak these numbers using NerdWallet’s calculator, here.

Remember, with compounding interest, the earlier you start investing, the more time there will be to let the power of compounding work its magic. In the Roth IRA example above, extend your contributions to age 70 and you jump from $900k to nearly $1.3M! Over just 5 extra years the account increases in value by 44%.

Common retirement plans

Now that we’ve convinced you of the importance of starting early, let’s take a look at a few common retirement investing options. Over the next several weeks, we will write more in-depth articles on each of these investing vehicles, but for now, here are brief definitions of a few:

401 (k): A 401 (k) is considered a contribution account that is offered to employees by an employer; the employer will commonly offer a contribution “match,” which helps encourage employees to contribute to the retirement fund. For example, your employer might contribute up to 3% of your salary—as long as you put in at least that amount yourself.

Roth IRA: A Roth IRA is an account that allows you to set aside “after-tax” income up to a specified amount each year (as of this writing, the absolute maximum annual contribution is $6,000). Both earnings on the account and withdrawals after age 59½ are then tax-free, as your initial contributions came from income that had already been taxed.

Traditional IRA: A traditional IRA is a tax-advantaged plan that allows you significant tax breaks while you save for retirement. Anyone who earns money by working can contribute to the plan with “pre-tax dollars,” meaning any contributions are not considered taxable income. Whereas Roth withdrawals are tax-free, withdrawals from a traditional account are taxed.

SEP IRA: The SEP IRA is set up like a traditional IRA, but for small business owners and their employees. Only the employer can contribute to this plan, and contributions go into a SEP IRA for each employee rather than a trust fund. Self-employed individuals can also set up a SEP IRA.

It’s never too early to start saving for retirement

If you take one thing from this introduction article, let it be this: it’s never too early to start saving for retirement - it may seem like a lifetime away, but time will go fast and your future self will be glad you started saving early! Over the next several weeks, we’re going to break down a few common retirement investing vehicles. As always, we hope that you will find this series useful and please don’t hesitate to reach out with comments or questions about the content!

If you liked this article, please subscribe to our newsletter and be sure to follow us on Twitter, Instagram and YouTube!

Finish out the week strong!

Brandon and Dan

Do you want to HODL BTC in a tax-advantaged retirement account? Check out Choice by Kingdom Trust! Click this LINK to find out more!

Disclosure: The article was written by Daniel Kuhman and Brandon Keys, and it expresses the author's own opinions. The information presented in this article is for informational purposes only and in no way should be construed as financial advice or recommendation to buy or sell any stock, asset, or cryptocurrency. Brandon and Daniel are not financial advisors. We encourage all readers to do further research and do your own due diligence before making any investments.