Starbucks Corporation (Ticker: SBUX) - Brief Breakdown

In our Brief Breakdowns, we pick a stock and take opposite sides – one of us presents the bullish argument and the other presents the bearish argument.

If you haven’t already, subscribe to our newsletter here to get our articles directly to your inbox and follow us on Twitter and Instagram! Also join us for our Twitter spaces, every Monday we discuss our stock breakdown at 8 PM EST, & Friday we have a Bitcoin Happy Hour at 4:30 PM EST!

Company Description

Starbucks Corporation is a multinational chain of coffeehouses, roasters, marketers, and retailers of specialty coffee worldwide. Its stores offer coffee, tea beverages, whole bean and ground coffee, single-serve coffee products, iced coffee products, breakfast sandwiches, pastries, and lunch items. Starbucks is the world’s largest coffee chain with 33,833 stores in 80 countries and 15,444 in the United States. Out of the US based stores, 8,900 are company-operated, while the remainder are licensed. Starbucks offers products under the Starbucks, Teavana, Seattle’s Best Coffee, Evolution Fresh, Ethos, Starbucks Reserve, and Princi brand names.

Quantitative Analysis

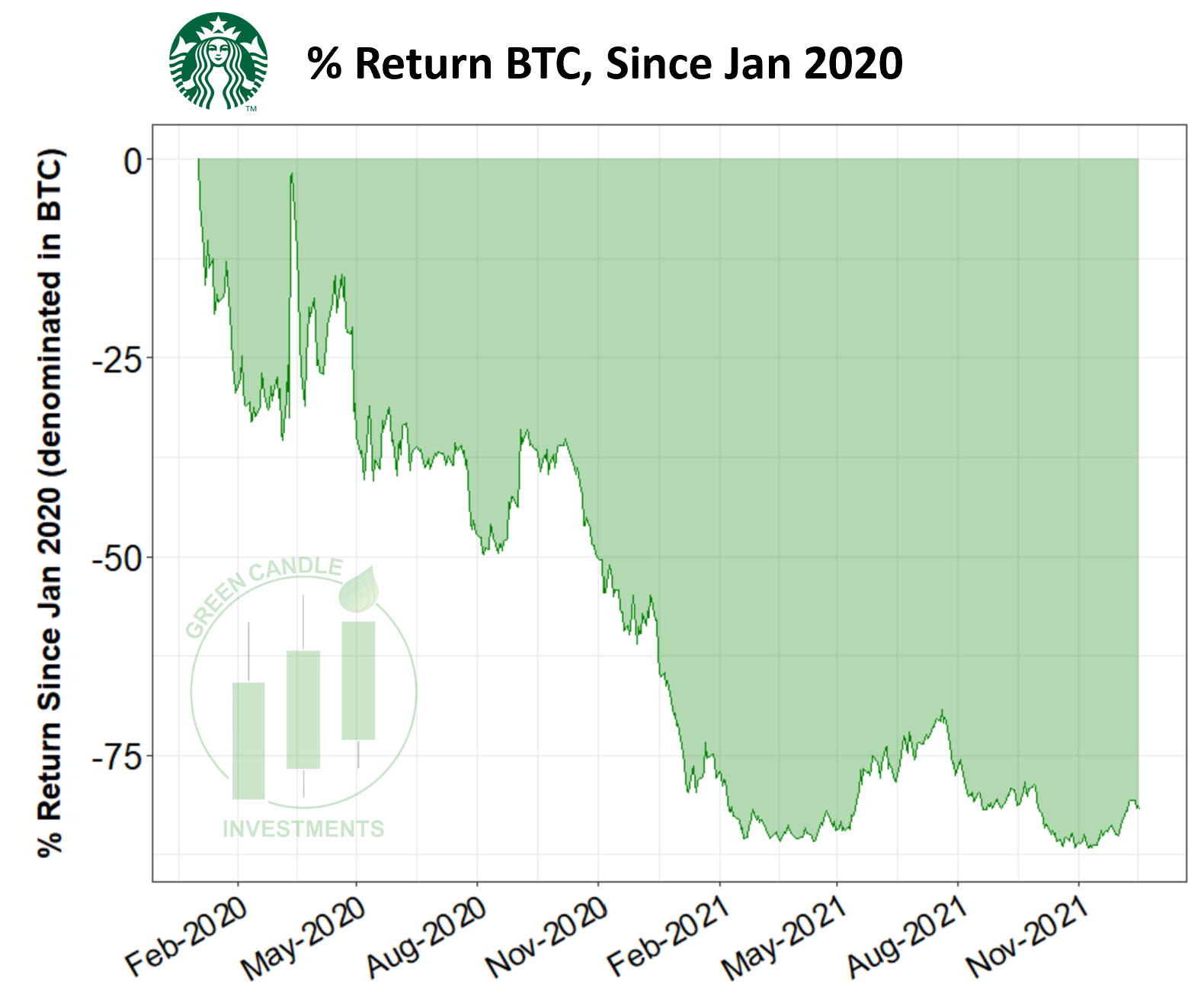

At the time of this writing (12/19/2021), SBUX is trading at $108.63 with a 52 week range of $95.92 - $126.32 and a market cap of $127.44B. In Q4 of 2021, SBUX’s consolidated net revenue was up 31% to a record $8.1 billion, comparable store sales were up 17% globally and up 22% in the U. S.. Starbucks has also committed $20 billion of share repurchases and dividends over the next three years. Return of equity (ROE: Net Income / Total Equity *100) of SBUX is -60.67% and net margin (net income / revenue) is 14.45%. The debt to equities ratio (total liabilities / total equity) is -6.9. This financial analysis was done using financialstockdata.com (become a beta tester here). You can view SBUX’s last quarterly earnings here and 2020 annual report here. Below we have percent returns denominated in both USD and in Bitcoin.

Qualitative Analysis

Starbucks is the world’s largest coffee brand and has the largest retail footprint of any coffee retailer globally. People and financial influencers like Dave Ramsey have brought up Starbucks high priced coffee as a slight and not a financially smart decision, but that does not seem to affect the sales. In the new work from home environment, coffee shops are becoming more popular because of the free WiFi and the ability to get out of their home office to work. Starbucks is one of the most well known coffee brands and their massive global footprint gives them staying power.

Bullish Thesis

Here are three points to support the bullish thesis:

Large Physical Footprint: As noted above, Starbucks is the world’s largest coffee chain, operating 15,444 in the United States and nearly 34,000 stores worldwide. These include not only standalone stores, but also those located in other outlets (e.g., Target, Kroger, etc.). By 2030, they plan to expand to 55,000 stores worldwide, primarily through growth in China. That’s right - while it took ~20 years to open 34,000 stores, they plan to open another 21,000 in the next 9 years. This level of growth (if they achieve it) should have any investor excited.

More Than Just Coffee: Starbucks has done a great job making money from their customers over time. One way in which they’ve accomplished this is product expansion. In 1971, when the first Starbucks opened in Seattle, they didn’t even sell individual beverages. It wasn’t until 1982 that Starbucks implemented a coffee bar. Today, Starbucks has over 40 drinks on their menu, a number of food and pastry items, and other knick knacks (e.g., mugs, thermostats) for sale. What used to be a trip to the shop for a $2 coffee has quickly turned into a $15 stop for coffee, a breakfast sandwich, and a cake pop.

New Deal with Amazon: In November, Starbucks announced that they were partnering with retail giant Amazon to open their first ever cashier-less location in New York City. Throughout the pandemic, many companies realized the need for contactless service - for retailers, this meant developing platforms for remote digital transactions and contactless pick-up or delivery. While most states in the U.S. have completely re-opened their economies, countries around the world are going back into lockdown. These contactless locations would likely be exempt from closures and would allow Starbucks to continue operating. Even when everyone comes to their senses and re-opens, some customers will have grown accustomed to contactless services. While I personally prefer to walk into a coffee shop and order from a cashier, many customers may opt for contactless services - Starbucks will be able to provide both.

Bearish Thesis

Here are three points to support the bearish thesis:

Perception of Expensive Coffee: Many “financial gurus” tell their followers that the $5 cup of coffee that Starbucks offers is too expensive and in order to cut spending you should cut out the Starbucks coffee on a daily/weekly basis. This negative light these gurus shed can get anyone that initially consumes their content will more than likely stop shopping in the short term at Starbucks. Although I do not subscribe to that theory, Dave Ramsey is one of the most widely followed financial influencers and his influence cannot be understated.

Looming Lockdowns: Although companies like Starbucks may be better suited for lockdowns than others, it is something that should not be taken lightly. In the short term in March 2020, stocks plummeted and even the companies that were better suited for the pandemic. Some areas are going back into lockdowns even with vaccine mandates and this potential widespread lockdowns will hurt Starbucks in the short term. It will be interesting to see how this all plays out and how it affects businesses in this potential second shut down.

Potential Decrease in Consumer Spending: This goes hand in hand with the looming lockdowns. March 2020 caused everyone to sell off equities and save cash. This could lead to decreased spending and as Starbucks coffee is expensive and not essential, consumers can find cheaper versions of their products and stop going to Starbucks and its subsidiaries all together. This decrease and the increase in fixed costs could mean difficult times are head for Starbucks and most consumer products.

Learn more about SBUX here. Stay up to date on Green Candle by subscribing to our newsletter and following us on Twitter and Instagram! And don’t forget to join us in our Twitter Spaces tonight at 8 PM EST!

If you’re new to stock investing, check out our introduction to stock investing series:

Have a great week everyone,

Brandon & Daniel

Disclosure: The article was written by Daniel Kuhman and Brandon Keys, and it expresses the author's own opinions. They are not receiving compensation for it. They have no business relationships with any company whose stock is mentioned in this article. The information presented in this article is for informational purposes only and in no way should be construed as financial advice or recommendation to buy or sell any stock. Brandon and Daniel are not financial advisors. We encourage all readers to do further research and do your own due diligence before making any investments.