The Astrolabe - Let the Yield Curve Control Games Begin

Guest Article Written by Nadir Khan

If you haven’t already, subscribe to our newsletter here to get our articles directly to your inbox and follow us on Twitter and Instagram! Also join us for our Twitter spaces, every Tuesday we discuss our stock breakdown at 8 PM EST, & Friday we have a Bitcoin Happy Hour at 4:30 PM EST!

Dear readers,

The Federal Reserve of the United States has a dirty little secret: Yield Curve Control has begun and they don’t want anyone to find out.

What is a Yield Curve?

The yield curve is a graphical representation of the interest rates paid on bonds of different maturities, typically government bonds, plotted against their respective maturities. The yield curve shows the relationship between the yield or interest rate of a bond and the time to maturity.

Normally, the yield curve slopes upward, meaning that longer-term bonds have higher yields than shorter-term bonds. This reflects the expectation that over time, inflation and interest rates may increase, and investors demand a higher return to compensate for this increased risk.

The winding unpredictable road of central bank policy leads dangerous places..

However, sometimes the yield curve can invert, meaning that short-term bonds have higher yields than long-term bonds. This inversion of the yield curve has often been a precursor to economic recessions, as it suggests that investors expect interest rates to fall in the future due to a weakening economy. We currently find ourselves in a deeply inverted environment.

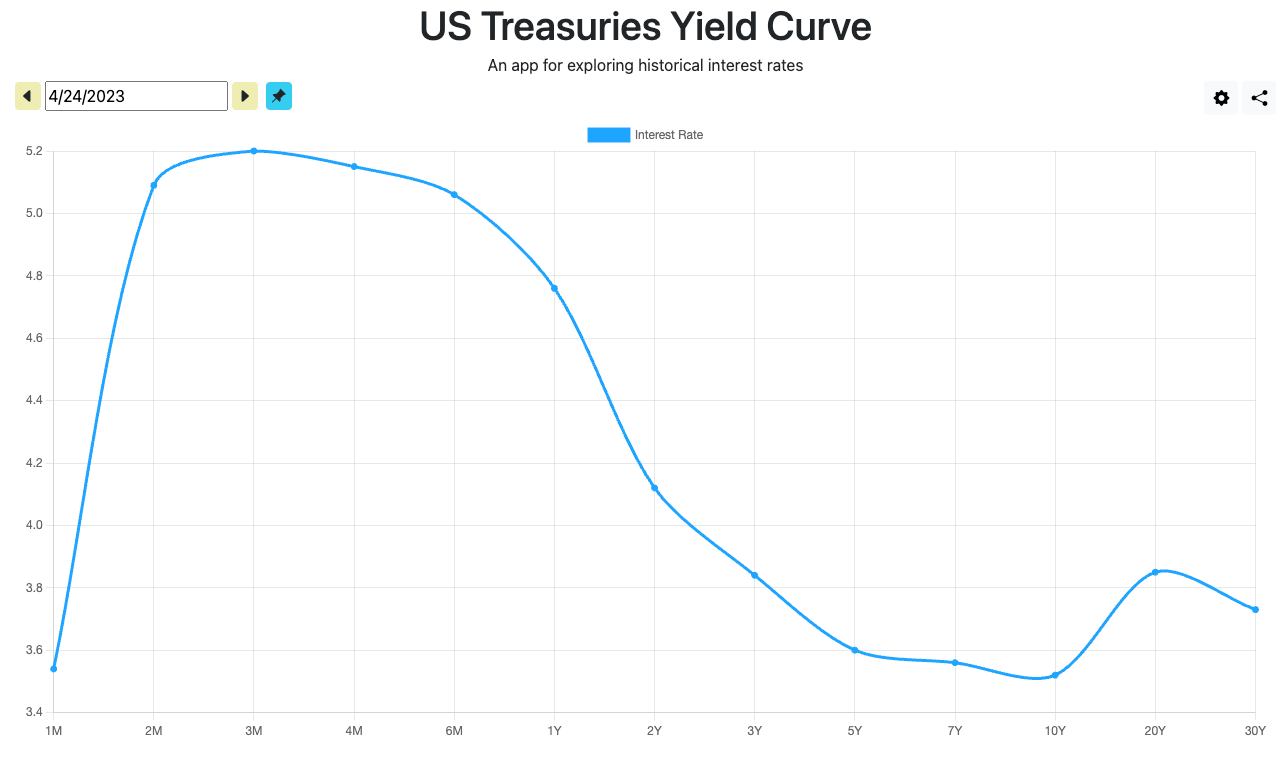

This is an inverted yield curve. The short end returning much higher than the long end. The bond market expects trouble ahead.. Source: ustreasuryyieldcurve.com

Investors, market participants and policymarkers (in theory) closely watch the shape of the yield curve for insight into the market's expectations for economic growth, inflation, and monetary policy.

A central thesis of The Astrolabe is that we live in a credit-backed system, whereby the creation of debt has been the primary engine fuelling economic “growth” for the last 40 years. In this sense, the debt markets are far more indicative of the health and direction of global markets and the economy than any other market. Credit markets remain the deepest, most liquid and most influential pillar of this fragile system. In this way, the yield curve and credit market provides a more honest assessment than central bankers and policymakers. That is, if it is allowed to price itself freely..

What is Yield Curve Control?

Yield curve control (YCC) is when a central bank intervenes in the bond market. The central bank basically walks into the room and says “I don’t like what I see here, let me rearrange things.” Functionally, this means the central bank will use its money printer to create reserves (M2 or narrow money) to purchase government bonds in order set a particular yield.

For example, if people lose confidence in the 10 year bond, and believe (rightly) that it will result in a loss over time when for inflation, then they will sell the 10y bond and the yield will rise (as bond prices drop, the government has to offer a more attractive return for people to hold its paper IOU).

The problem with rising yields is that it pressures the government balance of payments. If they are already running a deficit (spending more than they earn, which they are), paying higher interest rates on rising bond yields makes them get deeper underwater. This is where the financial engineering of YCC comes into play.

The Central Bank comes in and starts buying the affected bonds from the government. This artificial demand for the “long-end” of the bond curve suppresses yields and alleviates pressure on state coffers. For example, if the target level is 2%, and the yield on the 10-year bond rises above that level, the central bank may purchase bonds in the market to push the yield back down.

Why is YCC undesirable? Breaking Price Signals

This policy is not without consequences. YCC distorts market signals and creates major challenges for unwinding the policy once it is in place. Moreover, it directly contributes to inflation over the medium and longer term. It is just a way of kicking the can down the road and continually inflating an excessive debt balloon. The only way it can ever be paid back is to let the currency inflate.

As a sovereign, you have to choose between saving your currency or saving your debt. The currency is historically always chosen as the release valve as a sovereign country can always avoid a “hard” default on its debt through bond market manipulation.

What was BTFP?

The Bank Term Funding Program (“BTFP”) is a band-aid solution created in March 2023 to temporarily avoid bank runs. The program was created by the Federal Reserve to provide emergency liquidity to U.S. depository institutions who were holding long term bonds that cratered in value. As the Fed aggressively raised rates in 2022, banks who held long term bonds as safe reserve assets began to see major losses pile up. These losses are referred to as “unrealized” as they hadn’t been sold them yet and marked as a loss on their books. Seeing these losses, depositors ran for the door and tried to get there funds out asap.

Long term bonds only pay out if they are held to maturity (10y, 20y, 30y), and with depositors running out the door and all their deposits tied up in long term treasuries, panic spread and there was no choice for the Fed but to come in and provide a “rescue”. Then the largest bank collapse since 2008 happened in March 2023. two banks failed (Signature Bank and Silicon Valley Bank). The program was hastily thrown together over a weekend.

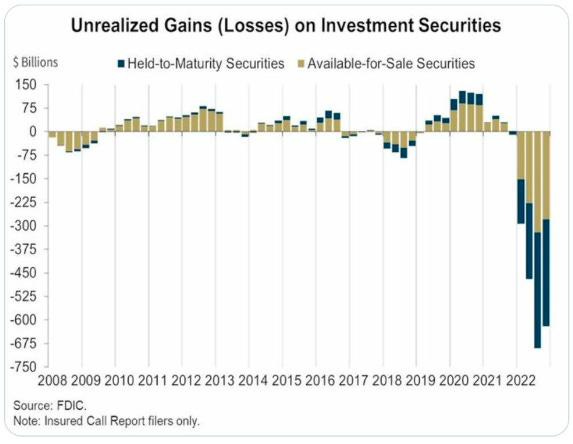

US Banks are sitting on enormous losses in what they thought was the safest “asset” out there: long duration US Treasury Bonds. Source: FDIC

The BTFP offers loans of up to one year in length to eligible depository institutions that pledge collateral such as U.S. Treasuries, mortgage-backed securities, and other qualifying assets. Here is the kicker: the loan is offered at “par-value”, meaning if your bond was worth $0.60 on the $1, the central bank loans you the full $1.

How is BTFP = YCC?

Offering par-value loans for underwater bonds that banks are holding is a backdoor form of Yield Curve Control. The Fed has essentially stepped in as a last resort buyer of long term treasury bonds and thus has re-priced them, bringing the yields back down. Seeing the degree of unrealized losses on bank balance sheets, the Fed added liquidity back into the system. And although the Fed says the “BTFP was created to support American businesses and households”, how come the math doesn’t add up? If a bank holds a bond worth $0.60 on the dollar of what is was once worth, how can is magically receive $1 back as though none of the losses had occurred?

The cost of this policy will be released through the currency in the form of continued debasement and inflation. Inflation was not a transitory supply-chain phenomenon nor was it a product of the Russian invasion. The deeper structural inflation that we will experience in the coming years is a product, in part, of excessive monetary expansion and manipulation into credit markets.

Yield Curve Control is an inherently inflationary and distortionary policy. As the hour grows late for a system absolutely bursting with debt that will never be paid back, policy makers continue to double down on the very actions that got us in this mess in the first place, accelerating towards an ever nearing cliff.

If you enjoyed this piece please subscribe to The Astrolabe for more insights, analysis and translations of complex monetary, macro and investing concepts.

Macro Insights Pod:

Thanks for reading,

Nadir

If you’re new to stock investing, check out our introduction to stock investing series:

Disclosure: The article was written by Brandon Keys or a guest writer, and it expresses the author's own opinions. I am not receiving compensation for it. I have no business relationships with any company whose stock is mentioned in this article. The information presented in this article is for informational purposes only and in no way should be construed as financial advice or recommendation to buy or sell any stock. Brandon is not a financial advisor. I encourage all readers to do further research and do your own due diligence before making any investments.