The New Age Investing Portfolio

Education Series

If you haven’t already, subscribe to our newsletter here to get our articles directly to your inbox and follow us on Twitter, Instagram, and YouTube! In our Educational Series we will be taking a deep dive into different ways to invest your money in hopes that one or multiple of these methods strikes you as interesting and encourages you to invest your money to grow your wealth.

First, what is an investing portfolio?

An investing portfolio is a combination of all of your investments. This can include anything from real estate, stocks, bonds, ETFs, Bitcoin, various cryptocurrencies, wine, trading cards, and much more! We previously published a series of articles describing how to invest in stocks and real estate (you can check them out here: stocks & real estate). There are many theories on how to “balance” a portfolio - that is, how to distribute the money in your portfolio across different asset classes. Investors often analyze their holdings by quantifying percentages of each asset class in their portfolio. In this article, we describe the classic “60/40”

portfolio and then both founders of Green Candle break down their own portfolios. As a reminder, neither Brandon or Dan are financial advisors. Below, we break down our own portfolios to show you how two incredibly like minded individuals still use different investing strategies.

The 60/40 Portfolio

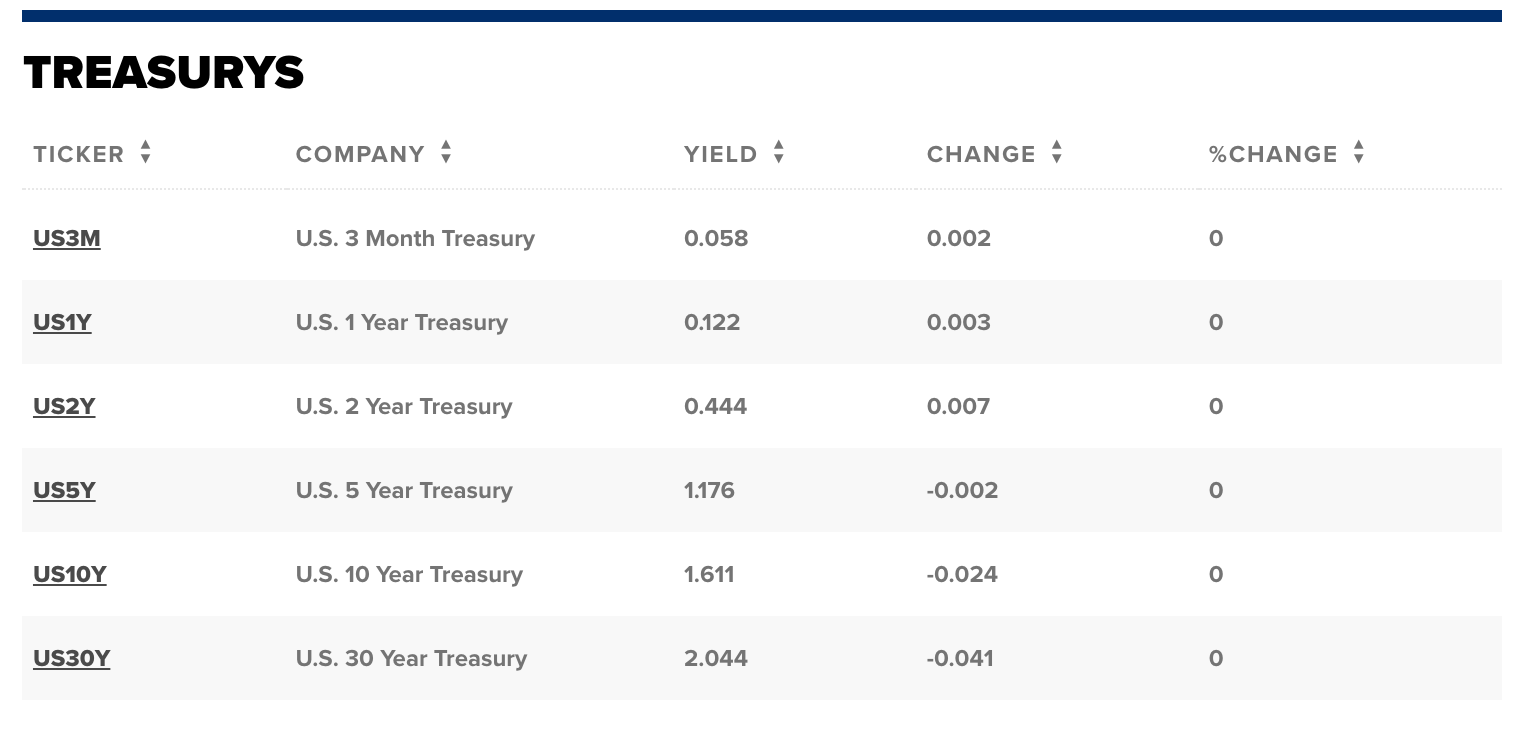

The classic “60/40” is a portfolio containing 60% stocks and 40% bonds. The 60% stocks can be individual stocks, ETFs, mutual funds, or a combination of all of these. The other 40% is made up of bonds, which are fixed income instruments that essentially act as I.O.U.s between a lender and a borrower. According to CNBC, the current highest bond return is slightly over 2% for the 30 year treasury, you can see all of the values in the table below.

With inflation reportedly over 5% for 2021 alone, a 2% yield on bonds will not even keep your purchasing power steady. With assets inflating well over 5%, it does not seem responsible to intentionally lose purchasing power with 40% of your portfolio.

1st Portfolio

These percentages have changed over time and have changed drastically over the past year due to massive inflation of real estate pricing and Bitcoin price taking off from around $8k to ~$63k at the time of this writing. My current rental property also rose in price around 30% and with most of that money coming from a loan, 30% of value with borrowed money gives massive returns. This in turn has made my stock and ETF holdings become miniscule. My largest stock holdings are NLST and PENN, which have both done well for me since buying these stocks, with NLST doing tremendous up around 700%. So although my stock holdings are small relative to my BTC and Real Estate, they have still performed very well relative to bonds. My largest ETF holdings are VOO, ARKF, & ARKK. My ETFs haven’t done quite as well as my stock picks, but throughout the long term I anticipate these will have less volatility and continue to improve over time. I’m excited about the future of my portfolio and will continue to update on my progress!

2nd Portfolio

For this exercise, I thought it would be useful to present my general investing and retirement portfolios separately to demonstrate how my time preference influences my investing decisions.

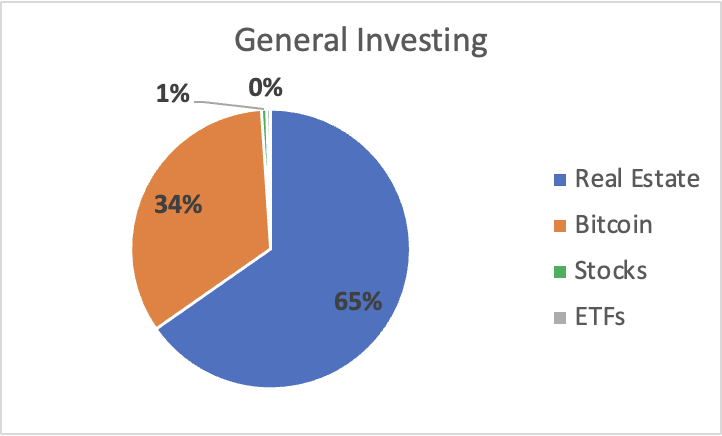

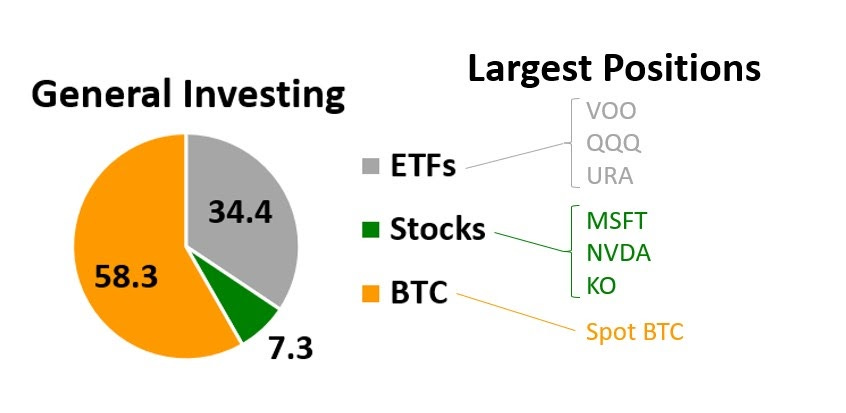

My general portfolio can be broken into three asset classes: ETFs (34.4%), individual company stocks (7.3%), and bitcoin (58.3%). At the moment, my general investing portfolio is largely being used as a means of saving for a down payment on my first piece of real estate, which I’d like to be able to do in the next 12-15 months. Because of this, a large chunk of this portfolio is dedicated to assets that I believe will grow quickly over the next year. I am extremely bullish on BTC and believe that it will continue to rise in value - the real question will be whether or not I’m willing to sell any of my sats when the time comes for me to buy a house. The next largest chunk of this portfolio includes ETFs - primarily VOO (S&P 500 index fund), QQQ (Nasdaq 100 index fund), and URA (an index fund for uranium). This chunk is largely here to provide some stability to the portfolio, but I don’t mind that these index funds continue to hit new ATHs week after week. Finally, the last ~7% of my general investing portfolio contains individual stocks. Of my individual stocks, my largest allocation accounts for only 1.1% of my entire portfolio and the majority of them account for less than 1%. I’m using this chunk of the portfolio to learn more about individual stock/company assessment, so I typically start a new stock at a very low allocation and gradually add or subtract from it based on company performance/reporting.

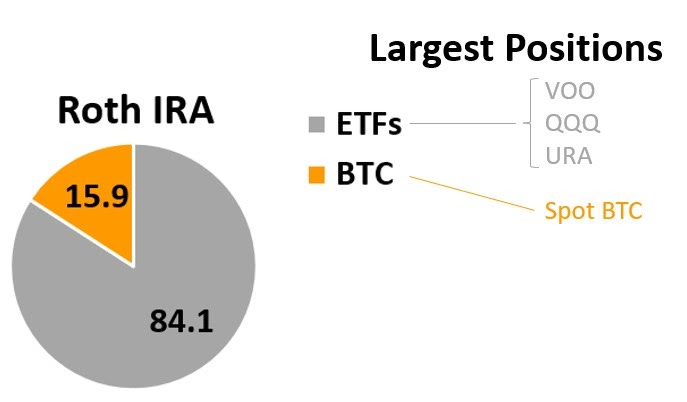

Whereas individual stocks and BTC account for large percentages of my general portfolio, my retirement portfolio is nearly 85% market index ETFs. This is a Roth IRA, so I will not be able to draw any money from this account for at least 30 years. Because I have a much longer time horizon on my retirement portfolio, I’m willing to invest largely in relatively safe ETFs that have a solid history of moderate returns. Given enough time, the power of compounding can turn moderate returns into huge sums of money. I have ~16% of this account allocated to bitcoin. In 30 years, I believe BTC will be the reserve currency of most countries in the world.

If you’re new to stock investing, check out our introduction to stock investing series:

If you’re new to real estate investing, check out our real estate investing series:

Real Estate Wrap Up

Have a great rest of your week!

Brandon & Dan

If you liked this article, please subscribe to our newsletter and be sure to follow us on Twitter, Instagram and YouTube!

Disclosure: The article was written by Daniel Kuhman and Brandon Keys, and it expresses the author's own opinions. The information presented in this article is for informational purposes only and in no way should be construed as financial advice or recommendation to buy or sell any stock, asset, or cryptocurrency. Brandon and Daniel are not financial advisors. We encourage all readers to do further research and do your own due diligence before making any investments.