Uber Technologies Inc. (Ticker: UBER) - Brief Breakdown

In our Brief Breakdowns, we pick a stock and take opposite sides – one of us presents the bullish argument and the other presents the bearish argument.

Brief Breakdown: Uber Technologies Inc. (NASDAQ: UBER)

In our Brief Breakdowns, we pick a stock and take opposite sides – one of us presents the bullish argument and the other presents the bearish argument. If you haven’t already, subscribe to our newsletter here to get our articles directly to your inbox and follow us onTwitter and Instagram!

Company Description

Uber Technologies Inc. (NASDAQ Ticker: UBER) is an American technology company whose services include ride-hailing, food delivery, package delivery, couriers, freight transportation, and electric bicycle and motorized scooter rental (through a partnership with Lime). Uber was founded in 2009 and was an immediate disrupter to the taxicab industry, allowing anyone to use their own personal vehicle to transport patrons to locations. Uber is estimated to have over 93 million monthly active users worldwide and has operations in 900 metropolitan areas worldwide. The company started with early success and in 2013 was named tech company of the year by USA Today. As Uber grew, it added more services - in 2014 they launched UberPOOL, a shared transport service, and Uber Eats, a food delivery service. Uber has had multiple investments combining operations in Europe and Asia with Yandex Taxi and Grab. In 2019 Uber became a public company via an initial public offering. Following the IPO, Uber’s shares dropped 11%, resulting in the biggest IPO first-day dollar loss in US history. Recently Uber has been criticized for the treatment of drivers as independent contractors, disruption of the taxicab businesses, and a cause of increased traffic congestion.

Quantitative Analysis

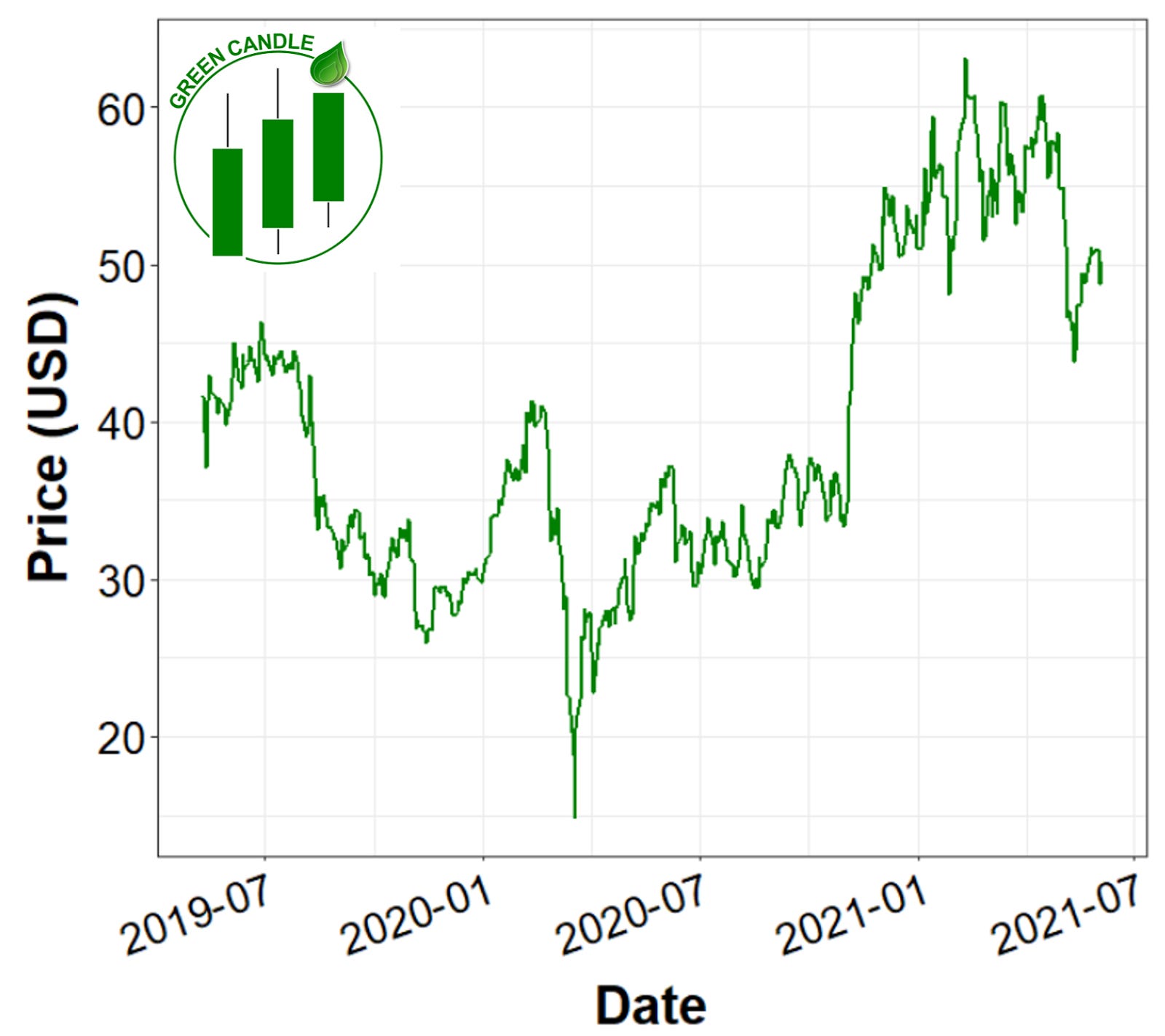

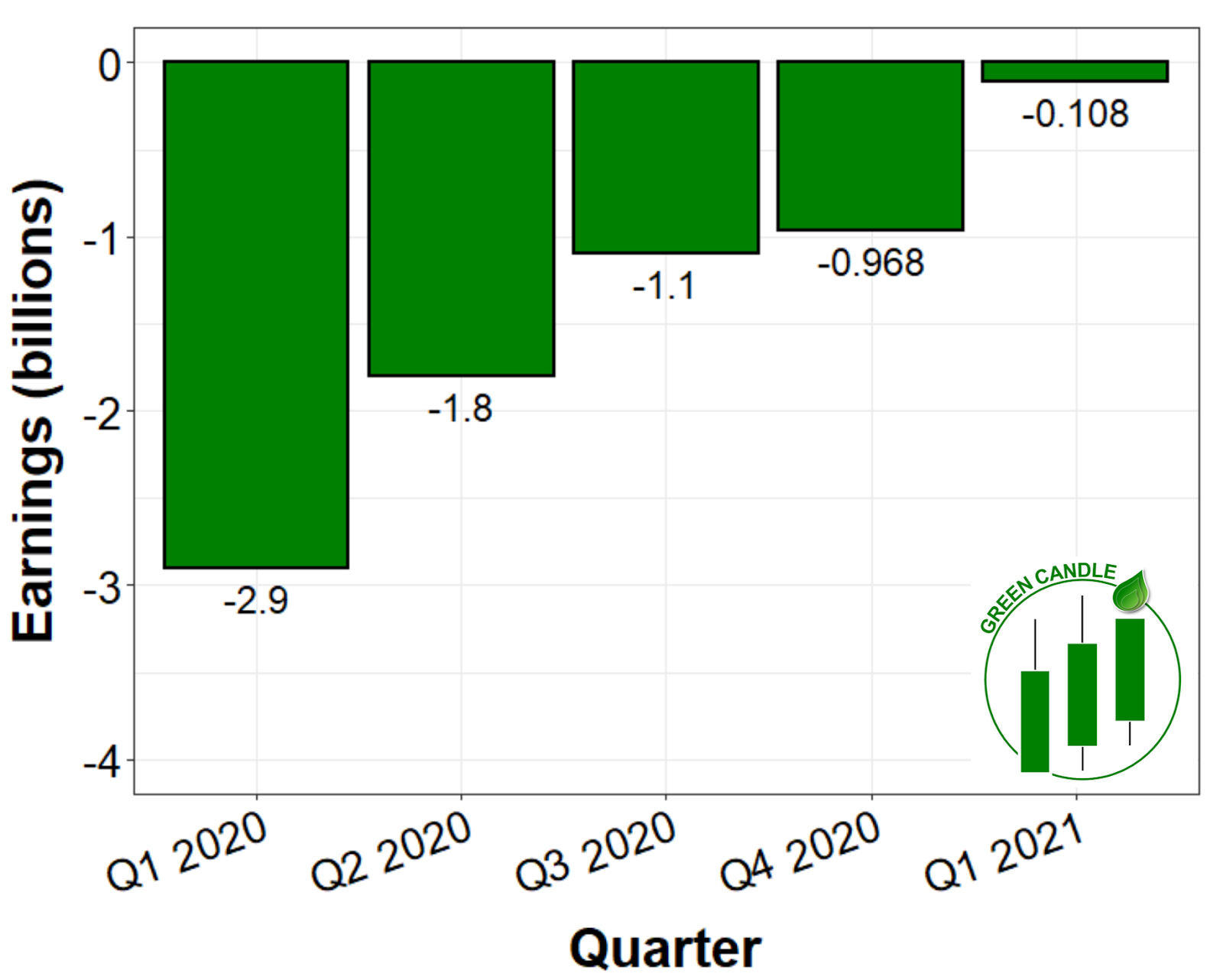

At the time of this writing (6/6/2021), Uber is trading at $50.18 with a 52 week range of $28.39 - $64.05 and a market cap of $93.93B. In Q1 of 2021, Uber gross bookings reached an all-time high of $19.5B, up 24% year over-year, but reported a net loss of $108 million. Revenue of $2.9 billion and mobility revenue of $853 million were reduced by a $600 million accrual made for the resolution of historical claims in the UK relating to the classification of drivers in Q1 2021. During the COVID-19 pandemic, more and more users went to the mobile app platform to get food delivery service. This is shown in the 166% increase in delivery gross bookings, which equates to $12.5 billion. Although Uber is up 33.2% over the last 12 months, it’s stock has fallen by 9.91% in the last 3 months. This downward velocity is likely - at least in part - due to store/restaurant re-openings and a decreased demand for food delivery services. Despite the growth in the delivery and gig economy, Uber has yet to report positive earnings in a quarter since becoming publicly traded. Like many “tech” companies, Uber’s lack of positive earnings has not hindered stock prices. You can view Uber’s 2021 Q1 earnings here and Uber’s 2020 annual report here.

Qualitative Analysis

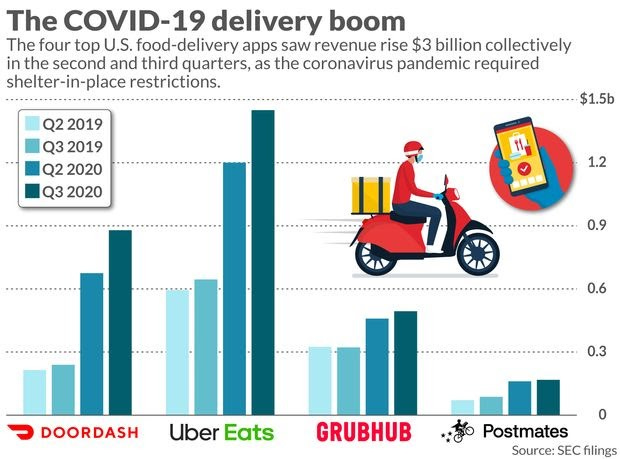

Uber has drawn criticism from some on their treatment of drivers as independent contractors rather than employees. This designation affects taxation, work hours, and overtime benefits. Despite the criticism, Uber controls 68% of the rideshare market share and 22% of the food delivery market. With each quarter throughout the COVID-19 pandemic, the food delivery industry grew. According to MarketWatch, the top four US food delivery apps saw revenue rise by $3 billion collectively in the second and third quarters of 2020. As COVID-related restrictions loosen, it is unclear whether delivery services such as Uber will continue to see the kind of growth it saw during the pandemic. If Uber’s food delivery sector decreases, there is hope that Uber’s ride share revenue will rise back to pre-COVID levels. If food delivery services maintain their growth and rideshare demand returns to pre-COVID levels, Uber is in for one hell of a year!

Here are three points to support the bullish thesis:

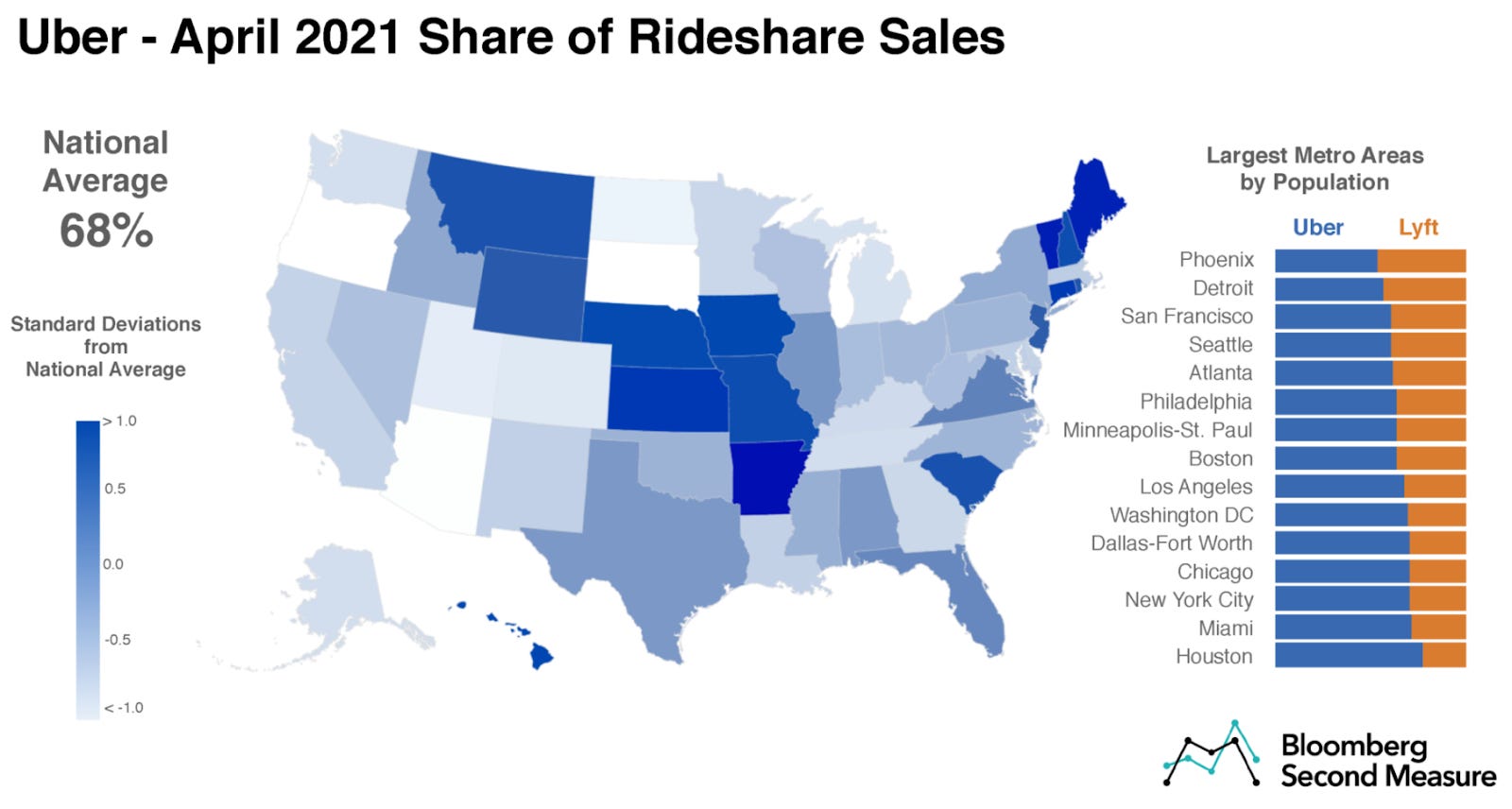

Market share: By far one of Uber’s biggest advantages is its existing dominance over market share. In the rideshare sector, Uber controls an estimated 68% of the market, with its only serious competition coming from Lyft. This control is partially due to the relatively small amount of mainstream competition in the industry - in fact, we were hard pressed to come up with rideshare companies not named Uber or Lyft (although, Google helped us out and told us about Via). However, control over the rideshare market does not appear to be a fluke for Uber. As noted in the chart above, they also control a substantial share of the food delivery sector, with their only real competition coming from DoorDash and GrubHub. If Uber continues to exercise this level of control across multiple markets, expect their stock value to continue rising.

Brand recognition: Uber dominates the rideshare market in large part due to its familiarity with consumers in a sector with relatively few mainstream brands. Despite negative news coverage in 2017, Uber enjoys a solid reputation. They have received overwhelmingly positive customer reviews. Indeed, at the time of this writing Uber has a 4.6 star rating in the Apple App Store and a 4.4 star rating on the Google Play store. Lyft, Uber’s primary competitor in the rideshare sector, has a 4.9 star rating on the Apple App Store but only a 3.6 star rating on the Google Play Store. Uber’s ability to maintain positive customer relations in the face of negative press is a competitive advantage that shouldn’t be underestimated. Although Uber enjoys solid brand recognition with consumers, it should be noted that drivers may feel slightly different. One driver survey found that drivers had more favorable experiences working with Lyft.

Product diversification and adaptability: Uber began as a ridesharing company, but has quickly adapted their product to meet other demands. After disrupting the taxicab industry, they quickly incorporated carpooling and food and package delivery services. They also recently entered into a deal with Lime, an electric scooter service. As part of the deal, Lime acquired Jump, Uber’s electric bike and scooter business. This deal not only increased Uber’s exposure to the growing “microcommuter” market, but also allowed them to shed Jump’s cash losses. Their ability to adapt their products and services bodes well for their future. Automation is likely to take place in many of the sectors in which Uber operates - particularly ridesharing and food delivery - as autonomous (self-driving) vehicles become more reliable and accessible. As this transition happens, Uber's ability to adapt will help it maintain its competitive edge.

Bearish Thesis

Here are three points to support the bearish thesis:

Lack of Earnings: Although Uber is a well known brand name and a major player in the technology space, they have not reported positive earnings for a single quarter since going public. In the past two quarters Uber has lost $108 million (Q1 2021) and $968 million (Q4 2020). Although Uber seems to be closer to becoming profitable, it is discouraging to see continual revenue losses. Many companies, when initially going public, do not make a profit though, so there is a chance for Uber to turn it around. There is a lot of uncertainty going forward with Uber’s business model as the food delivery industry saw a major increase during COVID, but with more food delivery applications on the market and potentially less delivery orders, that seems like an uphill battle. Uber has managed to maintain its market control of the rideshare industry, but the decreased usage of rideshares apps and other factors listed below may narrow the gap between Uber and its competition.

Competition: Although Uber is one of the most recognizable brands in the space, there is immense amount of competition in all aspects of Uber Technologies. Due to COVID-19, Uber’s food delivery service increased in earnings, but that is where they face the most competition. Although Uber recently acquired Postmates, there are other services such as GrubHub, DoorDash, and Seamless, that offer stiff competition in the food delivery service. Uber currently has 22% market share for food delivery. However, because delivery is dependent on drivers that Uber hires remotely, they lack internal brand loyalty that might otherwise help lift Uber’s market position. Uber does have 68% of the market share in the ridesharing sector, but Lyft’s market share is increasing. With COVID-19, few customers used the rideshare feature of Uber and more used the food delivery service. Now that many restaurants and even some grocers are offering delivery from their own applications or hiring their own drivers to deliver food and products, many are going straight to the source instead of using a third party such as Uber. Uber will need to find a way to maintain or grow their control over market share in the ridesharing sector and continue to grow its position in the food delivery sector.

Negative Publicity: Uber unfortunately has been followed with negative publicity since 2014. In 2014, Uber began operating in cities without regard for local regulation. This caused many issues, including temporary bans in some cities and states. Uber has also launched fierce attacks on competitors that have garnered negative publicity. For example, Uber once orchestrated an attack on Gett, ordering rides only to cancel them later, wasting driver time and delaying service to actual customers. Uber also has been in the public eye for misleading drivers about earnings, short-changing drivers, and operating during a taxi strike. There have also been instances of Uber evading law enforcement operations in Greyball and Ripley. Unfortunately, this is not the end of the controversy. Uber had sexual harassment allegations which caused a management shakeup and the firing of 20 employees following an investigation. Uber has also had privacy concerns, including out-of-app customer tracking (tracking movements while not on the application) and data breaches. Finally, Uber is well-known for their clever maneuvering around U.S. tax codes - like it or not, this tends to draw the attention of federal agencies, which may spell trouble for investors. All in all, there have been a multitude of controversies and when there is controversy it is generally not good for the health of the company and it is not enticing for potential investors.

Learn more about Uber Technology here. Stay up to date on Green Candle by subscribing to our newsletter and following us on Twitter and Instagram!

Disclosure: The article was written by Daniel Kuhman and Brandon Keys, and it expresses the author's own opinions. They are not receiving compensation for it. They have no business relationships with any company whose stock is mentioned in this article. The information presented in this article is for informational purposes only and in no way should be construed as financial advice or recommendation to buy or sell any stock. Brandon and Daniel are not financial advisors. We encourage all readers to do further research and do your own due diligence before making any investments.