Walt Disney Co. (Ticker: DIS) - Brief Breakdown

In our Brief Breakdowns, we pick a stock and take opposite sides – one of us presents the bullish argument and the other presents the bearish argument.

If you haven’t already, subscribe to our newsletter here to get our articles directly to your inbox and follow us on Twitter and Instagram! Also join us for our Twitter spaces, every Monday we discuss our stock breakdown at 8 PM EST, & Friday we have a Bitcoin Happy Hour at 4:30 PM EST!

Company Description

The Walt Disney Company and its subsidiaries operate as a multinational entertainment and media conglomerate. Disney’s media networks operate domestic cable networks under the Disney, ESPN, Freeform, FX, and National Geographic brands as well as the television broadcast network under the ABC brand. Disney couples its media networks with in-person parks, experiences, and products such as Walt Disney World Resort, Disneyland, National Geographic Expeditions, and much more. Through the Studio Entertainment segment, they produce and distribute motion pictures under the Walt Disney Pictures, Twentieth Century Fox, Marvel, Lucasfilm, Pixar, Fox Searchlight Pictures, and Blue Sky Studios brands. The Studio Entertainment sector of Disney also develops, produces, and licenses live entertainment events and music. Disney also owns and operates streaming services such as Disney+, ESPN+, Hulu, and Hotstar.

Quantitative Analysis

At the time of this writing (11/27/2021), DIS is trading at $148.11 with a 52 week range of $145.85 - $203.02 and a market cap of $269.21B. In Q4 of 2021, revenues increased 26% year-over-year (YoY) to $18,534 million. Diluted earnings per share (EPS) went from losing $0.39 to earning $0.09 YoY. Return of equity (ROE: Net Income / Total Equity *100) of DIS is 2.39% and net margin (net income / revenue) is 3.1%. The debt to equities ratio (total liabilities / total equity) is 1.19. This financial analysis was done using financialstockdata.com (become a beta tester here). You can view DIS’s last quarterly earnings and annual report here. Below we have percent returns since IPO denominated in both USD and in Bitcoin.

Qualitative Analysis

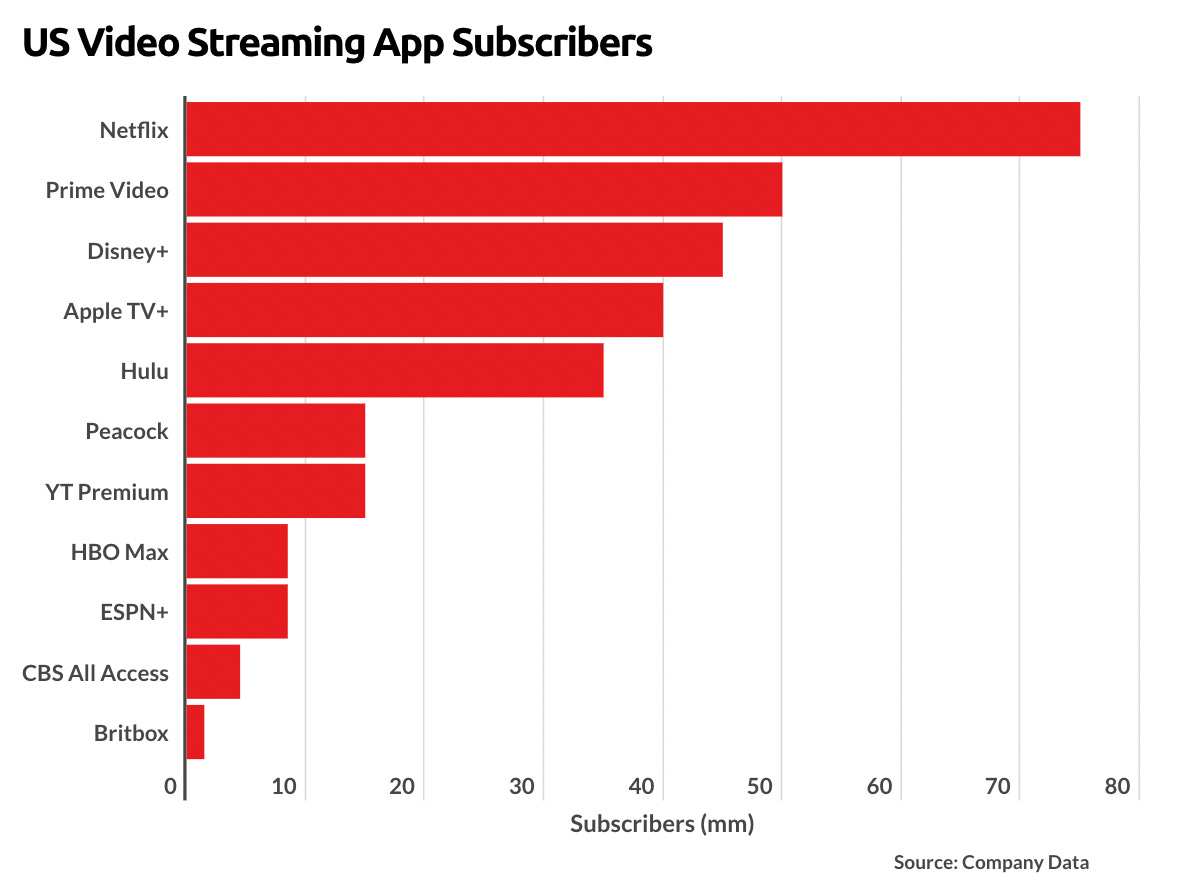

Disney is a media giant that has diversified its revenue through various avenues and subsidiaries that provide entertainment to a variety of consumer bases. The COVID-19 pandemic hurt Disney because production on many projects had to be halted and Disney had to find new ways to generate revenue. Disney+ was launched two years ago and now has 179 million total subscriptions and had 60% subscriber growth year-over-year. Consistent revenue from streaming services bolstered Disney throughout the pandemic when many were reluctant to travel and enjoy the live entertainment experiences that Disney offers (particularly their theme parks). Although Disney is a giant, it is in a difficult streaming war with Netflix, YouTube TV, and others. Although there are multiple players in the streaming war, Disney has their longevity to fall back on. Classic Disney movies are somewhat timeless and will always have fans who are willing to pay to watch those movies, purchase merchandise, and enjoy experiences and theme parks related to those movies. Disney looks poised to continue to grow and build off sustained revenue from Disney+, their other streaming services, and their live entertainment events.

Bullish Thesis

Here are three points to support the bullish thesis:

Product Diversity: Over the years, Disney has developed several strong sources of revenue. Perhaps the most obvious source of revenue is studio production. On top of their “one-and-done” classics like Snow White and Pinnochio, Disney has started and continues very successful franchises like Star Wars, Toy Story, and Frozen. Disney monetizes their studio productions not only through ticket sales and streaming revenue, but also through merchandising and live entertainment events. Speaking of streaming, Disney generates consistent revenue through Disney+, Hulu, and ESPN+, which have a combined total of 179 million subscribers. In addition to their studio productions and related lines of revenue (e.g., merchandise), Disney owns and operates several large theme parks/hotels, including Disneyland (California) and Walt Disney World (Florida). Prior to pandemic-related changes to operations (reduced capacity/complete shutdowns), Disney’s theme parks and hotels were responsible for ~35% of the company’s revenue. If these segments return to those pre-pandemic levels and add to their recent subscription segment gains, look for their revenue to spike.

Sentimental Value and a Proven Track Record: Many of Disney’s products have developed cult-like followings - think Mickey Mouse, Star Wars, Toy Story, etc. With complete control over the rights to these products, Disney can control when and where consumers can access them. This gives Disney a tremendous advantage over competitors, particularly in the streaming war that’s currently raging on in the entertainment industry. Disney can also monetize consumer nostalgia by selling merchandise and creating live entertainment events based on their most popular products (e.g., rides at their theme parks or traveling shows, like Disney On Ice). Whereas streaming competitors like Netflix are relatively new when it comes to creating and producing their own content, Disney has a long and successful history of doing so. As an investor, Disney’s track record of success is hard to ignore.

Parks Reopening: As stated above, Disney’s theme parks and hotels were responsible for major chunks of the company’s revenue. Unfortunately, revenue from both Disneyland and Walt Disney World plummeted during the COVID-19 pandemic. Although Walt Disney World in Florida was only closed for four months in 2020 (March through June), some estimate that the short-term closure cost the company nearly $5B. Even after re-opening, Disney World remained at reduced capacity for much of 2020 and 2021. Disneyland, on the other hand, was completely shuttered for over a year and continues to operate at reduced capacity. As the country re-opens and people return to pre-pandemic travel/vacation routines, look for these parks to contribute more substantially to revenue. Indeed, Disney’s new CEO Bob Chapek said in August that the company is “bullish” about the future of its U.S. theme parks and added that theme park reservations are higher now than in the company’s third fiscal quarter that ended in early July.

Bearish Thesis

Here are three points to support the bearish thesis:

Streaming Wars: With the trend of cutting the cord and people moving away from cable and moving towards streaming services, there has been an increase in competition. Disney does have three separate services that have quite a few subscribers in Disney+, Hulu and ESPN+, but Amazon and Netflix have a substantial lead in the US and Amazon Prime Video is also ahead of Disney+. With the competition comes the demand for new quality content, with the keyword being quality. Quality content takes a lot of capital to ensure big name producers and actors/actresses in order to keep people on their platform. Disney does have a big advantage with Disney+ having all Disney movies as well as ESPN+ having sporting events that people want to see. These advantages will keep consistent viewership, but in order to grow the production of quality content will take some capital.

Travel Precautions: Due to the COVID-19 pandemic and the new variants that seem to pop up weekly, many people are wary of traveling. The lack of traveling hurts not only Disney’s theme parks, but also hurts the Disney Cruise Lines. The revenue from Disney’s travel related sectors have increased since last year, but there is always the looming threat of additional shut downs. The shut downs have also delayed productions previously, with the most notable being a 15 month delay of “Black Widow”. Another shutdown could hinder their production of quality content, but Disney has old content that could help weather the storm barring any significant delays.

Recent Change in CEO: Disney has had a recent change in CEO as Bob Chapek, former chairman of Disney Parks, Experiences and Products was named the new CEO after Bob Iger stepped down in February 2020. Chapek has had his fair share of obstacles immediately with the COVID-19 pandemic starting just one month into his start as CEO and has handled it well so far. Iger left with big shoes to fill as Disney’s stock soared more than 400% or about 12% annualized returns. Chapek is left with the challenge of bringing in more “adult” viewers with a little more raunchy shows on its platforms. This will be a tough pivot in some aspects, especially for an unproven CEO at the helm.

Learn more about DIS here. Stay up to date on Green Candle by subscribing to our newsletter and following us on Twitter and Instagram! And don’t forget to join us in our Twitter Spaces tonight at 8 PM EST!

If you’re new to stock investing, check out our introduction to stock investing series:

Have a great week everyone,

Brandon & Daniel

Disclosure: The article was written by Daniel Kuhman and Brandon Keys, and it expresses the author's own opinions. They are not receiving compensation for it. They have no business relationships with any company whose stock is mentioned in this article. The information presented in this article is for informational purposes only and in no way should be construed as financial advice or recommendation to buy or sell any stock. Brandon and Daniel are not financial advisors. We encourage all readers to do further research and do your own due diligence before making any investments.