Saving for Retirement - Roth IRAs

If you haven’t already, subscribe to our newsletter here to get our articles delivered directly to your inbox and follow us on Twitter, Instagram, and YouTube! In our Educational Series we will be taking a deep dive into different ways to invest your money in hopes that one or multiple of these methods strikes you as interesting and encourages you to invest your money to grow your wealth.

What is a Roth IRA?

Established officially in 1997 and named after former U.S. Senator William Roth, a Roth IRA is an individual retirement account (IRA) that allows post-tax contributions and tax-free withdrawals (so long as certain conditions are satisfied). Although similar in some respects to traditional IRAs, Roth IRAs are unique in their tax structure. Specifically, contributions to Roth IRAs come from “after-tax” dollars; this means that the contributions are not tax-deductible. However, once you start withdrawing funds from the IRA, the money is tax free. Conversely, traditional IRA contributions are generally made with “pre-tax” dollars; this means that you can get a tax deduction on your contribution but that you will pay income tax when you withdraw funds from the account.

Who is eligible to open a Roth IRA?

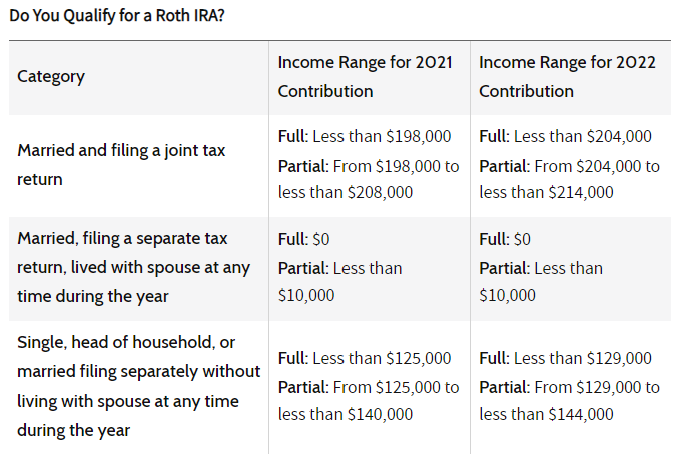

Anyone with earned income is eligible to open and contribute to a Roth IRA as long as they meet requirements concerning filing status and income. Anyone with annual income above a certain amount - which is periodically adjusted by the IRS - becomes ineligible. The chart below from Investopedia shows the eligibility figures for 2021 and 2022.

An individual who earns less than the ranges shown for their appropriate filing status can contribute up to 100% of their compensation or the contribution limit, whichever is less. For example, a single individual who earns less than $129,000 in 2021 is eligible to contribute the maximum amount allowed; a similar individual who earns $144,000 in 2022 will be unable to contribute to a Roth IRA.

A quick word about Choice by Kingdom Trust

Do you want to HODL BTC in a tax-advantaged retirement account? Check out Choice by Kingdom Trust, where both Daniel and Brandon hold their Roth IRAs. Click this LINK to find out more!

How much can you contribute to your Roth IRA?

For 2022, the maximum contribution to a Roth IRA is $6,000 for individuals under 50 and $7,000 for individuals 50 and older. If you meet the “full” contribution criteria laid out in the table above, you can make the maximum contribution. If you meet the “partial” contribution criteria, consult the IRS website for details on calculating your contribution limit here. And finally, if you meet the “zero” contribution criteria, you are unable to make any contributions to your Roth IRA. There is one other potential scenario: your annual income is less than the maximum contribution (for 2022, less than $6,000). For example, suppose you earn $2,000 in January and don't earn any additional money for the rest of the year. The maximum amount you can contribute to your Roth IRA will be $2,000 for that year.

What kind of contributions are allowed in your Roth IRA?

The IRS regulates not only the amount you can contribute to a Roth IRA, but also the type of money that can be deposited. Generally speaking, you are only allowed to contribute earned income to a Roth account. For individuals working for an employer, compensation that is eligible to fund a Roth IRA includes:

Wages

Salaries

Commissions

Bonuses

Any other amount paid to the individual for the services performed

For a self-employed individual, or a member of a pass-through business, compensation is the individual’s net earnings from their business, less any deduction allowed for contributions made to retirement plans on the individual’s behalf, and further reduced by 50% of the individual’s self-employment taxes.

The list of ineligible contributions includes:

Income from rental property or other profits from property maintenance

Interest income

Income from a pension or annuity

Stock dividends and capital gains

Passive income earned from a partnership in which you do not provide substantial services

When can you start to withdraw from your Roth IRA?

Now that you know what a Roth IRA is, who is eligible to contribute, how much you can contribute, and what kinds of funds can be contributed, let’s get to the fun part: making withdrawals in retirement!

You can technically withdraw contributions from your Roth IRA at any age, both tax- and penalty-free, so long as you take out only an amount equal to or less than the sum that you’ve put in. In other words, so long as you do not withdraw a sum more than that which you’ve contributed, then the distribution is not considered taxable income and is not subject to penalty, regardless of your age or how long the funds have been in the account.

However, for distribution of account earnings (the amount earned on top of contributions, for example through stock price growth) to be considered a qualified distribution and occur tax- and penalty-free, it must occur at least five years after the Roth IRA owner established and funded their first Roth account, and under at least one of the following conditions:

The Roth IRA holder is at least age 59½ when the distribution occurs.

The distributed assets are used toward purchasing—or building or rebuilding—a first home for the Roth IRA holder or a qualified family member. However, this is limited to $10,000 per lifetime.

The distribution occurs after the Roth IRA holder becomes disabled.

The assets are distributed to the beneficiary of the Roth IRA holder after the Roth IRA holder’s death.

If the conditions described above are not met, withdrawal of account earnings will be subjected to taxes and, if you’re under the age of 59½, a penalty fee.

It’s never too early to start saving for retirement

As we said in our introduction to this series, if you take one thing from this series on retirement investing, let it be this: it’s never too early to start saving for retirement - it may seem like a lifetime away, but time will go fast and your future self will be glad you started saving early! As always, we hope that you will find this series useful and please don’t hesitate to reach out with comments or questions about the content! Here is a running list of the articles included in this series:

Retirement Investing - Roth IRA

If you liked this article, please subscribe to our newsletter and be sure to follow us on Twitter, Instagram and YouTube!

Finish out the week strong!

Brandon and Dan

Disclosure: The article was written by Daniel Kuhman and Brandon Keys, and it expresses the author's own opinions. The information presented in this article is for informational purposes only and in no way should be construed as financial advice or recommendation to buy or sell any stock, asset, or cryptocurrency. Brandon and Daniel are not financial advisors. We encourage all readers to do further research and do your own due diligence before making any investments.