Redfin Corp. (Ticker: RDFN) - Brief Breakdown

In our Brief Breakdowns, we pick a stock and take opposite sides – one of us presents the bullish argument and the other presents the bearish argument.

If you haven’t already, subscribe to our newsletter here to get our articles directly to your inbox and follow us on Twitter and Instagram!

Company Description

Redfin is an American based full-service real estate brokerage. RDFN operates an online real estate marketplace, similar to Zillow (which we broke down last week), which provides real estate services including assisting in the purchase or sale of a home. RDFN also provides title and settlement services, originates and sells mortgages, and buys and sells homes. Redfin’s business model is to undercut competition based on sellers paying Redfin a discounted fee, either 1.0% or 1.5% to list the seller’s home. The company also charges an additional fee of ~2.0% - 3.0% to the seller to compensate the brokerage representing the buyer. Redfin went public in 2017 through an IPO. Redfin recently announced the acquisition of RentPath, a media company that owns Rent.com, ApartmentGuide.com, Lovely, and Rentals.com.

Quantitative Analysis

At the time of this writing (7/18/2021), Redfin is trading at $54.11 with a 52 week range of $37.31 - $98.44 and a market cap of $5.63B. In Q1 of 2021, Redfin’s market share increased from 0.21% to 1.14% of all existing home sales in the US, saved homebuyers and sellers over $42 million, and posted revenue of $268 million (a year-over-year increase of 40% compared to Q1 of 2020). Real estate services gross margin was 24% compared to 14% in Q1 2020 and operating expenses increased 9% during the same period. The return of equity (ROE: Net Income / Total Equity *100) of Redfin is 1.28%, the debt to equities (D/E) ratio is 3.74, and the Net Margin (Net Income / Revenue) is 0.6%. In the past year, the RDFN stock has underperformed the S&P 500, increasing from a low of $38.73 to its current value of $54.11. This financial analysis was done using financialstockdata.com (become a beta tester here). You can view RDFN’s 2021 Q1 earnings here and their 2020 Annual Report here.

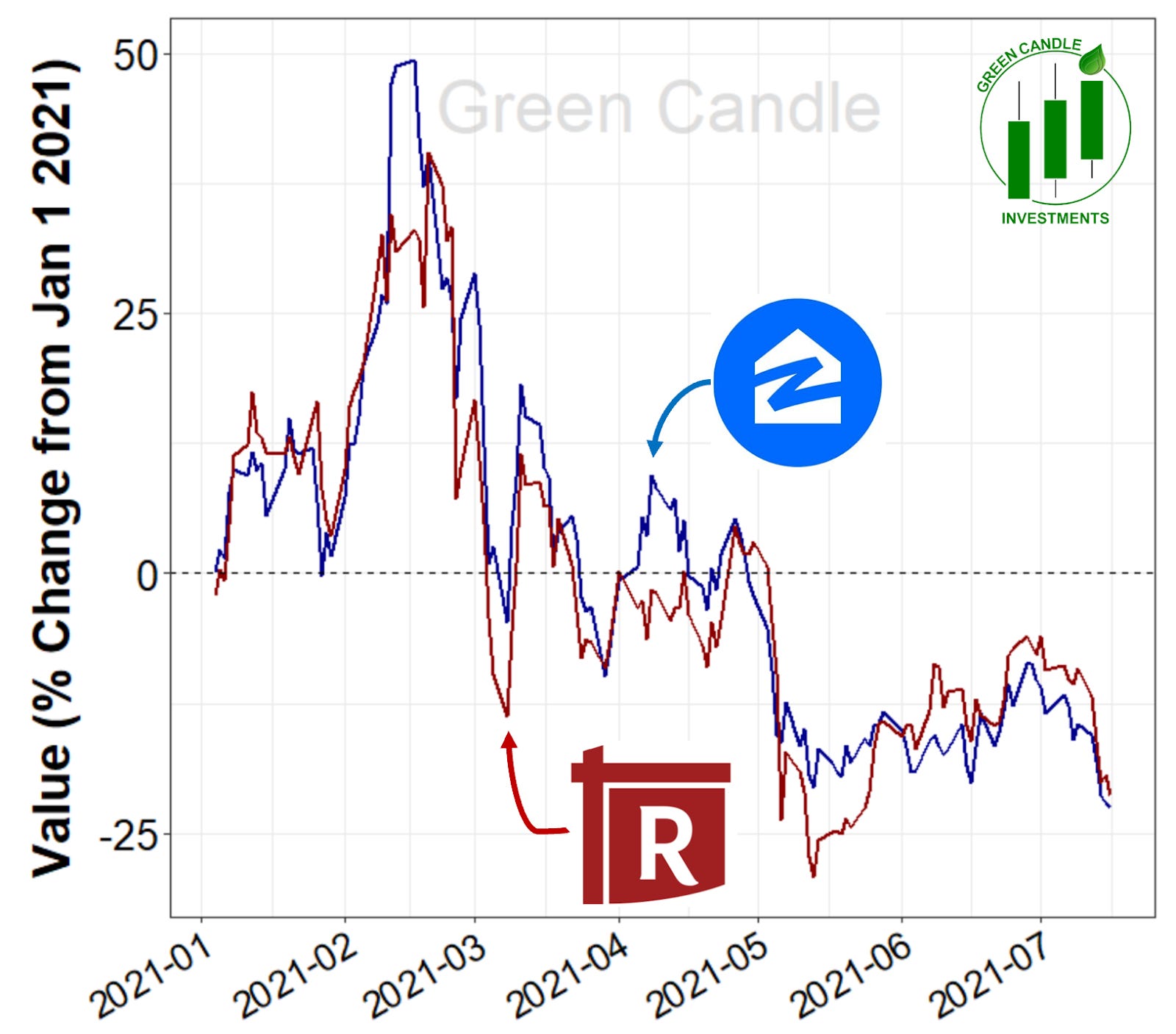

YTD Change in Price: RDFN vs ZG

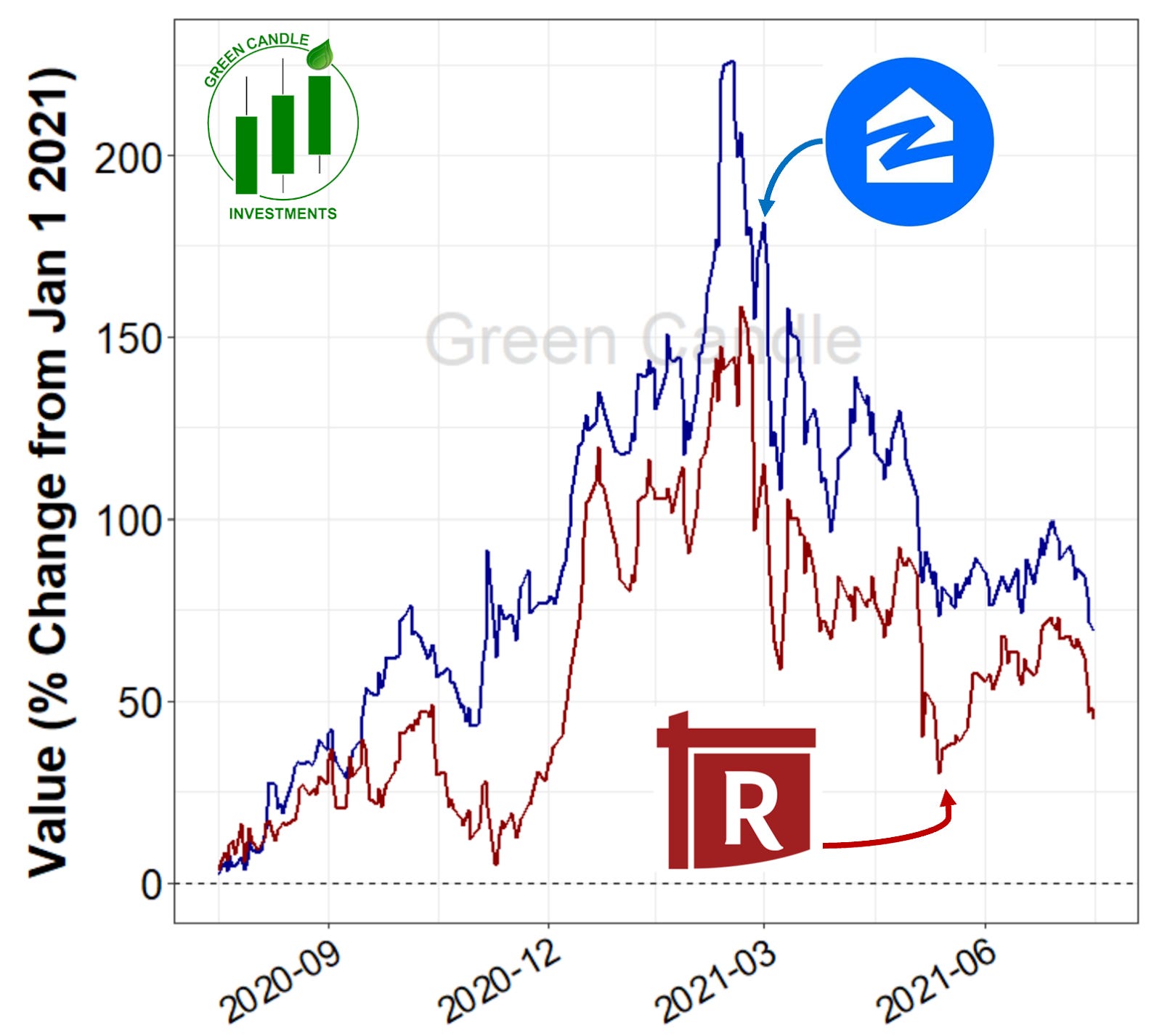

12-Month Change in Price: RDFN vs ZG

Qualitative Analysis

Redfin is a real estate broker and a real estate e-commerce website which means the business benefits when there is a lot of inventory and houses are on the market for a period of time. Unfortunately for Redfin, and Zillow for that matter, the real estate market is extremely hot right now so houses are flying off the shelves. Redfin is an up and coming disrupter in the real estate space that uses its tech-driven operating model to stand out. Similarly to Zillow, Redfin is also starting to offer RedfinNOW in select markets to allow sellers to sell their homes directly to Redfin for cash. Redfin also offers the ability to handle home inspections, title, and appraisal paperwork, making Redfin a potential one stop shop for all things real estate related. Redfin has large competition with the name brand in the e-commerce real estate space, Zillow (which we broke down last week) so it has room to grow in the rapidly growing industry. Although Redfin is not the top player in the real-estate e-commerce space, the industry is a $1.9 trillion industry and Redfin holds an average of 42 million monthly users to encourage sellers to market their homes on their platform.

Bullish Thesis

Here are three points to support the bullish thesis:

Building tech to reduce friction in an established service: A common theme throughout many of our breakdowns has been the use of technology to improve services and/or products in time-tested industries. For example, we broke down Uber, which used technology to reduce friction points in the ride hailing industry. Although we have not broken down Intuit, they offer TurboTax to facilitate online tax filing (again, using tech to reduce friction points in an existing industry). Redfin is now one of several companies (including Zillow) to successfully leverage technology to improve real estate services. Buying and selling real estate is a notoriously daunting task - and rightfully so, it’s a complicated and often costly endeavor. Similar to Uber and TurboTax, Redfin’s goal is to create a digital platform that reduces the friction points associated with buying or selling a home. So long as Redfin can continue to develop and successfully scale its platform, investors can expect the company to rise in value, as the real estate industry may have ebbs and flows but will always exist.

Steady growth and successful scaling: One difficult aspect of any tech-related disruptor is convincing people that the new way of doing something beats the old way. Redfin appears to be successful in convincing both customers and agents that their platform beats traditional brokerage services. Their market share in the residential market continues to rise (currently standing at 1.14%, up ~23% and ~37% from the same period in 2020 and 2019, respectively). Their YoY revenue also reflects steady and substantial growth. From 2017 to 2020, their revenue rose from $370M to $886M - a 139% increase in less than 5 years! Redfin’s monthly average visitors rose from 35.5M to 46.2M in Q1 of 2021 versus the same period of 2020. This particular trend will only continue to rise given Redfin’s recent acquisition of RentPath, a major media company that owns Rent.com, ApartmentGuide.com, Lovely, and Rentals.com. According to an article at seekingalpha.com, RentPath draws in ~16M monthly visitors and posted revenue of ~200M in 2020. Growth-by-acquisition can be beneficial, so long as Redfin successfully incorporates the new entities into its own model and optimizes the additional sources of revenue. Regardless, Redfin has proven its ability to steadily grow over time.

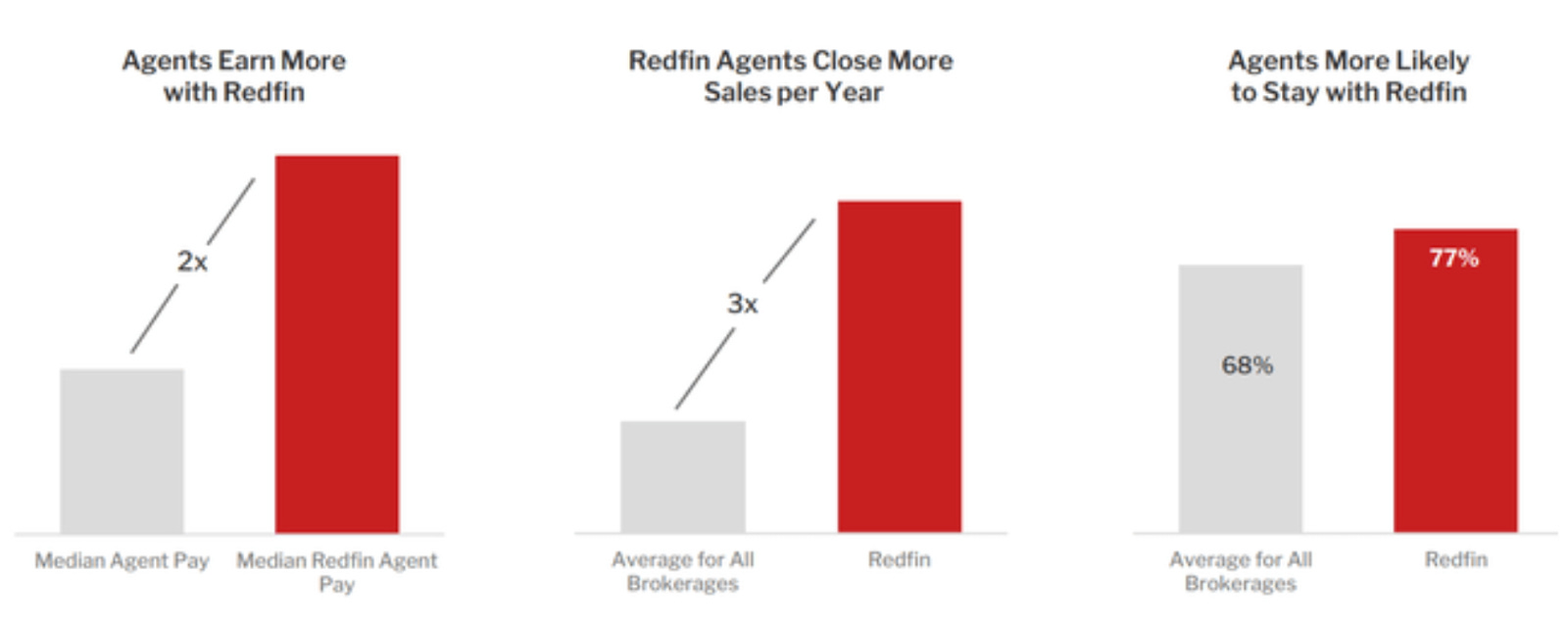

Positive for both customers and agents: When we broke down Airbnb, part of our bearish thesis was their struggle to onboard new hosts. This necessarily limits Airbnb’s ability to scale their service to more consumers (there is a physical limit in how many options their consumers have). Similarly, for a company like Redfin to scale successfully (i.e., meet a growing customer base), they will need to hire more real estate agents. Redfin is appealing for new agents for a number of reasons: their agents earn ~2x more than median agent pay for all brokerages and they close ~3x more sales than the average agent from all brokerages. This helps with agent retention (77% of current agents say they are likely to stay) and can help entice new agents. If Redfin can facilitate new agent onboarding and keep agent turnover low, look for them to be well positioned to handle an increased customer base.

Source: Redfin investors presentation.

Bearish Thesis

Here are three points to support the bearish thesis:

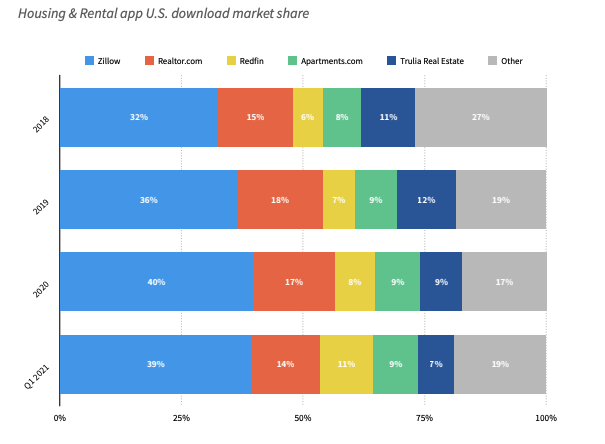

Substantial Gap with Zillow: As previously mentioned in our breakdown with Zillow, there is a substantial gap between the amount of users on Zillow’s platform compared to Redfin. Zillow also owns Truila which is comparable to the size of Redfin. Redfin had 42 million average monthly users in 2020 and in May of 2021, Zillow’s user growth grew by 59 million users for a total of 315 million for that month alone. That is not to say that 42 million is not a substantial amount, but with the way the housing market is and houses being on the market for little to no time, this does not suit Redfin to grow its business. Redfin will have to find creative ways to stand out or spend massive amounts of money on marketing in order to try to shrink the gap with Zillow.

Current Real Estate Market: You might think that because the real estate market is so hot right now that this would benefit Redfin, well think again. As mentioned above, homes are flying off the shelves and do not need to be put on multiple (or any) real estate e-commerce sites in order to help with the sale. Redfin benefits when sellers need to use their site in order to sell homes, but as hot as the market is right now there is no need for an e-commerce website. It is unclear whether the housing market will shift or change in the near future, but with no rate change discussions occurring until 2023 it seems this market will continue for at least the near future.

Inflation of Home Prices: Unfortunately inflation is at its highest month over month average since June of 2008, we’ve highlighted a couple tweet threads about it (data driven & cost driven) and housing prices have been skyrocketing. If the inflation continues, there will need to be a monumental crash in order to bring housing prices back to a place where housing is affordable for first time home buyers. If housing becomes unattainable for the average American, there might be monthly users who simply browse or “window shop” on Redfin but do not look to purchase. If that’s the case, Redfin will need to profit off of advertisements or some other kind of revenue based on views to their website instead of being a modern real estate broker which is the goal of the company.

Learn more about Redfin here. Stay up to date on Green Candle by subscribing to our newsletter and following us on Twitter and Instagram!

Have a great week everyone,

Brandon & Daniel

Disclosure: The article was written by Daniel Kuhman and Brandon Keys, and it expresses the author's own opinions. They are not receiving compensation for it. They have no business relationships with any company whose stock is mentioned in this article. The information presented in this article is for informational purposes only and in no way should be construed as financial advice or recommendation to buy or sell any stock. Brandon and Daniel are not financial advisors. We encourage all readers to do further research and do your own due diligence before making any investments.